Foot Locker 2014 Annual Report Download - page 53

Download and view the complete annual report

Please find page 53 of the 2014 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

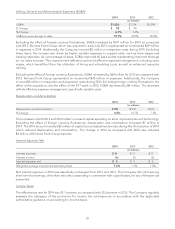

In 2014, the Company elected to perform its review of goodwill using the two-step impairment test approach.

The Company used a combination of a discounted cash flow approach and market-based approach to

determine the fair value of a reporting unit. The determination of discounted cash flows of the reporting units

and assets and liabilities within the reporting units requires significant estimates and assumptions. These

estimates and assumptions primarily include, but are not limited to, the discount rate, terminal growth rates,

earnings before depreciation and amortization, and capital expenditures forecasts. The market approach

requires judgment and uses one or more methods to compare the reporting unit with similar businesses,

business ownership interests, or securities that have been sold. Due to the inherent uncertainty involved in

making these estimates, actual results could differ from those estimates. The Company has evaluated the merits

of each significant assumption, both individually and in the aggregate, used to determine the fair value of the

reporting units, as well as the fair values of the corresponding assets and liabilities within the reporting units,

and concluded they are reasonable and are consistent with prior valuations. The fair value of all the

reporting units substantially exceeded their carrying values.

Owned trademarks and tradenames that have been determined to have indefinite lives are not subject to

amortization but are reviewed at least annually for potential impairment. The fair values of purchased intangible

assets are estimated and compared to their carrying values. We estimate the fair value of these intangible

assets based on an income approach using the relief-from-royalty method. This methodology assumes that, in

lieu of ownership, a third party would be willing to pay a royalty in order to exploit the related benefits of these

types of assets. This approach is dependent on a number of factors, including estimates of future growth and

trends, royalty rates in the category of intellectual property, discount rates, and other variables. We base our fair

value estimates on assumptions we believe to be reasonable, but which are unpredictable and inherently

uncertain. Actual future results may differ from those estimates. We recognize an impairment loss when the

estimated fair value of the intangible asset is less than the carrying value. During 2014, impairment charges

totaled $4 million.

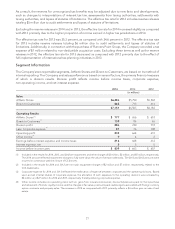

Share-Based Compensation

The Company estimates the fair value of options granted using the Black-Scholes option pricing model. The

Black-Scholes option pricing valuation model requires the use of subjective assumptions. Changes in these

assumptions, listed below, can materially affect the fair value of the options.

Risk-free Interest Rate — The risk-free interest rate is determined using the Federal Reserve nominal rates for

U.S. Treasury zero-coupon bonds with maturities similar to those of the expected term of the award being

valued.

Expected Volatility — The Company estimates the expected volatility of its common stock at the grant date

using a weighted-average of the Company’s historical volatility and implied volatility from traded options on

the Company’s common stock. A 50 basis point change in volatility would cause a 1 percent change to the fair

value.

Expected Term — The expected term of options granted is estimated using historical exercise and post-vesting

employment termination patterns, which the Company believes are representative of future behavior. Changing

the expected term by one year changes the fair value by 7 to 8 percent depending on if the change was an

increase or decrease to the expected term.

Dividend Yield — The expected dividend yield is derived from the Company’s historical experience. A 50 basis

point change to the dividend yield would change the fair value by approximately 5 percent.

Share-based compensation expense is recorded for those awards expected to vest using an estimated

forfeiture rate based on the Company’s historical pre-vesting forfeiture data, which it believes are representative

of future behavior, and periodically will revise those estimates in subsequent periods if actual forfeitures differ

from those estimates.

30