Allstate 2011 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2011 Allstate annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

-

260

-

261

-

262

-

263

-

264

-

265

-

266

-

267

-

268

-

269

-

270

-

271

-

272

-

273

-

274

-

275

-

276

|

|

• Factors comprising the Allstate brand standard auto loss ratio increase of 1.4 points to 70.7 in 2010 from 69.3 in

2009 were the following:

– 2.0% increase in standard auto claim frequency for property damage in 2010 compared to 2009

– 6.2% increase in standard auto claim frequency for bodily injury in 2010 compared to 2009

– 0.5% decrease in auto paid claim severities for property damage in 2010 compared to 2009

– 0.3% decrease in auto paid claim severities for bodily injury in 2010 compared to 2009

• Factors comprising the Allstate brand homeowners loss ratio, which includes catastrophes, increase of 2.5 points to

82.1 in 2010 from 79.6 in 2009 were the following:

– 2.3 point increase in the effect of catastrophe losses to 31.3 points in 2010 compared to 29.0 points in 2009

– 1.1% decrease in homeowner claim frequency, excluding catastrophes, in 2010 compared to 2009

– 1.6% increase in paid claim severity, excluding catastrophes, in 2010 compared to 2009

• Factors comprising the $138 million increase in catastrophe losses to $2.21 billion in 2010 compared to $2.07 billion

in 2009 were the following:

– 90 events with losses of $2.37 billion in 2010 compared to 82 events with losses of $2.24 billion in 2009

– $163 million favorable prior year reserve reestimates in 2010 compared to $169 million favorable reserve

reestimates in 2009

• Factors comprising prior year reserve reestimates of $159 million favorable in 2010 compared to $112 million

favorable in 2009 included:

– prior year reserve reestimates related to auto, homeowners and other personal lines in 2010 contributed

$179 million favorable, $23 million favorable and $15 million unfavorable, respectively, compared to prior year

reserve reestimates in 2009 of $57 million favorable, $168 million favorable and $89 million unfavorable,

respectively

– prior year reestimates in 2010 are attributable to favorable prior year catastrophe reestimates and severity

development that was better than expected, partially offset by litigation settlements

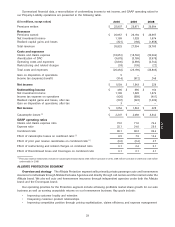

• Property-Liability underwriting income was $495 million in 2010 compared to $995 million in 2009. Underwriting

income, a measure not based on GAAP, is defined below.

• Property-Liability investments as of December 31, 2010 were $35.05 billion, an increase of 1.5% from $34.53 billion

as of December 31, 2009. Net investment income was $1.19 billion in 2010, a decrease of 10.5% from $1.33 billion in

2009.

• Net realized capital losses were $321 million in 2010 compared to $168 million in 2009.

PROPERTY-LIABILITY OPERATIONS

Overview Our Property-Liability operations consist of two business segments: Allstate Protection and

Discontinued Lines and Coverages. Allstate Protection comprises two brands, the Allstate brand and Encompass姞

brand. Allstate Protection is principally engaged in the sale of personal property and casualty insurance, primarily

private passenger auto and homeowners insurance, to individuals in the United States and Canada. Discontinued Lines

and Coverages includes results from insurance coverage that we no longer write and results for certain commercial and

other businesses in run-off. These segments are consistent with the groupings of financial information that

management uses to evaluate performance and to determine the allocation of resources.

Underwriting income, a measure that is not based on GAAP and is reconciled to net income below, is calculated as

premiums earned, less claims and claims expense (‘‘losses’’), amortization of DAC, operating costs and expenses and

restructuring and related charges, as determined using GAAP. We use this measure in our evaluation of results of

operations to analyze the profitability of the Property-Liability insurance operations separately from investment results.

It is also an integral component of incentive compensation. It is useful for investors to evaluate the components of

income separately and in the aggregate when reviewing performance. Net income is the GAAP measure most directly

comparable to underwriting income. Underwriting income should not be considered as a substitute for net income and

does not reflect the overall profitability of the business.

The table below includes GAAP operating ratios we use to measure our profitability. We believe that they enhance

an investor’s understanding of our profitability. They are calculated as follows:

• Claims and claims expense (‘‘loss’’) ratio – the ratio of claims and claims expense to premiums earned. Loss ratios

include the impact of catastrophe losses.

• Expense ratio – the ratio of amortization of DAC, operating costs and expenses, and restructuring and related

charges to premiums earned.

• Combined ratio – the ratio of claims and claims expense, amortization of DAC, operating costs and expenses, and

restructuring and related charges to premiums earned. The combined ratio is the sum of the loss ratio and the

27

MD&A