The Hartford 2015 Annual Report Download - page 89

Download and view the complete annual report

Please find page 89 of the 2015 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

|

|

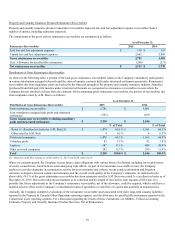

89

Natural Catastrophe Risk

Natural catastrophe risk is defined as the exposure arising from natural phenomena (e.g., weather, earthquakes, wildfires, etc.) that create

a concentration or aggregation of loss across the Company's insurance or asset portfolios. The Company uses both internal and third-

party models to estimate the potential loss resulting from various catastrophe events and the potential financial impact those events

would have on the Company's financial position and results of operations across the property-casualty, group life, disability, and asset

management businesses. For natural catastrophe perils, the Company's modeled loss estimates are derived by averaging 21 modeled loss

events representing a 250 year return. The Company generally limits its estimated pre-tax loss as a result of natural catastrophes for

property & casualty exposures from a single 250-year event to less than 30% of statutory surplus of the property and casualty insurance

subsidiaries prior to reinsurance and to less than 15% of statutory surplus of the property and casualty insurance subsidiaries after

reinsurance. While Enterprise Risk Management has a process to track and manage these limits, from time to time the estimated loss to

natural catastrophes from a single 250-year event prior to reinsurance may fluctuate above or below these limits due to changes in

modeled loss estimates, exposures or statutory surplus.

For the peril of earthquake, the 21 events averaged to determine the modeled loss estimate include events occurring in California as well

as the Northeastern, Southeastern, Northwestern, Midwestern, New Madrid and Great Lakes regions of the United States with associated

magnitudes ranging from 7.1 to 9.2 on the Moment Magnitude scale. The estimated 250 year pre-tax probable maximum loss from

earthquake events is estimated to be $810 before reinsurance and $494 net of reinsurance. For the peril of hurricane, the 21 events

averaged to determine the modeled loss estimate include category 1 through 5 events in Florida, as well as Mid Atlantic, Northeastern

and Texas region landfalls. The estimated 250 year pre-tax probable maximum losses from hurricane events are estimated to be

$1.5 billion and $685, before and after reinsurance, respectively. The loss estimates represent total property losses for hurricane events

and property and workers compensation losses for earthquake events resulting from a single event. The estimates provided are based on

250-year return period loss estimates that have a 0.4% likelihood of being exceeded in any single year.

The net loss estimates provided above assume that the Company is able to recover all losses ceded to reinsurers under its reinsurance

programs. There are various methodologies used in the industry to estimate the potential property and workers compensation losses that

would arise from various catastrophe events and companies may use different models and assumptions in their estimates. Therefore, the

Company's estimates of gross and net losses arising from a 250-year hurricane or earthquake event may not be comparable to estimates

provided by other companies. Furthermore, the Company's estimates are subject to significant uncertainty and could vary materially

from the actual losses that would arise from these events and the loss estimates provided by other companies. The Company also

manages natural catastrophe risk for group life and group disability, which in combination with property and workers compensation loss

estimates are subject to separate enterprise risk management net aggregate loss limits as a percent of enterprise surplus.

Terrorism Risk

The Company defines terrorism risk as the risk of losses from terrorist attacks, including losses caused by single-site and multi-site

conventional attacks, as well as the potential for attacks using nuclear, biological, chemical or radiological weapons (“NBCR”). The

Company monitors aggregations of terrorism risk exposure around key landmarks primarily in major metropolitan areas that span the

Company's insurance portfolio. ERM limits for terrorism apply to aggregations of risk across property-casualty, group benefits and

specific asset portfolios and are defined based on a deterministic, single-site conventional terrorism attack scenario. The Company

manages its potential estimated loss from a conventional terrorism loss scenario up to $1.7 billion gross of reinsurance and before

coverage under TRIPRA. In addition, the Company monitors exposures monthly and employs both internally developed and vendor-

licensed loss modeling tools as part of its risk management discipline. While our modeled exposures to conventional terrorist attacks

around landmark locations may fluctuate above and below $1.7 billion, currently, all such terrorism exposures are within ERM limits.

For a discussion on risks related to terrorist attacks, see the risk factor, "The occurrence of one or more terrorist attacks in the geographic

areas we serve or the threat of terrorism in general may have a material adverse effect on our business, financial condition, results of

operations and liquidity."