Quest Diagnostics 2000 Annual Report Download - page 99

Download and view the complete annual report

Please find page 99 of the 2000 Quest Diagnostics annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108

|

|

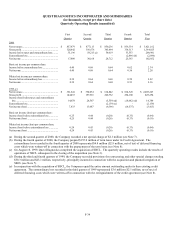

QUEST DIAGNOSTICS INCORPORATED AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

(dollars in thousands unless otherwise indicated)

F-29

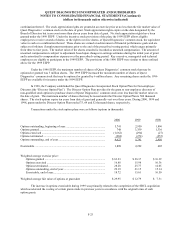

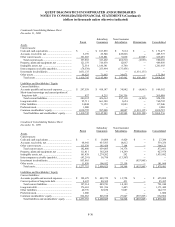

Investments in subsidiaries are accounted for by the parent on the equity method for purposes of the

supplemental consolidating presentation. Earnings (losses) of subsidiaries are therefore reflected in the parent’s

investment accounts and earnings. The principal elimination entries eliminate investments in subsidiaries and

intercompany balances and transactions.

The following condensed consolidating financial data illustrates the composition of the combined guarantors. It

reflects the impact of the Receivables Financing as discussed above beginning with the third quarter of 2000, the addition

of SBCL as a Subsidiary Guarantor for periods subsequent to the closing of the acquisition during the third quarter of

1999 (see Note 3) and the formation of two joint ventures in 1998 that are non-guarantor subsidiaries. The Company

believes that separate complete financial statements of the respective guarantors would not provide additional material

information which would be useful in assessing the financial composition of the Subsidiary Guarantors.