Volvo 2003 Annual Report Download - page 71

Download and view the complete annual report

Please find page 71 of the 2003 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

|

|

69

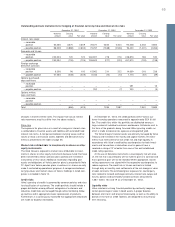

January 1, 2003 December 31, 2003

Carrying value 1Fair value 2Carrying value 1Fair value 2

Available for sale

Marketable securities 422 422 446 446

Shares and convertible debenture loan 27,338 17,575 22,963 20,648

Trading 16,130 16,080 19,083 19,072

1In accordance with Swedish GAAP.

2 For the purpose of these disclosures, fair values have been based upon quoted market prices for listed securities.

The carrying values and fair values for these securities were distributed as follows:

D. Restructuring costs. Up to and including 2000, restructuring

costs were in the Volvo Group’s year-end accounts reported in the

year that implementation of these measures was approved by each

company’s Board of Directors. In accordance with US GAAP, costs

were reported for restructuring measures only under the condition

that a sufficiently detailed plan for implementation of the measures is

prepared at the end of the accounting period. Effective in 2001,

Volvo adopted a new Swedish accounting standard, RR 16

Provisions, contingent liabilities and contingent assets, which was

substantially equivalent to US GAAP at that time. As from 2003,

when SFAS 146 “Accounting for Costs Associated with Exit or

Disposal Activities” became effective under US GAAP, there are

again differences compared to Swedish GAAP regarding the timing

of when restructuring costs should be recognized in the income

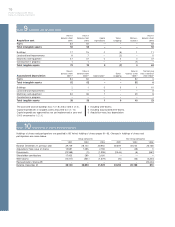

SFAS 115- SFAS 115-

Summary of debt and equity securities adjustment, Income adjustment,

available for sale and trading Carrying value 1Fair value 2gross taxes net

Trading, December 31, 2003 19,083 19,072 (11) 3 (8)

Trading, January 1, 2003 16,130 16,080 (50) 14 (36)

Change 2003 39 (11) 28

Available for sale

Marketable securities 446 446 – – –

Shares and convertible debenture loan 22,963 20,648 (2,315) (29) (2,344)

Available for sale

December 31, 2003 23,409 21,094 (2,315) (29) (2,344)

January 1, 2003 27,760 17,997 (9,763) 22 (9,741)

Change 2003 37,448 (51) 7,397

statement. However, no differences has been identified in relation to

business transactions during 2003.

E. Provisions for post-employment benefits. Effective in 2003,

provisions for post-employment benefits in Volvo’s consolidated

financial statements are accounted for in accordance with RR 29

Employee benefits, which conforms in all significant respects with

IAS 19 Employee Benefits. See further in Note 1 and 22. In accord-

ance with US GAAP, post-employment benefits should be accounted

for in accordance with SFAS 87, “Employers Accounting for

Pensions” and SFAS 106, “Employers’ Accounting for Post-retire-

ment Benefits Other than Pensions”. The differences between Volvo’s

accounting principles and US GAAP pertain to different transition

dates, recognition of past service costs and minimum liability

adjustments.

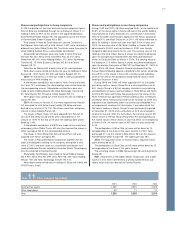

Net periodical costs for post-employment benefits 2001 2002 2003

Net periodical costs in accordance with Swedish accounting principles 3,910 5,087 4,424

Net periodical costs in accordance with US GAAP 3,454 4,418 5,075

Adjustment of this year’s income in accordance

with US GAAP, before income taxes 456 669 (651)

Net provisions for post-employment benefits Dec 31, 2001 Dec 31, 2002 Dec 31, 2003

Net provisions for post-employment benefits in accordance

with Swedish accounting principles (13,877) (15,528) (15,094)

Difference in actuarial methods (284) 170 –

Unrecognized actuarial (gains) and losses 1,154 1,350 5,296

Unrecognized transition (assets) and obligations according to SFAS 87, net (52) (33) (29)

Unrecognized past service costs – – 659

Minimum liability adjustments (546) (1,507) (4,268)

Net provisions for post-employment benefits in accordance with US GAAP (13,605) (15,548) (13,436)

The projected benefit obligation, accumulated benefit obligation and

fair value of plan assets for the pension plans with an accumulated

benefit obligation in excess of plan assets were 18,867; 18,340 and

13,475 at December 31, 2003.

1In accordance with Swedish GAAP.

2 For the purpose of these disclosures, fair values have been based upon

quoted market prices for listed securities.

3 Of the net SFAS 115 adjustment during 2003, 3,969 has been reported as

an increase of net income in accordance with US GAAP and 3,428 has

been reported in Other comprehensive income.