Foot Locker 2014 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2014 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

FOOT LOCKER, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Summary of Significant Accounting Policies − (continued)

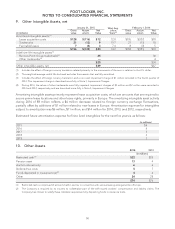

Goodwill and Other Intangible Assets

Goodwill and intangible assets with indefinite lives are reviewed for impairment annually during the first quarter

of its fiscal year or more frequently if impairment indicators arise.

The review of goodwill impairment consists of either using a qualitative approach to determine whether it is more likely

than not that the fair value of the assets is less than their respective carrying values or a two-step impairment test, if

necessary. If, based on the results of the qualitative assessment, it is concluded that it is not more likely than not that the

fair value of the intangible asset is greater than its carrying value, the two-step test is performed to identify potential

impairment. If it is determined that it is not more likely than not that the fair value of the reporting unit is less than its

carrying value, it is unnecessary to perform the two-step impairment test. Based on certain circumstances, we may elect

to bypass the qualitative assessment and proceed directly to performing the first step of the two-step impairment test.

The first step of the two-step goodwill impairment test compares the fair value of the reporting unit to its carrying

amount, including goodwill. The second step includes hypothetically valuing all the tangible and intangible assets of

the reporting unit as if the reporting unit had been acquired in a business combination. Then, the implied fair value of

the reporting unit’s goodwill is compared to the carrying amount of that goodwill. If the carrying value of the asset

exceeds its fair value, an impairment loss is recognized in the amount of the excess. The fair value of each reporting unit

is determined using a combination of market and discounted cash flow approaches.

Intangible assets that are determined to have finite lives are amortized over their useful lives and are measured

for impairment only when events or changes in circumstances indicate that the carrying value may be impaired.

Intangible assets with indefinite lives are tested for impairment if impairment indicators arise and, at a minimum,

annually. We estimate the fair value based on an income approach using the relief-from-royalty method.

Derivative Financial Instruments

All derivative financial instruments are recorded in the Company’s Consolidated Balance Sheets at their fair

values. For derivatives designated as a hedge, and effective as part of a hedge transaction, the effective portion

of the gain or loss on the hedging derivative instrument is reported as a component of other comprehensive

income/loss or as a basis adjustment to the underlying hedged item and reclassified to earnings in the period

in which the hedged item affects earnings. The effective portion of the gain or loss on hedges of foreign net

investments is generally not reclassified to earnings unless the net investment is disposed of. To the extent

derivatives do not qualify or are not designated as hedges, or are ineffective, their changes in fair value are

recorded in earnings immediately, which may subject the Company to increased earnings volatility.

Fair Value

The Company categorizes its financial instruments into a three-level fair value hierarchy that prioritizes the

inputs to valuation techniques used to measure fair value into three broad levels. The fair value hierarchy gives

the highest priority to quoted prices in active markets for identical assets or liabilities (Level 1) and the lowest

priority to unobservable inputs (Level 3). If the inputs used to measure fair value fall within different levels of the

hierarchy, the category level is based on the lowest priority level input that is significant to the fair value

measurement of the instrument. Fair value is determined based upon the exit price that would be received to

sell an asset or paid to transfer a liability in an orderly transaction between market participants exclusive of any

transaction costs. The Company’s financial assets recorded at fair value are categorized as follows:

Level 1 — Quoted prices for identical instruments in active markets.

Level 2 — Quoted prices for similar instruments in active markets; quoted prices for identical or similar

instruments in markets that are not active; and model-derived valuations in which all significant inputs or

significant value-drivers are observable in active markets.

Level 3 — Model-derived valuations in which one or more significant inputs or significant value-drivers are

unobservable.

44