Chevron 2009 Annual Report Download - page 84

Download and view the complete annual report

Please find page 84 of the 2009 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92

|

|

FS-PB

82 Chevron Corporation 2009 Annual Report

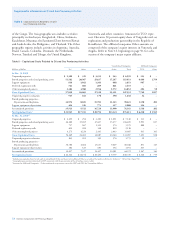

Supplemental Information on Oil and Gas Producing Activities

with the Angola LNG project accounted for a majority of the

632 BCF increase in Other affiliated companies.

In 2009, net revisions increased reserves by 569 BCF for

consolidated companies and decreased reserves by 44 BCF for

affiliated companies. For consolidated companies, net increases

were 493 BCF in Asia primarily as a result of reservoir studies

in Bangladesh and development drilling in Thailand. These

results were partially offset by a downward revision due to

the impact of higher prices on production-sharing contracts

in Myanmar. The United States and Other regions increased

reserves 39 BCF and 33 BCF, respectively. In the United States,

development drilling in the Gulf of Mexico was partially offset

by performance revisions in the California and mid-continent

areas. In Other regions, improved reservoir performance and

compression in Australia was partially offset by the effect of

higher prices on production-sharing contracts in Trinidad.

For equity affiliates, a downward revision of 237 BCF at

TCO was due to the effect of higher prices on royalty determi-

nation and an increase in gas injection for SGI/SGP facilities.

This decline was partially offset by performance and drilling

opportunities related to the Angola LNG project.

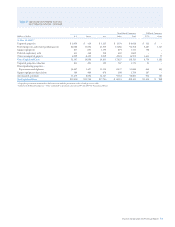

Extensions and Discoveries In 2007, extensions and dis-

coveries accounted for an increase of 518 BCF worldwide.

The largest addition was 330 BCF in Bangladesh, the result

of drilling activities. Other additions were not individually

significant.

In 2009, worldwide extensions and discoveries of 4,387

BCF were attributed to consolidated companies. The Gorgon

Project in Australia accounted for essentially all of the 4,277

BCF additions in the Other regions. In Asia, development drill-

ing in Thailand accounted for the majority of the increase. In

the United States, delineation drilling in California accounted

for the majority of the increase.

Purchases In 2007, purchases of natural gas reserves

were 141 BCF for consolidated companies, which include the

acquisition of an additional interest in the Bibiyana Field in

Bangladesh. Affiliated company purchases of 211 BCF related

to the formation of a new Hamaca equity affiliate in Venezuela

and an initial booking related to the Angola LNG project.

Sales In 2007, sales were 76 BCF and 175 BCF for

consolidated companies and equity affiliates, respectively.

The affiliated company sales related to the dissolution of a

Hamaca equity affiliate in Venezuela.

In 2009, worldwide sales of 117 BCF were related to

consolidated companies. For the Other regions, the sale of

properties in Argentina accounted for 84 BCF. The sale of

properties in the Gulf of Mexico accounted for the majority

of the 33 BCF decrease in the United States.

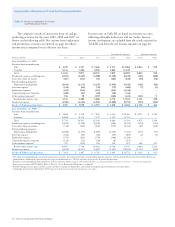

Table VI Standardized Measure of Discounted Future Net Cash

Flows Related to Proved Oil and Gas Reserves

The standardized measure of discounted future net cash

flows, related to the preceding proved oil and gas reserves, is

calculated in accordance with the requirements of the FASB.

Estimated future cash inflows from production are com-

puted by applying 12 month-average prices for oil and gas to

year-end quantities of estimated net proved reserves. Future

price changes are limited to those provided by contractual

arrangements in existence at the end of each reporting year.

Future development and production costs are those estimated

future expenditures necessary to develop and produce year-

end estimated proved reserves based on year-end cost indices,

assuming continuation of year-end economic conditions,

and include estimated costs for asset retirement obligations.

Estimated future income taxes are calculated by applying

appropriate year-end statutory tax rates. These rates reflect

allowable deductions and tax credits and are applied to

estimated future pretax net cash flows, less the tax basis of

related assets. Discounted future net cash flows are calculated

using 10 percent midperiod discount factors. Discounting

requires a year-by-year estimate of when future expenditures

will be incurred and when reserves will be produced.

The information provided does not represent manage-

ment’s estimate of the company’s expected future cash flows

or value of proved oil and gas reserves. Estimates of proved-

reserve quantities are imprecise and change over time as

new information becomes available. Moreover, probable and

possible reserves, which may become proved in the future,

are excluded from the calculations. The arbitrary valuation

prescribed by the FASB requires assumptions as to the timing

and amount of future development and production costs. The

calculations are made as of December 31 each year and should

not be relied upon as an indication of the company’s future

cash flows or value of its oil and gas reserves. In the following

table, “Standardized Measure Net Cash Flows” refers to the

standardized measure of discounted future net cash flows.