Priceline 2014 Annual Report Download - page 72

Download and view the complete annual report

Please find page 72 of the 2014 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

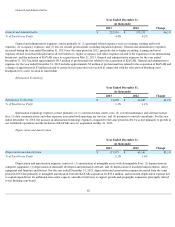

Off-Balance Sheet Arrangements.

As of December 31, 2014 , we did not have any off-balance sheet arrangements that have, or are reasonably likely to have, a current or

future effect on our financial condition, results of operations, liquidity, capital expenditures or capital resources.

Item 7A. Quantitative and Qualitative Disclosures About Market Risk

We manage our exposure to interest rate risk and foreign currency risk through internally established policies and procedures and, when

deemed appropriate, through the use of derivative financial instruments. We use foreign exchange derivative contracts to manage short-term

foreign currency risk.

The objective of our policies is to mitigate potential income statement, cash flow and fair value exposures resulting from possible future

adverse fluctuations in rates. We evaluate our exposure to market risk by assessing the anticipated near-term and long-term fluctuations in

interest rates and foreign exchange rates. This evaluation includes the review of leading market indicators, discussions with financial analysts

and investment bankers regarding current and future economic conditions and the review of market projections as to expected future rates. We

utilize this information to determine our own investment strategies as well as to determine if the use of derivative financial instruments is

appropriate to mitigate any potential future market exposure that we may face. Our policy does not allow speculation in derivative instruments

for profit or execution of derivative instrument contracts for which there are no underlying exposures. We do not use financial instruments for

trading purposes and are not a party to any leveraged derivatives. To the extent that changes in interest rates and currency exchange rates affect

general economic conditions, we would also be affected by such changes.

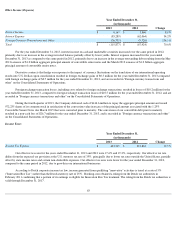

We did not experience any material changes in interest rate exposures during the year ended December 31, 2014

. Based upon economic

conditions and leading market indicators at December 31, 2014 , we do not foresee a significant adverse change in interest rates in the near

future.

Fixed rate investments are subject to unrealized gains and losses due to interest rate volatility. We performed a sensitivity analysis to

determine the impact a change in interest rates would have on the fair value of our available for sale investments assuming an adverse change of

100 basis points. A hypothetical 100 basis point (1.0%) increase in interest rates would have resulted in a decrease in the fair values of our

investments as of December 31, 2014 of approximately $85 million. These hypothetical losses would only be realized if we sold the investments

prior to their maturity.

As of December 31, 2014 , the outstanding aggregate principal amount of our debt is $4.2 billion . We estimate that the market value of

such debt was approximately $4.8 billion as of December 31, 2014 . A substantial portion of the market value of our debt in excess of the

outstanding principal amount is related to the conversion premium on our outstanding convertible bonds.

We conduct a significant portion of our business outside the United States through subsidiaries with functional currencies other than the

U.S. Dollar (primarily Euros). As a result, we face exposure to adverse movements in currency exchange rates as the operating results of our

international operations are translated from local currency into U.S. Dollars upon consolidation. If the U.S. Dollar weakens against the local

currency, the translation of these foreign-currency-denominated balances will result in increased net assets, gross bookings, gross profit,

operating expenses, and net income. Similarly, our net assets, gross bookings, gross profit, operating expenses, and net income will decrease if

the U.S. Dollar strengthens against the local currency. Additionally, foreign exchange rate fluctuations on transactions denominated in currencies

other than the functional currency results in gains and losses that are reflected in the Consolidated Statement of Operations.

From time to time, we enter into foreign exchange derivative contracts to minimize the impact of short-term foreign currency

fluctuations on our consolidated operating results. Our derivative contracts principally address foreign exchange fluctuation risk for the Euro and

the British Pound Sterling versus the U.S. Dollar. As of December 31, 2014 and 2013 , there were no such outstanding derivative contracts

associated with foreign currency translation risk. Foreign exchange gains of $13.7 million , $0.3 million , and $0.7 million for the years ended

December 31, 2014 , 2013 , and 2012 , respectively, were recorded in "Foreign currency transactions and other" in the Consolidated Statements

of Operations.

68