Priceline 2014 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2014 Priceline annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

|

|

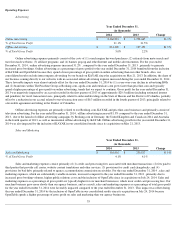

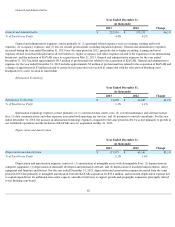

Foreign exchange transaction losses, including costs related to foreign exchange transactions, of $17.6 million for the year ended

December 31, 2014 , compared to foreign exchange transaction losses of $10.2 million for the year ended December 31, 2013 , are recorded in

"Foreign currency transactions and other" on the Consolidated Statements of Operations.

During the year ended December 31, 2014 , we delivered cash of $122.9 million to repay the aggregate principal amount and issued

300,256 shares of our common stock and paid cash of $2.2 million in satisfaction of the conversion value in excess of the principal amount

associated with our 1.25% Convertible Senior Notes due March 2015 that were converted prior to maturity. The conversion of our convertible

debt prior to maturity resulted in a non-cash loss of $6.3 million for the year ended December 31, 2014 , compared to a non-cash loss of $26.7

million for the year ended December 31, 2013 , which is recorded in "Foreign currency transactions and other" on the Consolidated Statements

of Operations.

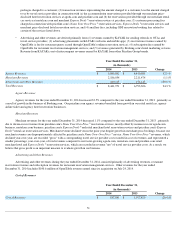

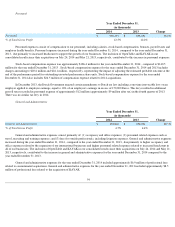

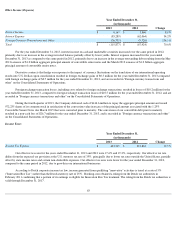

Income Taxes

Our effective tax rates, expressed as income tax expense as a percentage of earnings before income taxes, for the years ended

December 31, 2014 and 2013 were 19.0% and 17.6% , respectively. Our effective tax rate differs from the U.S. federal statutory tax rate of 35%,

due to lower tax rates outside the United States, partially offset by U.S. state income taxes and certain non-

deductible expenses. Our effective tax

rate was higher for the year ended December 31, 2014 , compared to the year ended December 31, 2013 , primarily due to the acquisitions of

OpenTable on July 24, 2014 and KAYAK on May 21, 2013, both of which are principally taxed at the higher U.S. tax rates.

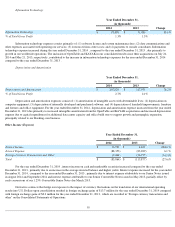

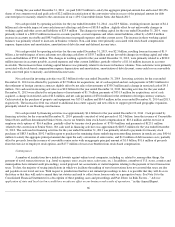

Under Dutch corporate income tax law, income generated from qualifying "innovative" activities is taxed at a rate of 5% ("Innovation

Box Tax") rather than the Dutch statutory rate of 25%. Booking.com obtained a ruling from the Dutch tax authorities confirming that a portion

of its earnings is eligible for Innovation Box Tax treatment. The ruling from the Dutch tax authorities is valid through December 31, 2017.

Until our U.S. net operating loss carryforwards are utilized or expire, most of our U.S. income will not be subject to a cash tax liability,

other than federal alternative minimum tax and state income taxes. However, we expect to pay foreign taxes on our non-U.S. income except in

countries where we have operating loss carryforwards. We expect that our international operations will grow their pretax income faster than the

U.S. business over the long term and, therefore, it is our expectation that our cash tax payments will increase as our international businesses

generate an increasing share of our pre-tax income.

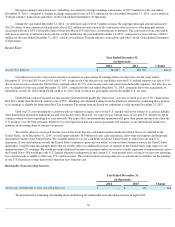

We will be subject to increased income taxes in the event that our cash balances held outside the United States are remitted to the

United States. As of December 31, 2014 , we held approximately $6.9 billion of cash, cash equivalents, short-term investments and long-term

investments outside of the United States. We currently intend to use our cash held outside the United States to reinvest in our non-U.S.

operations. If our cash balances outside the United States continue to grow and our ability to reinvest those balances outside the United States

diminishes, it will become increasingly likely that we will be subject to additional income tax expense in the United States with respect to our

unremitted non-

U.S. earnings. We would not make additional income tax payments unless we were to actually repatriate our international cash to

the United States. We would pay only U.S. federal alternative minimum tax and certain U.S. state income taxes as long as we have net operating

loss carryforwards available to offset our U.S. taxable income. This could result in us being subject to a cash income tax liability on the earnings

of our U.S. businesses sooner than would otherwise have been the case.

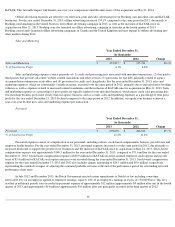

Redeemable Noncontrolling Interests

We purchased the remaining outstanding shares underlying the redeemable noncontrolling interests in April 2013.

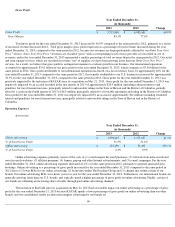

56

Year Ended December 31,

(in thousands)

2014

2013

Change

Income Tax Expense

$

567,695

$

403,739

40.6

%

Year Ended December 31,

(in thousands)

2014

2013

Change

Net Income Attributable to Noncontrolling Interests

$

—

$

135

NA