Foot Locker 2014 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2014 Foot Locker annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

FOOT LOCKER, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS

1. Summary of Significant Accounting Policies − (continued)

and sourcing costs are capitalized in merchandise inventories. The Company expenses the freight associated with

transfers between its store locations in the period incurred. The Company maintains an accrual for shrinkage based

on historical rates.

Cost of sales is comprised of the cost of merchandise, as well as occupancy, buyers’ compensation, and

shipping and handling costs. The cost of merchandise is recorded net of amounts received from suppliers for

damaged product returns, markdown allowances, and volume rebates, as well as cooperative advertising

reimbursements received in excess of specific, incremental advertising expenses. Occupancy costs include the

amortization of amounts received from landlords for tenant improvements.

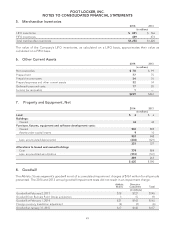

Property and Equipment

Property and equipment are recorded at cost, less accumulated depreciation and amortization. Significant

additions and improvements to property and equipment are capitalized. Depreciation and amortization are

computed on a straight-line basis over the following estimated useful lives:

Buildings Maximum of 50 years

Leasehold improvements 10 years or term of lease, if shorter

Furniture, fixtures, and equipment 3 − 10 years

Software 2 − 7 years

Maintenance and repairs are charged to current operations as incurred. Major renewals or replacements that

substantially extend the useful life of an asset are capitalized and depreciated.

Internal-Use Software Development Costs

The Company capitalizes certain external and internal computer software and software development costs incurred

during the application development stage. The application development stage generally includes software design

and configuration, coding, testing, and installation activities. Capitalized costs include only external direct cost of

materials and services consumed in developing or obtaining internal-use software, and payroll and payroll-related

costs for employees who are directly associated with and devote time to the internal-use software project.

Capitalization of such costs ceases no later than the point at which the project is substantially complete and ready

for its intended use. Training and maintenance costs are expensed as incurred, while upgrades and enhancements

are capitalized if it is probable that such expenditures will result in additional functionality. Capitalized software, net

of accumulated amortization, is included as a component of property and equipment and was $39 million and

$38 million at January 31, 2015 and February 1, 2014, respectively.

Recoverability of Long-Lived Assets

The Company reviews long-lived tangible and intangible assets with finite lives for impairment losses whenever

events or changes in circumstances indicate that the carrying amounts may not be recoverable. Management’s

policy in determining whether an impairment indicator exists, a triggering event, comprises measurable

operating performance criteria at the division level, as well as qualitative measures. The Company considers

historical performance and future estimated results, which are predominately identified from the Company’s

strategic long-range plans, in its evaluation of potential store-level impairment and then compares the carrying

amount of the asset with the estimated future cash flows expected to result from the use of the asset. If the

carrying amount of the asset exceeds the estimated expected undiscounted future cash flows, the Company

measures the amount of the impairment by comparing the carrying amount of the asset with its estimated fair

value. The estimation of fair value is measured by discounting expected future cash flows at the Company’s

weighted-average cost of capital. The Company estimates fair value based on the best information available

using estimates, judgments, and projections as considered necessary.

43