TCF Bank 2014 Annual Report Download - page 47

Download and view the complete annual report

Please find page 47 of the 2014 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

|

|

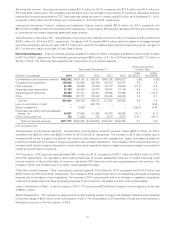

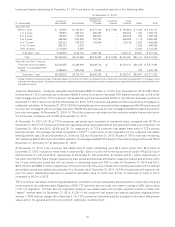

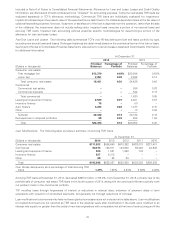

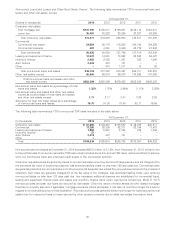

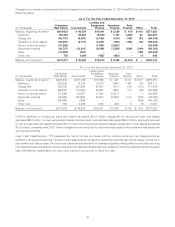

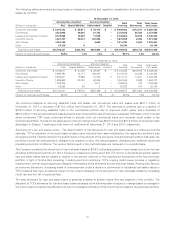

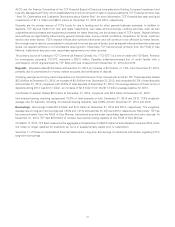

loan is performing based on the restructured terms; however, these loans are still considered impaired and follow TCF’s impaired

loan reserve policies.

Under consumer real estate programs, TCF typically reduces a customer’s contractual payments by an amount appropriate for

the borrower’s financial condition. Due to clarifying bankruptcy-related regulatory guidance adopted in the third quarter of 2012,

loans discharged in Chapter 7 bankruptcy where the borrower did not reaffirm the debt are reported as non-accrual TDR loans

upon discharge as a result of the removal of the borrower’s personal liability on the loan. Due to additional clarifying regulatory

guidance adopted in the first quarter of 2014, these loans may now return to accrual status when TCF expects full repayment of

the remaining pre-discharged contractual principal and interest. Although loans classified as TDR loans are considered impaired,

TCF received more than 47% of the original contractual interest due on accruing consumer real estate TDR loans in 2014,

yielding 3.3%, by modifying the loans to qualified customers instead of foreclosing on the property.

Commercial loans that are 90 or more days past due and not well secured at the time of modification remain on non-accrual

status. Regardless of whether contractual principal and interest payments are well-secured at the time of modification,

equipment finance loans that are 90 or more days past due remain on non-accrual status. Loans modified when on non-accrual

status continue to be reported as non-accrual loans until there is sustained repayment performance for a reasonable period of at

least six consecutive months. At December 31, 2014, 87.7% of total commercial TDR loans were accruing and TCF recognized

more than 93% of the original contractual interest due on accruing commercial TDR loans in 2014. At December 31, 2014,

collection of principal and interest under the modified terms was reasonably assured on all accruing commercial TDR loans.

TCF utilizes a multiple note structure as a workout alternative for certain commercial loans, which restructures a troubled loan

into two notes. When utilizing this multiple note structure, the first note is always classified as a TDR loan. Under TCF policy, the

first note is established at an amount and with market terms that provide reasonable assurance of payment and performance. If

the loan was modified at an interest rate equal to the yield of a new loan originated with comparable risk at the time of

restructuring and the loan is performing based on the terms of the restructuring agreement, this note may be removed from TDR

loan classification in the calendar year after modification. This note is reported on accrual status if the loan has been formally

restructured so as to be reasonably assured of payment and performance according to its modified terms. This evaluation

includes consideration of the customer’s payment performance for a reasonable period of at least six consecutive months, which

may include time prior to the restructuring, before the loan is returned to accrual status. The second note is charged-off. This

second note is a separate and distinct legal contract and is still outstanding. Should the borrower’s financial position improve, the

loan may become recoverable. At December 31, 2014, one TDR loan restructured as multiple notes with a combined total

contractual balance of $12.4 million and a remaining book balance of $11.4 million is included in the preceding table.

See Note 6 of Notes to Consolidated Financial Statements, Allowance for Loan and Lease Losses and Credit Quality Information,

for additional information regarding TCF’s loan modifications.

34