Pottery Barn 2008 Annual Report Download - page 67

Download and view the complete annual report

Please find page 67 of the 2008 Pottery Barn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

|

|

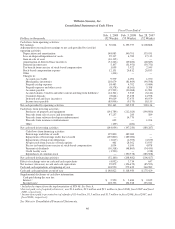

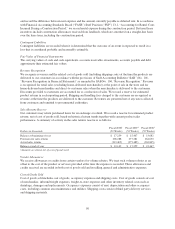

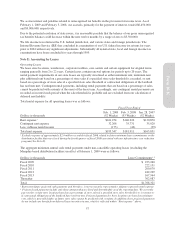

of credit represent only a future commitment to fund inventory purchases to which we had not taken legal title as

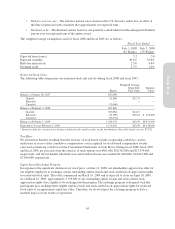

of February 1, 2009. The latest expiration possible for any future letters of credit issued under the facilities is

February 1, 2010.

Interest Expense

Interest expense was $1,480,000 (net of capitalized interest of $1,163,000), $2,099,000 (net of capitalized interest

of $1,389,000) and $2,125,000 (net of capitalized interest of $699,000) for fiscal 2008, fiscal 2007 and fiscal

2006, respectively.

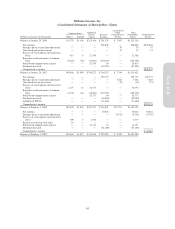

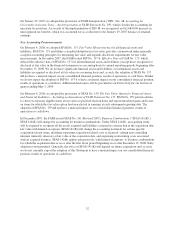

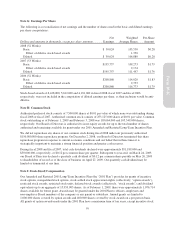

Note D: Income Taxes

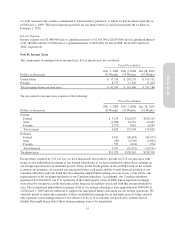

The components of earnings before income taxes, by tax jurisdiction, are as follows:

Fiscal Year Ended

Dollars in thousands

Feb. 1, 2009

(52 Weeks)

Feb. 3, 2008

(53 Weeks)

Jan. 28, 2007

(52 Weeks)

United States $ 33,376 $ 299,235 $ 319,732

Foreign 8,577 17,105 17,454

Total earnings before income taxes $ 41,953 $ 316,340 $ 337,186

The provision for income taxes consists of the following:

Fiscal Year Ended

Dollars in thousands

Feb. 1, 2009

(52 Weeks)

Feb. 3, 2008

(53 Weeks)

Jan. 28, 2007

(52 Weeks)

Current

Federal $ 5,143 $126,219 $148,125

State (1,096) 19,254 24,645

Foreign 2,775 7,061 6,299

Total current 6,822 152,534 179,069

Deferred

Federal 4,817 (26,494) (44,573)

State (83) (4,796) (5,802)

Foreign 373 (661) (376)

Total deferred 5,107 (31,951) (50,751)

Total provision $11,929 $120,583 $128,318

Except where required by U.S. tax law, we have historically elected not to provide for U.S. income taxes with

respect to the undistributed earnings of our foreign subsidiaries as we have intended to utilize those earnings in

our foreign operations for an indefinite period of time. In the fourth quarter of fiscal 2008, based on the current

economic environment, we assessed our anticipated future cash needs and the overall financial position of our

Canadian subsidiary and concluded that the remaining undistributed earnings were in excess of our future cash

requirements for the on-going operations of our Canadian subsidiary. Accordingly, our Canadian subsidiary

repatriated $13,900,000 to our U.S. operations in the fourth quarter of fiscal 2008. These repatriated earnings

were offset by foreign tax credits that reduced the financial tax liability associated with this foreign dividend to

zero. The accumulated undistributed earnings of all of our foreign subsidiaries were approximately $500,000 as

of February 1, 2009 and are sufficient to support our anticipated future cash needs for our foreign operations. We

currently intend to utilize the remainder of these undistributed earnings for an indefinite period of time and will

only repatriate such earnings when it is tax effective to do so. It is currently not practical to estimate the tax

liability that might be payable if these foreign earnings were to be repatriated.

55

Form 10-K