Chevron 2009 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2009 Chevron annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

|

|

Chevron Corporation 2009 Annual Report 61

FS-PB

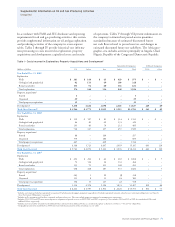

Note 21 Employee Benefit Plans – Continued

The components of net periodic benefit cost and amounts recognized in other comprehensive income for 2009, 2008 and 2007

are shown in the table below:

Pension Benefits

2009 2008 2007 Other Benefits

U.S. Int’l. U.S. Int’l. U.S. Int’l. 2009 2008 2007

Net Periodic Benefit Cost

Service cost $ 266 $ 128 $ 250 $ 132 $ 260 $ 125 $ 43 $ 44 $ 49

Interest cost 481 292 499 292 483 255 180 178 184

Expected return on plan assets (395) (203) (593) (273) (578) (266) – – –

Amortization of prior-service

(credits) costs (7) 23 (7) 24 46 17 (81) (81) (81)

Recognized actuarial losses 298 108 60 77 128 82 27 38 81

Settlement losses 141 1 306 2 65 – – – –

Curtailment losses – – – – – 3 (5) – –

Special termination benefit recognition – – – 1 – – – – –

Total net periodic benefit cost 784 349 515 255 404 216 164 179 233

Changes Recognized in Other

Comprehensive Income

Net actuarial loss (gain) during period 823 194 2,624 646 (160) 31 82 (42) (401)

Amortization of actuarial loss (439) (109) (366) (79) (193) (82) (27) (38) (81)

Prior service cost (credit) during period 1 13 – 32 (301) 97 20 – –

Amortization of prior-service

credits (costs) 7 (23) 7 (24) (46) (20) 81 81 81

Total changes recognized in

other comprehensive income 392 75 2,265 575 (700) 26 156 1 (401)

Recognized in Net Periodic

Benefit Cost and Other

Comprehensive Income $ 1,176 $ 424 $ 2,780 $ 830 $ (296) $ 242 $ 320 $ 180 $ (168)

Net actuarial losses recorded in “Accumulated other

comprehensive loss” at December 31, 2009, for the company’s

U.S. pension, international pension and OPEB plans are

being amortized on a straight-line basis over approximately

11, 13 and 10 years, respectively. These amortization periods

represent the estimated average remaining service of employ-

ees expected to receive benefits under the plans. These losses

are amortized to the extent they exceed 10 percent of the

higher of the projected benefit obligation or market-related

value of plan assets. The amount subject to amortization is

determined on a plan-by-plan basis. During 2010, the com-

pany estimates actuarial losses of $318, $102 and $26 will be

amortized from “Accumulated other comprehensive loss” for

U.S. pension, international pension and OPEB plans, respec-

tively. In addition, the company estimates an additional $220

will be recognized from “Accumulated other comprehensive

loss” during 2010 related to lump-sum settlement costs from

U.S. pension plans.

The weighted average amortization period for recognizing

prior service costs (credits) recorded in “Accumulated other

comprehensive loss” at December 31, 2009, was approximately

eight and 12 years for U.S. and international pension plans,

respectively, and eight years for other postretirement benefit

plans. During 2010, the company estimates prior service

(credits) costs of $(7), $27 and $(74) will be amortized from

“Accumulated other comprehensive loss” for U.S. pension,

international pension and OPEB plans, respectively.