Pep Boys 2012 Annual Report Download - page 81

Download and view the complete annual report

Please find page 81 of the 2012 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended February 2, 2013, January 28, 2012 and January 29, 2011

NOTE 1—SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES (Continued)

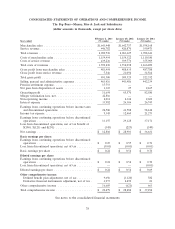

MERCHANDISE INVENTORIES Merchandise inventories are valued at the lower of cost or

market. Cost is determined by using the last-in, first-out (LIFO) method. If the first-in, first-out (FIFO)

method of costing inventory had been used by the Company, inventory would have been $565.8 million

and $536.4 million as of February 2, 2013 and January 28, 2012, respectively. During fiscal 2012, 2011

and 2010, the effect of LIFO layer liquidations on gross profit was immaterial.

The Company’s inventory, consisting primarily of automotive tires, parts, and accessories, is used

on vehicles typically having long lives. Because of this, and combined with the Company’s historical

experience of returning excess inventory to the Company’s vendors for full credit, the risk of

obsolescence is minimal. The Company establishes a reserve for excess inventory for instances where

less than full credit will be received for such returns or where the Company anticipates items will be

sold at retail prices that are less than recorded costs. The reserve is based on management’s judgment,

including estimates and assumptions regarding marketability of products, the market value of inventory

to be sold in future periods and on historical experiences where the Company received less than full

credit from vendors for product returns. The Company also provides for estimated inventory shrinkage

based upon historical levels and the results of its cycle counting program. The Company’s inventory

adjustments for these matters were approximately $4.6 million at February 2, 2013 and January 28,

2012, respectively. In future periods the company may be exposed to material losses should the

company’s vendors alter their policy with regard to accepting excess inventory returns.

PROPERTY AND EQUIPMENT Property and equipment are recorded at cost. Depreciation and

amortization are computed using the straight-line method over the following estimated useful lives:

building and improvements, 5 to 40 years, and furniture, fixtures and equipment, 3 to 10 years.

Maintenance and repairs are charged to expense as incurred. Upon retirement or sale, the cost and

accumulated depreciation are eliminated and the gain or loss, if any, is included in the determination

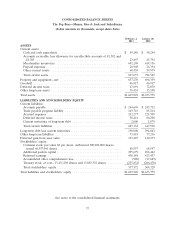

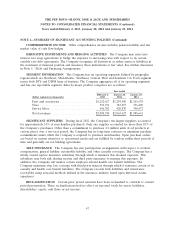

of net income. Property and equipment information follows:

February 2, January 28,

(dollar amounts in thousands) 2013 2012

Land ...................................... $ 203,386 $ 204,023

Buildings and improvements ...................... 885,389 875,999

Furniture, fixtures and equipment .................. 728,122 723,938

Construction in progress ........................ 3,282 3,279

Accumulated depreciation and amortization .......... (1,162,909) (1,110,900)

Property and equipment—net ..................... $ 657,270 $ 696,339

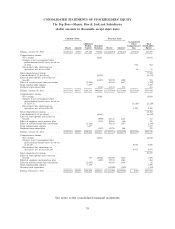

GOODWILL At fiscal year end 2012, the Company had six reporting units, of which three

included goodwill (related to prior acquisitions by the Company). The Company tests the recorded

amount of goodwill for recovery on an annual basis in the fourth quarter of each fiscal year.

Impairment reviews may also be triggered by any significant events or changes in circumstances

affecting the Company’s business.

Goodwill impairment testing consists of a two-step process, if necessary. The first step is to

compare the fair value of a reporting unit with its carrying amount. If the carrying amount of a

reporting unit exceeds its fair value, the second step of the impairment test must be performed in order

42