Quest Diagnostics 2003 Annual Report Download - page 63

Download and view the complete annual report

Please find page 63 of the 2003 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

|

|

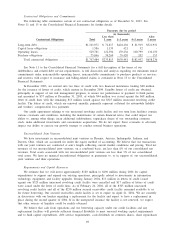

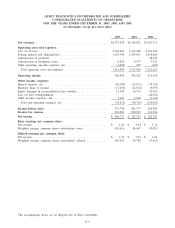

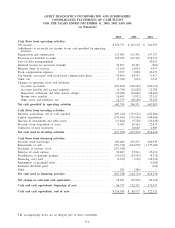

In 2001, we refinanced a majority of our long-term debt on a senior unsecured basis. Specifically, we

completed a $550 million senior notes offering, or the Senior Notes, and entered into a new $500 million

senior unsecured credit facility, or the Credit Agreement, which included a five-year $325 million revolving

credit agreement and a $175 million term loan. We used the net proceeds from the senior notes offering and

the term loan, together with cash on hand, to repay all of the $584 million which was outstanding under our

then existing senior secured credit agreement, including the costs to settle existing interest rate swap agreements,

and to consummate a cash tender offer of our 10

3

⁄

4

% senior subordinated notes due 2006, or the Subordinated

Notes. In conjunction with our debt refinancing, we recorded a loss on debt extinguishment of $42 million, $36

million of which represented the write-off of $23 million of deferred financing costs, associated with the debt

which was refinanced, and $13 million of payments related primarily to the tender premium incurred in

connection with our cash tender offer for our Subordinated Notes. The remaining $6 million of losses

represented amounts incurred in conjunction with the cancellation of certain interest rate swap agreements,

which were terminated in connection with the debt that was refinanced. Prior to our debt refinancing, our

secured credit agreement required us to maintain interest rate swap agreements to mitigate the risk of changes

in interest rates associated with a portion of our variable interest rate indebtedness.

Other income (expense), net, represents miscellaneous income and expense items related to non-operating

activities, such as gains and losses associated with investments and other non-operating assets. For the year

ended December 31, 2002, other income (expense), net includes a $4.9 million pretax gain on the sale of

certain assets, partially offset by losses on miscellaneous non-operating assets. For the year ended December 31,

2001, other income (expense), net includes the net impact of writing-off $9.6 million of certain impaired assets,

partially offset by a $6.3 million gain on the sale of an investment.

Income Taxes

During 2001, our effective tax rate was significantly impacted by goodwill amortization, the majority of

which was not deductible for tax purposes, and had the effect of increasing the overall tax rate. The reduction

in the effective tax rate for the year ended December 31, 2002 was primarily due to the elimination of

amortization of goodwill (as a result of adopting SFAS 142, effective January 1, 2002) the majority of which

was not deductible for tax purposes.

Impact of Contingent Convertible Debentures on Diluted Earnings per Common Share

On November 26, 2001, we completed our $250 million offering of 1

3

⁄

4

% contingent convertible debentures

due 2021, or the Debentures. Each one thousand dollar principal amount of Debentures is convertible into

11.429 shares of our common stock, which represents an initial conversion price of $87.50 per share. Holders

may surrender the Debentures for conversion into shares of our common stock under any of the following

circumstances: (i) if the sales price of our common stock is above 120% of the conversion price (or $105 per

share) for specified periods; (ii) if we call the Debentures; or (iii) if specified corporate transactions have

occurred. See Note 11 to the Consolidated Financial Statements for a further discussion of the Debentures.

The if-converted method is used in determining the dilutive effect of the Debentures in periods when the

holders of such securities are permitted to exercise their conversion rights. As of and for each of the years

ended December 31, 2003 and 2002, the holders of our Debentures did not have the ability to exercise their

conversion rights. Had the requirements to allow the holders to exercise their conversion rights been met and

the Debentures remained outstanding for the entire period, diluted earnings per common share would have been

reduced by approximately 2% during each of the years ended December 31, 2003 and 2002.

Quantitative and Qualitative Disclosures About Market Risk

We address our exposure to market risks, principally the market risk of changes in interest rates, through a

controlled program of risk management that may include the use of derivative financial instruments. We do not

hold or issue derivative financial instruments for trading purposes. We do not believe that our foreign exchange

exposure is material to our financial position or results of operations. See Note 2 to the Consolidated Financial

Statements for additional discussion of our financial instruments and hedging activities.

At December 31, 2003 and 2002, the fair value of our debt was estimated at $1.2 billion and $899

million, respectively, using quoted market prices and yields for the same or similar types of borrowings, taking

into account the underlying terms of the debt instruments. At December 31, 2003 and 2002, the estimated fair

value exceeded the carrying value of the debt by approximately $86 million and $77 million, respectively. An

46