Quest Diagnostics 2003 Annual Report Download - page 57

Download and view the complete annual report

Please find page 57 of the 2003 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

|

|

various liability insurance programs for claims that could result from providing or failing to provide clinical

laboratory testing services, including inaccurate testing results and other exposures. Our insurance coverage

limits our maximum exposure on individual claims; however, we are essentially self-insured for a significant

portion of these claims. While the basis for claims reserves incorporates actuarially determined losses based

upon our historical and projected loss experience, the process of analyzing, assessing and establishing reserve

estimates relative to these types of claims involves a high degree of judgment. Changes in the facts and

circumstances associated with a claim could have a material impact on our results of operations, principally

costs of services, and cash flows in the period that reserve estimates are revised. We believe that present

insurance coverage and reserves are sufficient to cover currently estimated exposures, but we cannot assure

investors that we will not incur liabilities in excess of recorded reserves. Similarly, although we believe that we

will be able to obtain adequate insurance coverage in the future at acceptable costs, we cannot assure investors

that we will be able to do so.

Billing-related settlement reserves

Our business is subject to extensive and frequently changing federal, state and local laws and regulations.

We have entered into several settlement agreements with various government and private payers during recent

years relating to industry-wide billing and marketing practices that had been substantially discontinued by early

1993. In addition, we are aware of several pending lawsuits filed under the qui tam provisions of the civil False

Claims Act and have received notices of private claims relating to billing issues similar to those that were the

subject of prior settlements with various government payers. We have a comprehensive compliance program that

is intended to ensure the strict implementation and observance of all applicable laws, regulations and Company

policies. The Quality, Safety and Compliance Committee of the Board of Directors requires periodic reporting

of compliance operations from management. As an integral part of our compliance program, we investigate all

reported or suspected failures to comply with federal healthcare reimbursement requirements. Any

non-compliance that results in Medicare or Medicaid overpayments is reported to the government and

reimbursed by us. As a result of these efforts, we have periodically identified and reported overpayments. While

we have reimbursed these overpayments and have taken corrective action where appropriate, we cannot assure

investors that in each instance the government will necessarily accept these actions as sufficient.

While we believe that we are in material compliance with all applicable laws, many of the regulations

applicable to us, including those relating to billing and reimbursement of tests and those relating to relationships

with physicians and hospitals, are vague or indefinite and have not been interpreted by the courts. They may be

interpreted or applied by a prosecutorial, regulatory or judicial authority in a manner that could require us to

make changes in our operations, including our billing practices. If we fail to comply with applicable laws and

regulations, we could suffer civil and criminal penalties, including the loss of licenses or our ability to

participate in Medicare, Medicaid and other federal and state healthcare programs.

Although management believes that established reserves for billing-related claims are sufficient, it is

possible that additional information (such as the indication by the government of criminal activity, additional

tests being questioned or other changes in the government’s or private claimants’ theories of wrongdoing) may

become available which may cause the final resolution of these matters to exceed established reserves by an

amount which could be material to our results of operations and cash flows in the period in which such claims

are settled. We do not believe that these issues will have a material adverse effect on our overall financial

condition.

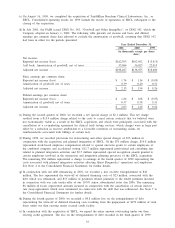

Accounting for and recoverability of goodwill

In July 2001, the Financial Accounting Standards Board, or FASB, issued Statement of Financial

Accounting Standards, or SFAS, No. 142, “Goodwill and Other Intangible Assets’’, or SFAS 142. The impact of

adopting SFAS 142 is summarized in Note 2 to the Consolidated Financial Statements.

Effective January 1, 2002, we evaluate the recoverability and measure the potential impairment of our

goodwill under SFAS 142. The annual impairment test is a two-step process that begins with the estimation of

the fair value of the reporting unit. The first step screens for potential impairment and the second step measures

the amount of the impairment, if any. Our estimate of fair value considers publicly available information

regarding the market capitalization of our Company, as well as (i) publicly available information regarding

comparable publicly-traded companies in the clinical laboratory testing industry, (ii) the financial projections and

future prospects of our business, including its growth opportunities and likely operational improvements, and

(iii) comparable sales prices, if available. As part of the first step to assess potential impairment, we compare

40