Foot Locker 2014 Annual Report Download - page 87

Download and view the complete annual report

Please find page 87 of the 2014 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

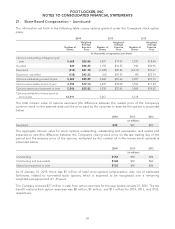

FOOT LOCKER, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

20. Retirement Plans and Other Benefits − (continued)

The Company’s investment strategy seeks to utilize asset classes with differing rates of return, volatility, and

correlation in order to reduce risk by providing diversification relative to equities. Diversification within asset

classes is also utilized to ensure that there are no significant concentrations of risk in plan assets and to reduce

the effect that the return on any single investment may have on the entire portfolio.

The target composition of the Company’s Canadian qualified pension plan assets is 95 percent fixed-income

securities and 5 percent equity. The Company believes that plan assets are invested in a prudent manner with

the same overall objective and investment strategy as noted above for the U.S. pension plan. The bond

portfolio is comprised of government and corporate bonds chosen to match the duration of the pension plan’s

benefit payment obligations. This current asset allocation will limit future volatility with regard to the funded

status of the plan. This allocation has resulted in higher pension expense due to the lower long-term rate of

return associated with fixed-income securities.

The assets related to the Runners Point Group pension plans were not significant.

Valuation of Investments

Significant portions of plan assets are invested in commingled trust funds. These funds are valued at the net

asset value of units held by the plan at year end. Stocks traded on U.S. security exchanges are valued at closing

market prices on the measurement date.

The fair values of the Company’s U.S. pension plan assets at January 31, 2015 and February 1, 2014 were as

follows:

Level 1 Level 2 Level 3 2014

Total 2013

Total*

(in millions)

Cash and cash equivalents $ — $ 1 $ — $1 $—

Equity securities:

U.S. large-cap

(1)

— 102 — 102 101

U.S. mid-cap

(1)

—31—31 30

International

(2)

—71—71 67

Corporate stock

(3)

21 — — 21 15

Fixed-income securities:

Long duration corporate and government

bonds

(4)

— 254 — 254 236

Intermediate duration corporate and

government bonds

(5)

— 110 — 110 105

Other types of investments:

Real estate securities

(6)

—20—20 20

Insurance contracts — 1 — 11

Other

(7)

—2—2—

Total assets at fair value $ 21 $592 $ — $613 $575

* Each category of plan assets is classified within the same level of the fair value hierarchy for 2014 and 2013.

(1) These categories consist of various managed funds that invest primarily in common stocks, as well as other equity securities and a

combination of other funds.

(2) This category comprises three managed funds that invest primarily in international common stocks, as well as other equity securities

and a combination of other funds.

(3) This category consists of the Company’s common stock. The increase from the prior year is due to price appreciation No additional

stock was contributed during the year.

(4) This category consists of various fixed-income funds that invest primarily in long-term bonds, as well as a combination of other funds,

that together are designed to exceed the performance of related long-term market indices.

64