The Hartford 2015 Annual Report Download - page 158

Download and view the complete annual report

Please find page 158 of the 2015 The Hartford annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

148 -

149

149 -

150

150 -

151

151 -

152

152 -

153

153 -

154

154 -

155

155 -

156

156 -

157

157 -

158

158 -

159

159 -

160

160 -

161

161 -

162

162 -

163

163 -

164

164 -

165

165 -

166

166 -

167

167 -

168

168 -

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

|

|

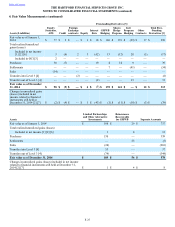

Table of Contents THE HARTFORD FINANCIAL SERVICES GROUP, INC.

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (continued)

4. Fair Value Measurements (continued)

F-27

The Securities Working Group performs ongoing analyses of the prices and credit spreads received from third parties to ensure that the

prices represent a reasonable estimate of the fair value. This process involves quantitative and qualitative analysis and is overseen by

investment and accounting professionals. As a part of these analyses, the Company considers trading volume, new issuance activity and

other factors to determine whether the market activity is significantly different than normal activity in an active market, and if so,

whether transactions may not be orderly considering the weight of available evidence. If the available evidence indicates that pricing is

based upon transactions that are stale or not orderly, the Company places little, if any, weight on the transaction price and will estimate

fair value utilizing an internal pricing model. In addition, the Company ensures that prices received from independent brokers represent a

reasonable estimate of fair value through the use of internal and external cash flow models utilizing spreads, and when available, market

indices. As a result of this analysis, if the Company determines that there is a more appropriate fair value based upon the available

market data, the price received from the third party is adjusted accordingly and approved by the Valuation Committee.

The Company conducts other specific monitoring controls around pricing. Daily analyses identify price changes over 3% for fixed

maturities and 5% for equity securities and trade prices for both debt and equity securities that differ over 3% to the current day's price.

Weekly analyses identify prices that differ more than 5% from published bond prices of a corporate bond index. Monthly analyses

identify price changes over 3%, prices that have not changed, and missing prices. Also on a monthly basis, a second source validation is

performed on most sectors. Analyses are conducted by a dedicated pricing unit that follows up with trading and investment sector

professionals and challenges prices with vendors when the estimated assumptions used differ from what the Company feels a market

participant would use. Examples of other procedures performed include, but are not limited to, initial and on-going review of third-party

pricing services’ methodologies, review of pricing statistics and trends, and back testing recent trades.

The Company has analyzed the third-party pricing services’ valuation methodologies and related inputs, and has also evaluated the

various types of securities in its investment portfolio to determine an appropriate fair value hierarchy level based upon trading activity

and the observability of market inputs. Most prices provided by third-party pricing services are classified into Level 2 because the inputs

used in pricing the securities are observable. Due to the lack of transparency in the process that brokers use to develop prices, most

valuations that are based on brokers’ prices are classified as Level 3. Some valuations may be classified as Level 2 if the price can be

corroborated with observable market data.

Derivative Instruments, including Embedded Derivatives within Investments

Derivative instruments are fair valued using pricing valuation models for OTC derivatives that utilize independent market data inputs,

quoted market prices for exchange-traded and OTC-cleared derivatives, or independent broker quotations. Excluding embedded and

reinsurance related derivatives, as of December 31, 2015 and 2014, 96% and 96%, respectively, of derivatives, based upon notional

values, were priced by valuation models, including discounted cash flow models and option-pricing models that utilize present value

techniques, or quoted market prices. The remaining derivatives were priced by broker quotations.

The Derivatives Working Group performs ongoing analyses of the valuations, assumptions and methodologies used to ensure that the

prices represent a reasonable estimate of the fair value. The Company performs various controls on derivative valuations which include

both quantitative and qualitative analyses. Analyses are conducted by a dedicated derivative pricing team that works directly with

investment sector professionals to analyze impacts of changes in the market environment and investigate variances. On a daily basis,

market valuations are compared to counterparty valuations for OTC derivatives. There are monthly analyses to identify market value

changes greater than pre-defined thresholds, stale prices, missing prices, and zero prices. Also on a monthly basis, a second source

validation, typically to broker quotations, is performed for certain of the more complex derivatives and all new deals during the month. A

model validation review is performed on any new models, which typically includes detailed documentation and validation to a second

source. The model validation documentation and results of validation are presented to the Valuation Committee for approval. There is a

monthly control to review changes in pricing sources to ensure that new models are not moved to production until formally approved.

The Company utilizes derivative instruments to manage the risk associated with certain assets and liabilities. However, the derivative

instrument may not be classified with the same fair value hierarchy level as the associated assets and liabilities. Therefore, the realized

and unrealized gains and losses on derivatives reported in the Level 3 rollforward may be offset by realized and unrealized gains and

losses of the associated assets and liabilities in other line items of the financial statements.