Starwood 2010 Annual Report Download - page 105

Download and view the complete annual report

Please find page 105 of the 2010 Starwood annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

|

|

ASU Nos. 2009-16 and 2009-17 on January 1, 2010 and, as a result, at December 31, 2010 we had $494 million of

non-recourse debt and $19 million of restricted cash associated with securitized vacation ownership receivables.

Including this debt and restricted cash associated with securitized vacation ownership receivables, our net debt was

$2.535 billion at December 31, 2010.

Our Facilities are used to fund general corporate cash needs. As of December 31, 2010, we have availability of

over $1.4 billion under the Facilities. We have reviewed the financial covenants associated with our Facilities, the

most restrictive being the leverage ratio. As of December 31, 2010, we were in compliance with this covenant and

expect to remain in compliance through the end of 2011. We have the ability to manage the business in order to

reduce our leverage ratio by reducing operating costs, selling, general and administrative costs and postponing

discretionary capital expenditures. However, there can be no assurance that we will stay below the required leverage

ratio if the current economic climate deteriorates.

Based upon the current level of operations, management believes that our cash flow from operations and asset sales,

together with our significant cash balances (approximately $816 million at December 31, 2010, including $63 million of

short-term and long-term restricted cash), available borrowings under the Facilities and other bank credit facilities

(approximately $1.4 billion at December 31, 2010), and capacity for additional borrowings will be adequate to meet

anticipated requirements for scheduled maturities, dividends, working capital, capital expenditures, marketing and

advertising program expenditures, other discretionary investments, interest and scheduled principal payments and share

repurchases for the foreseeable future. However, there can be no assurance that we will be able to refinance our

indebtedness as it becomes due and, if refinanced, on favorable terms. In addition, there can be no assurance that in our

continuing business we will generate cash flow at or above historical levels, that currently anticipated results will be

achieved or that we will be able to complete dispositions on commercially reasonable terms or at all.

If we are unable to generate sufficient cash flow from operations in the future to service our debt, we may be

required to sell additional assets at lower than preferred amounts, reduce capital expenditures, refinance all or a

portion of our existing debt or obtain additional financing at unfavorable rates. Our ability to make scheduled

principal payments, to pay interest on or to refinance our indebtedness depends on our future performance and

financial results, which, to a certain extent, are subject to general conditions in or affecting the hotel and vacation

ownership industries and to general economic, political, financial, competitive, legislative and regulatory factors

beyond our control.

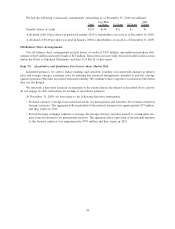

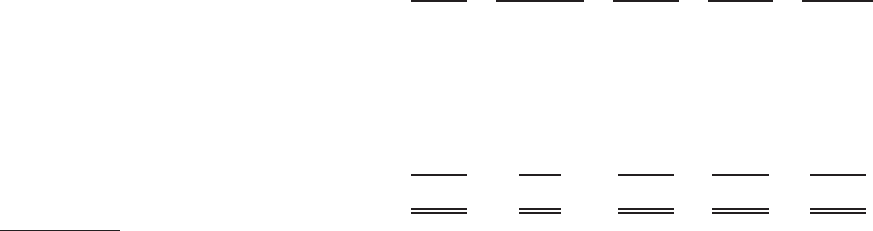

We had the following contractual obligations (1) outstanding as of December 31, 2010 (in millions):

Total

Due in Less

Than 1 Year

Due in

1-3 Years

Due in

3-5 Years

Due After

5 Years

Debt

(2)

........................... $2,855 $ 9 $1,210 $ 951 $ 685

Interest payable .................... 890 208 322 204 156

Capital lease obligations

(3)

............ 2 — — — 2

Operating lease obligations

(4)

.......... 1,345 96 161 149 939

Unconditional purchase obligations

(5)

.... 225 69 124 28 4

Other long-term obligations ........... 3 2 1 — —

Total contractual obligations ........... $5,320 $384 $1,818 $1,332 $1,786

(1) The table below excludes unrecognized tax benefits that would require cash outlays for $341 million, the timing

of which is uncertain. Refer to Note 15 of the consolidated financial statements for additional discussion on this

matter. In addition, the table excludes amounts related to the construction of our St. Regis Bal Harbour project

that has a total project cost of $750 million, of which $532 million has been paid through December 31, 2010.

(2) Excludes securitized debt of $494 million, all of which is non-recourse.

(3) Excludes sublease income of $2 million.

(4) Excludes sublease income of $13 million.

(5) Included in these balances are commitments that may be reimbursed or satisfied by our managed and franchised

properties.

37