Pep Boys 2012 Annual Report Download - page 110

Download and view the complete annual report

Please find page 110 of the 2012 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended February 2, 2013, January 28, 2012 and January 29, 2011

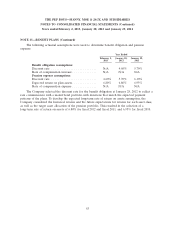

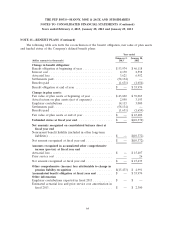

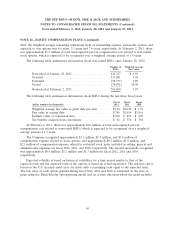

NOTE 14—EQUITY COMPENSATION PLANS (Continued)

During fiscal 2011, the Company began an employee stock purchase plan which provides eligible

employees the opportunity to purchase shares of the Company’s stock at a stated discount through

regular payroll deductions. The aggregate number of shares of common stock that may be issued or

transferred under the plan is 2,000,000 shares. All shares purchased by employees under this plan will

be issued through treasury stock. The Company’s expense for the discount during fiscal years 2012 and

2011 was immaterial. As of February 2, 2013, there were 1,916,178 shares available for issuing under

this plan.

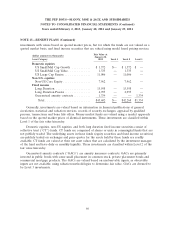

NOTE 15—INTEREST RATE SWAP AGREEMENT

On October 11, 2012, the Company settled its interest rate swap designated as a cash flow hedge

on $145.0 million of the Company’s Term Loan prior to its amendment and restatement. The swap was

used to minimize interest rate exposure and overall interest costs by converting the variable component

of the total interest rate to a fixed rate of 5.036%. Since February 1, 2008, this swap was deemed to be

fully effective and all adjustments in the interest rate swap’s fair value were recorded to accumulated

other comprehensive loss. The settlement of this swap resulted in an interest charge of $7.5 million,

which was previously recorded within accumulated other comprehensive loss. As of January 28, 2012,

the fair value of this swap was a net $12.5 million payable, recorded within other long-term liabilities

on the balance sheet.

On October 11, 2012, the Company entered into two new interest rate swaps for a notional

amount of $50.0 million each that together are designated as a cash flow hedge on the first

$100.0 million of the amended and restated Term Loan. The interest rate swaps convert the variable

LIBOR portion of the interest payments due on the first $100.0 million of the Term Loan to a fixed

rate of 1.855%. As of February 2, 2013, the fair value of the new swap was a net $1.6 million payable,

recorded within other long-term liabilities on the balance sheet.

NOTE 16—FAIR VALUE MEASUREMENTS

The Company’s fair value measurements consist of (a) non-financial assets and liabilities that are

recognized or disclosed at fair value in the Company’s financial statements on a recurring basis (at least

annually) and (b) all financial assets and liabilities.

Fair value is defined as the exit price, or the amount that would be received to sell an asset or

paid to transfer a liability in an orderly transaction between market participants as of the measurement

date. There is a hierarchy for inputs used in measuring fair value that maximizes the use of observable

inputs and minimizes the use of unobservable inputs by requiring that the most observable inputs be

used when available. Observable inputs are inputs market participants would use in valuing the asset or

liability developed based on market data obtained from sources independent of the Company.

Unobservable inputs are inputs that reflect the Company’s assumptions about the factors market

participants would use in valuing the asset or liability developed based upon the best information

available in the circumstances. The hierarchy is broken down into three levels. Level 1 inputs are

quoted prices (unadjusted) in active markets for identical assets or liabilities. Level 2 inputs include

quoted prices for similar assets or liabilities in active markets. Level 3 inputs are unobservable inputs

for the asset or liability. Categorization within the valuation hierarchy is based upon the lowest level of

input that is significant to the fair value measurement.

71