Qantas 2008 Annual Report Download - page 142

Download and view the complete annual report

Please find page 142 of the 2008 Qantas annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

-

154

-

155

-

156

|

|

140 Qantas Annual Report 2008

Notes to the Financial Statements

for the year ended 30 June 2008

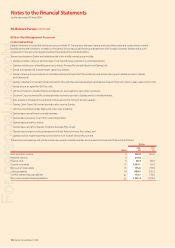

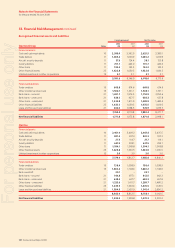

(C) Credit risk

Credit risk is the potential loss from a transaction in the event of default by the counterparty during the term of the transaction or on settlement

of the transaction. Credit exposure is measured as the cost to replace existing transactions should a counterparty default.

The Qantas Group conducts transactions with the following major types of counterparties:

trade debtor counterparties – the credit risk is the recognised amount, net of any impairment losses. As at 30 June 2008, this amounted

to $1,085.2 million (2007: $1,039.9 million). The Qantas Group has credit risk associated with travel agents, industry settlement organisations

and credit provided to direct customers. The Qantas Group minimises this credit risk through the application of stringent credit policies and

accreditation of travel agents through industry programs; and

other fi nancial asset counterparties – the Qantas Group restricts its dealings to counterparties that have acceptable credit ratings. Should the

rating of a counterparty fall below certain levels, internal policy dictates that approval by the Board is required to maintain the level of the

counterparty exposure.

The table below set out the maximum exposure to credit risk as at 30 June 2008:

Qantas Group Qantas

2008

$M

2007

$M

2008

$M

2007

$M

On Balance Sheet

Cash and cash equivalents 2,599.0 3,362.9 2,461.0 3,409.3

Trade debtors 1,085.2 1,039.9 841.3 937.3

Other loans 142.2 142.2 1,994.1 1,018.8

Aircraft security deposits 37.6 124.4 27.3 114.7

Sundry debtors 701.7 443.0 627.5 299.1

Other fi nancial assets 1,422.8 1,030.5 1,424.8 1,030.5

Off Balance Sheet

Operating leases as lessor 126.0 134.0 67.2 52.0

Total 6,114.5 6,276.9 7,443. 2 6,861.7

The Qantas Group minimises the concentration of credit risk by undertaking transactions with a large number of customers and counterparties

in various countries in accordance with Board approved policy. As at 30 June 2008, the credit risk of the Qantas Group to counterparties in relation

to other fi nancial assets, cash and cash equivalents, and other fi nancial liabilities where a right of offset exist amounted to $3,831.9 million (2007:

$4,727.5 million) and was spread over a number of regions, including Australia, Asia, Europe and the United States of America. Excluding associated

entities, Qantas Group’s credit exposure is with counterparties which have a minimum credit rating of A- / A3.

(D) Net fair value

The net fair value of cash, cash equivalents and non-interest-bearing fi nancial assets and liabilities approximates their carrying value due to their short

maturity. The net fair value of other fi nancial assets and liabilities is determined by valuing them at the present value of future contracted cash fl ows.

Cash fl ows are discounted using standard valuation techniques at the applicable market yield, having regard to the timing of the cash fl ows.

The net fair value of forward foreign exchange and fuel contracts is determined as the unrealised gain/loss at balance date by reference to market

exchange rates and fuel prices. The net fair value of interest rate swaps is determined as the present value of future contracted cash fl ows. Cash fl ows

are discounted using standard valuation techniques at the applicable market yield, having regard to the timing of the cash fl ows. The net fair value

of options is determined using standard valuation techniques.

Other fi nancial assets and liabilities represent the fair value of derivative fi nancial instruments recognised on Balance Sheet in accordance

with AASB 139.

•

•

33. Financial Risk Management continued

For personal use only