Pep Boys 2012 Annual Report Download - page 102

Download and view the complete annual report

Please find page 102 of the 2012 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

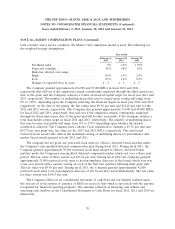

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended February 2, 2013, January 28, 2012 and January 29, 2011

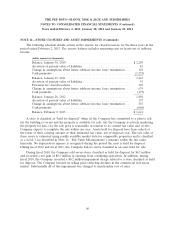

NOTE 13—BENEFIT PLANS (Continued)

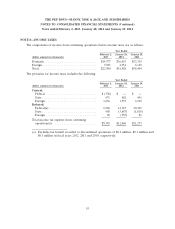

The following actuarial assumptions were used to determine benefit obligation and pension

expense:

Year Ended

February 2, January 28, January 29,

2013 2012 2011

Benefit obligation assumptions:

Discount rate .......................... N/A 4.60% 5.70%

Rate of compensation increase .............. N/A N/A N/A

Pension expense assumptions:

Discount rate .......................... 4.60% 5.70% 6.10%

Expected return on plan assets .............. 6.80% 6.80% 6.95%

Rate of compensation expense .............. N/A N/A N/A

The Company selected the discount rate for the benefit obligation at January 28, 2012 to reflect a

rate commensurate with a model bond portfolio with durations that match the expected payment

patterns of the plans. To develop the expected long-term rate of return on assets assumption, the

Company considered the historical returns and the future expectations for returns for each asset class,

as well as the target asset allocation of the pension portfolio. This resulted in the selection of a

long-term rate of return on assets of 6.80% for fiscal 2012 and fiscal 2011, and 6.95% for fiscal 2010.

63