Volvo 2003 Annual Report Download - page 39

Download and view the complete annual report

Please find page 39 of the 2003 Volvo annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

|

|

37

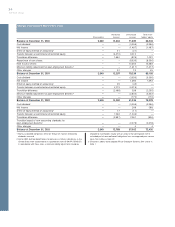

accordance with the principles set forth in the Recommendation of

the Swedish Financial Accounting Standards Council, RR 1:00,

Consolidated Financial Statements and Business Combinations.

All business combinations are accounted for in accordance with

the purchase method.

Companies that have been divested are included in the consolidat-

ed financial statements up to and including the date of divestment.

Companies acquired during the year are consolidated as of the date

of acquisition.

Joint ventures are preferably reported by use of the proportionate

method of consolidation. A few joint ventures are reported by use of

the equity method due to practical reasons.

Holdings in associated companies are reported in accordance

with the equity method. The Group’s share of reported income after

financial items in such companies, adjusted for minority interests, is

included in the consolidated income statement in Income from

investments in associated companies, reduced in appropriate cases

by amortization of goodwill. The Group’s share of reported taxes in

associated companies, is included in Group income tax expense.

For practical reasons, most of the associated companies are

included in the consolidated accounts with a certain time lag, nor-

mally one quarter. Dividends from associated companies are not

included in consolidated income. In the consolidated balance sheet,

the book value of shareholdings in associated companies is affected

by Volvo’s share of the company’s net income, reduced by the amort-

ization of goodwill and by the amount of dividends received.

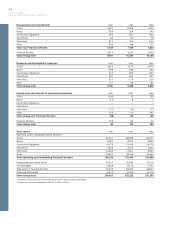

Accounting for hedges

Loans and other financial instruments used to hedge an underlying

position are reported as hedges. In order to apply hedge accounting,

the following criteria must be met: the position being hedged is iden-

tified and exposed to exchange-rate or interest-rate movements, the

purpose of the loan/ instrument is to serve as a hedge and the hedg-

ing effectively protects the underlying position against changes in

the market rates. Financial instruments used for the purpose of

hedging future currency flows are accounted for as hedges if the

currency flows are considered probable to occur.

Foreign currencies

In preparing the consolidated financial statements, all items in the

income statements of foreign subsidiaries and joint ventures (except

subsidiaries in highly inflationary economies) are translated to Swedish

kronor at the average exchange rates during the year (average rate).

All balance sheet items except net income are translated at ex-

change rates at the respective year-ends (year-end rate). The differ-

ences in consolidated shareholders’ equity arising as a result of vari-

ations between year-end exchange rates are charged or credited

directly to shareholders’ equity and classified as restricted or un-

restricted reserves. The difference arising in the consolidated bal-

ance sheet as a result of the translation of net income, in the income

statements, in foreign subsidiaries’ to Swedish kronor at average

rates, and in the balance sheets at year-end rate, is charged or

credited to unrestricted reserves. Movements in exchange rates

change the book value of foreign associated companies. This differ-

ence affects restricted reserves directly.

When foreign subsidiaries, joint ventures and associated compa-

nies are divested, the accumulated translation difference is reported

as a realized gain/ loss and, accordingly, affects the capital gain.

Financial statements of subsidiaries operating in highly inflationary

economies are translated to Swedish kronor using the monetary

method. Monetary items in the balance sheet are translated at year-

end rates and nonmonetary balance sheet items and corresponding

income statement items are translated at rates in effect at the time

of acquisition (historical rates). Other income statement items are

translated at average rates. Translation differences are credited to, or

charged against, income in the year in which they arise.

In the individual Group companies as well as in the consolidated

accounts, receivables and liabilities in foreign currency are valued at

period-end exchange rates.

Gains and losses pertaining to hedges are reported at the same

time as gains and losses of the items hedged. Received premiums or

payments for currency options, which hedge currency flows in busi-

ness transactions, are reported as income/ expense during the con-

tract period.

Gains/ losses on outstanding currency futures at year-end, which

were entered into to hedge future commercial currency flows, are

reported at the same time as the commercial flow is realized. For

other currency futures that do not fullfil the criteria for hedge

accounting a full market valuation is made on a portfolio basis and

are credited to, or charged against, income.

In valuing financial assets and liabilities whose original currency

denomination has been changed as a result of currency swap con-

tracts, the loan amount is accounted for translated to Swedish kro-

nor at the period-end exchange rate. Unrealized exchange rate gains

relating to swap contracts are reported among short-term receiv-

ables and unrealized exchange rate losses relating to swap contracts

are reported among current liabilities.

Exchange rate differences on loans and other financial instru-

ments in foreign currency, which are used to hedge net assets in for-

eign subsidiaries and associated companies, are offset against trans-

lation differences in the shareholders’ equity of the respective com-

panies.

Exchange rate gains and losses on payments during the year and

on the valuation of assets and liabilities in foreign currencies at year-

end are credited to, or charged against, income in the year they arise.

The more important exchange rates employed are shown above.

Other financial instruments

Interest-rate contracts and forward exchange rate contracts are used

to change the underlying financial asset and debt structure and are

reported as hedges against such assets and debts.

Interest-rate contracts used as part of the management of the

Group’s short-term investments are valued together with these

investments in accordance with the portfolio method. Provisions are

made for unrealized losses in excess of the unrealized gains within

the portfolio.

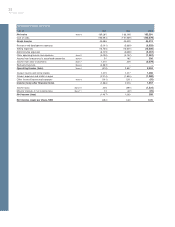

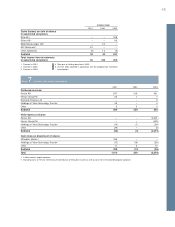

Exchange rates Average rate Year-end rate

Country Currency 2001 2002 2003 2001 2002 2003

Denmark DKK 1.2403 1.2326 1.2281 1.2670 1.2386 1.2226

Japan JPY 0.0850 0.0779 0.0697 0.0813 0.0740 0.0681

Norway NOK 1.1485 1.2205 1.1418 1.1840 1.2605 1.0815

Great Britain GBP 14.8763 14.5816 13.2023 15.4800 14.1538 12.9188

United States USD 10.3272 9.7287 8.0778 10.6700 8.8263 7.2763

Canada CAD 6.6721 6.1965 5.7688 6.6923 5.6335 5.5610

Euro EUR 9.2434 9.1596 9.1258 9.4240 9.2018 9.1033