Allstate 2011 Annual Report Download - page 138

Download and view the complete annual report

Please find page 138 of the 2011 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

128 -

129

129 -

130

130 -

131

131 -

132

132 -

133

133 -

134

134 -

135

135 -

136

136 -

137

137 -

138

138 -

139

139 -

140

140 -

141

141 -

142

142 -

143

143 -

144

144 -

145

145 -

146

146 -

147

147 -

148

148 -

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

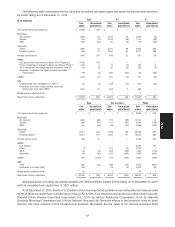

annuities and interest-sensitive life insurance. The surrender and partial withdrawal rate on deferred fixed annuities,

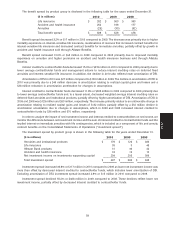

interest-sensitive life insurance products and Allstate Bank products, based on the beginning of year contractholder

funds, was 12.2% in 2010 compared to 11.8% in 2009 and 12.2% in 2008.

Net investment income decreased 6.9% or $211 million to $2.85 billion in 2010 from $3.06 billion in 2009 primarily

due to lower yields, reduced average investment balances and risk reduction actions.

Net investment income decreased 19.6% or $747 million to $3.06 billion in 2009 from $3.81 billion in 2008. The

decline was primarily due to lower yields, actions to shorten duration and maintain additional liquidity in the portfolio,

along with reduced average investment balances resulting primarily from reduced contractholder obligations.

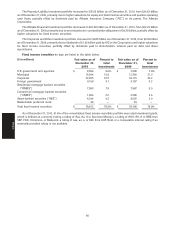

Net realized capital gains and losses are presented in the following table for the years ended December 31.

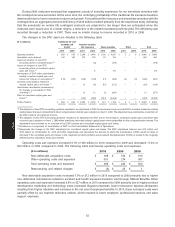

($ in millions) 2010 2009 2008

Impairment write-downs $ (501) $ (1,021) $ (1,256)

Change in intent write-downs (142) (268) (1,247)

Net other-than-temporary impairment losses

recognized in earnings (643) (1,289) (2,503)

Sales 219 638 178

Valuation of derivative instruments (94) 315 (985)

Settlements of derivative instruments (31) 41 197

EMA limited partnership income 32 (136) (14)

Realized capital gains and losses, pre-tax (517) (431) (3,127)

Income tax benefit 180 14 1,093

Realized capital gains and losses, after-tax $ (337) $ (417) $ (2,034)

For further discussion of realized capital gains and losses, see the Investments section of the MD&A.

Analysis of costs and expenses Total costs and expenses decreased 13.9% or $719 million in 2010 compared to

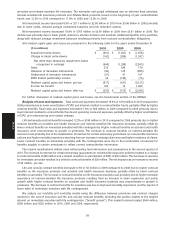

2009 primarily due to lower amortization of DAC and interest credited to contractholder funds, partially offset by higher

contract benefits. Total costs and expenses decreased 1.6% or $85 million in 2009 compared to 2008 primarily due to

lower interest credited to contractholder funds and operating costs and expenses, partially offset by higher amortization

of DAC and restructuring and related charges.

Life and annuity contract benefits increased 12.2% or $198 million in 2010 compared to 2009 primarily due to higher

contract benefits on accident and health insurance and interest-sensitive life insurance products, partially offset by

lower contract benefits on immediate annuities with life contingencies. Higher contract benefits on accident and health

insurance were proportionate to growth in premiums. The increase in contract benefits on interest-sensitive life

insurance was primarily due to the reestimation of reserves for certain secondary guarantees on universal life insurance

policies and higher mortality experience resulting from an increase in average claim size and higher incidence of claims.

Lower contract benefits on immediate annuities with life contingencies were due to the reestimation of reserves for

benefits payable to certain annuitants to reflect current contractholder information.

The reserve reestimations utilized more refined policy level information and assumptions in the second quarter of

2010. The increase in reserves for certain secondary guarantees on universal life insurance policies resulted in a charge

to contract benefits of $68 million and a related reduction in amortization of DAC of $50 million. The decrease in reserves

for immediate annuities resulted in a credit to contract benefits of $26 million. The net impact was an increase to income

of $8 million, pre-tax.

Life and annuity contract benefits increased 0.3% or $5 million in 2009 compared to 2008 due to higher contract

benefits on life insurance products and accident and health insurance business, partially offset by lower contract

benefits on annuities. The increase in contract benefits on life insurance products was primarily due to higher mortality

experience on interest-sensitive life insurance products resulting from an increase in claim experience and policy

growth while higher contract benefits on accident and health insurance business was proportionate to growth in

premiums. The decrease in contract benefits for annuities was due to improved mortality experience and the impact of

lower sales of immediate annuities with life contingencies.

We analyze our mortality and morbidity results using the difference between premiums and contract charges

earned for the cost of insurance and life and annuity contract benefits excluding the portion related to the implied

interest on immediate annuities with life contingencies (‘‘benefit spread’’). This implied interest totaled $549 million,

$558 million and $552 million in 2010, 2009 and 2008, respectively.

58

MD&A