Pep Boys 2012 Annual Report Download - page 101

Download and view the complete annual report

Please find page 101 of the 2012 Pep Boys annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

|

|

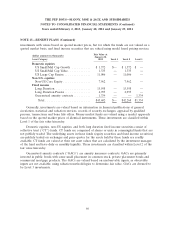

THE PEP BOYS—MANNY, MOE & JACK AND SUBSIDIARIES

NOTES TO CONSOLIDATED FINANCIAL STATEMENTS (Continued)

Years ended February 2, 2013, January 28, 2012 and January 29, 2011

NOTE 13—BENEFIT PLANS (Continued)

The Company has a qualified 401(k) savings plan and a separate savings plan for employees

residing in Puerto Rico, which cover all full-time employees who are at least 21 years of age with one

or more years of service. The Company contributes the lesser of 50% of the first 6% of a participant’s

contributions or 3% of the participant’s compensation under both savings plans. For fiscal 2012, 2011

and 2010, the Company’s contributions were conditional upon the achievement of certain

pre-established financial performance goals which were met in fiscal 2010, but not in fiscal 2012 or

2011. The Company’s savings plans’ contribution expense was $3.0 million in fiscal 2010.

The Company also maintained a defined benefit pension plan (the ‘‘Plan’’) covering full-time

employees hired on or before February 1, 1992. As of December 31, 1996, the Company froze the

accrued benefits under the Plan and active participants became fully vested. During the third quarter of

fiscal 2011, the Company began the process of terminating the Plan. During the fourth quarter of fiscal

2012, in accordance with Internal Revenue Service and Pension Benefit Guaranty Corporation

requirements, the Company contributed $14.1 million to fully fund the Plan on a termination basis and

recorded a $17.8 million settlement charge. The participants’ benefits were converted into a lump sum

cash payment or an annuity contract placed with an insurance carrier. The Company used a fiscal year

end measurement date for determining the benefit obligation and the fair value of Plan assets. The

actuarial computations were made using the ‘‘projected unit credit method.’’ Variances between actual

experience and assumptions for costs and returns on assets were amortized over the remaining service

lives of employees under the Plan.

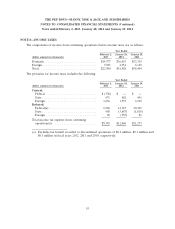

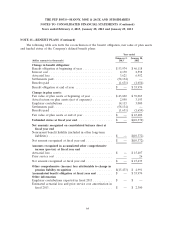

Pension expense is as follows:

Year Ended

February 2, January 28, January 29,

(dollar amounts in thousands) 2013 2012 2011

Service cost ............................ $ — $ — $ —

Interest cost ........................... 2,170 2,558 2,561

Expected return on plan assets .............. (2,658) (2,745) (2,151)

Amortization of prior service cost ............ 13 14 14

Recognized actuarial loss .................. 1,896 1,499 1,672

Net Period Pension Cost .................. 1,421 1,326 2,096

Settlement Charge ....................... 17,753 — —

Net Period Pension Cost .................. $19,174 $ 1,326 $ 2,096

62