Pep Boys 2012 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2012 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

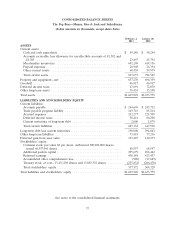

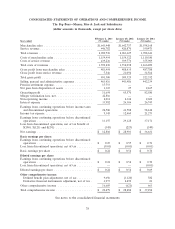

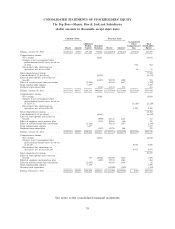

ITEM 7A QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

We have market rate exposure in our financial instruments due to changes in interest rates and

prices.

Variable and Fixed Rate Debt

Our Revolving Credit Agreement bears interest at daily LIBOR plus 2.00% to 2.50% based upon

the then current availability under the facility. At February 2, 2013, there were no outstanding

borrowings under the agreement. Additionally, we have a Senior Secured Term Loan facility due

October 2018 with a balance of $200 million at February 2, 2013, that bears interest at LIBOR subject

to a floor of 1.25%, plus 3.75%. Excluding our interest rate swap, a one percent change in the LIBOR

rate would have affected net earnings by approximately $1.2 million for fiscal 2012. The risks related to

changes in the LIBOR rate are substantially mitigated by our interest rate swap.

The fair value of our Senior Subordinated Notes due October 2018 was $203.5 million at

February 2, 2013. We determine fair value on our fixed rate debt by using quoted market prices and

current interest rates.

Interest Rate Swaps

On October 11, 2012, we settled our interest rate swap designated as a cash flow hedge on

$145.0 million of our Term Loan prior to its amendment and restatement. The swap was used to

minimize interest rate exposure and overall interest costs by converting the variable component of the

total interest rate to a fixed rate of 5.036%. Since February 1, 2008, this swap was deemed to be fully

effective and all adjustments in the interest rate swap’s fair value have been recorded to accumulated

other comprehensive loss. The settlement of this swap resulted in an interest charge of $7.5 million,

which was previously recorded within accumulated other comprehensive loss.

On October 11, 2012, we entered into two new interest rate swaps for a notional amount of

$50.0 million each that together are designated as a cash flow hedge on the first $100.0 million of the

amended and restated Term Loan. The interest rate swaps convert the variable LIBOR portion of the

interest payments, subject to a floor of 1.25%, due on the first $100.0 million of the Term Loan to a

fixed rate of 1.855%.

As of February 2, 2013, the fair value of the new interest rate swaps was a net $1.6 million

payable. As of January 28, 2012, the fair value of the previous swap, terminated in October 2012, was

$12.5 million payable. The swap value is recorded within other long-term liabilities on the balance

sheet.

35