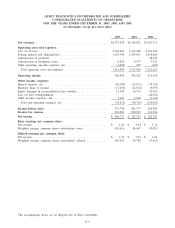

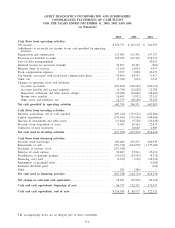

Quest Diagnostics 2003 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2003 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

|

|

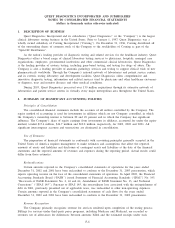

QUEST DIAGNOSTICS INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS—CONTINUED

(dollars in thousands unless otherwise indicated)

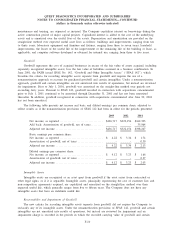

Investments

The Company accounts for investments in equity securities, which are included in “other assets’’ in

conformity with SFAS No. 115, “Accounting for Certain Investments in Debt and Equity Securities’’, which

requires the use of fair value accounting for trading or available-for-sale securities. Both realized and unrealized

gains and losses for trading securities are recorded currently in earnings as a component of non-operating

expenses within “other income (expense), net’’ in the consolidated statements of operations. Unrealized gains

and losses for available-for-sale securities are recorded as a component of accumulated other comprehensive

income (loss) within stockholders’ equity. Gains and losses on securities sold are based on the average cost

method.

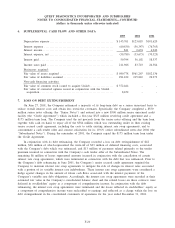

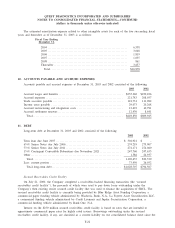

Investments at December 31, 2003 and 2002 consisted of the following:

2003 2002

Available-for-sale equity securities ..................................... $26,195 $ 5,692

Trading equity securities .............................................. 19,168 14,808

Other investments .................................................... 12,598 9,744

Total .............................................................. $57,961 $30,244

Investments in available-for-sale equity securities consist primarily of equity securities in public

corporations. Investments in trading equity securities represent participant directed investments of deferred

employee compensation and related Company matching contributions held in a trust pursuant to the Company’s

supplemental deferred compensation plan (see Note 13). Other investments do not have readily determinable fair

values and consist primarily of investments in preferred and common shares of privately held companies.

As of December 31, 2003 and 2002, the Company had gross unrealized gains (losses) from available-for-

sale equity securities of $15.5 million and $(6.6) million, respectively. “Other income (expense), net’’ for the

year ended December 31, 2001 included a gain of $6.3 million associated with the sale of certain available-for-

sale equity securities. For the years ended December 31, 2003, 2002 and 2001, gains (losses) from trading

equity securities totaled $1.9 million, $(1.0) million and $(0.1) million, respectively, and are included in “other

income (expense), net’’ within the consolidated statements of operations.

Financial Instruments

The Company’s policy for managing exposure to market risks may include the use of financial instruments,

including derivatives. The Company has established a control environment that includes policies and procedures

for risk assessment and the approval, reporting and monitoring of derivative financial instrument activities. These

policies prohibit holding or issuing derivative financial instruments for trading purposes.

SFAS No. 133, “Accounting for Derivative Instruments and Hedging Activities’’ (“SFAS 133’’), as

amended, requires that all derivative instruments be recorded on the balance sheet at their fair value. Changes in

the fair value of derivatives are recorded each period in current earnings or other comprehensive income,

depending on whether a derivative is designated as part of a hedge transaction and, if it is, the type of hedge

transaction. Effective January 1, 2001, the Company adopted SFAS 133, as amended. The cumulative effect of

the change in accounting for derivative financial instruments upon adoption on January 1, 2001 of SFAS 133, as

amended, reduced comprehensive income by approximately $1 million.

Fair Value of Financial Instruments

The carrying amounts of cash and cash equivalents, accounts receivable and accounts payable and accrued

expenses approximate fair value based on the short maturity of these instruments. At December 31, 2003 and

2002, the fair value of the Company’s debt was estimated at $1.2 billion and $899 million, respectively, using

quoted market prices and yields for the same or similar types of borrowings, taking into account the underlying

terms of the debt instruments. At December 31, 2003 and 2002, the estimated fair value exceeded the carrying

value of the debt by $86 million and $77 million, respectively.

F-12