NetSpend 2012 Annual Report Download - page 36

Download and view the complete annual report

Please find page 36 of the 2012 NetSpend annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

26 -

27

27 -

28

28 -

29

29 -

30

30 -

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

|

|

billing adjustments are recorded as a reduction of

revenues in the Company’s Consolidated Statements

of Income and actual adjustments to invoices are

charged against the allowance for billing

adjustments.

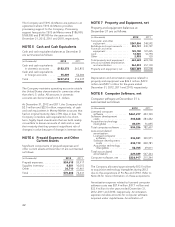

PROPERTY AND EQUIPMENT: Property and

equipment are stated at cost less accumulated

depreciation and amortization. Depreciation and

amortization are computed using the straight-line

method over the estimated useful lives of the assets.

Buildings and improvements are depreciated over

estimated useful lives of 5-40 years, computer and

other equipment over estimated useful lives of 2-

5 years, and furniture and other equipment over

estimated useful lives of 3-15 years. The Company

evaluates impairment losses on long-lived assets

used in operations in accordance with the provisions

of ASC 360, “Property Plant and Equipment.”

All ordinary repairs and maintenance costs are

expensed as incurred. Maintenance costs that extend

the asset life are capitalized and amortized over the

remaining estimated life of the asset.

LICENSED COMPUTER SOFTWARE: The

Company licenses software that is used in providing

services to clients. Licensed software is obtained

through perpetual licenses and site licenses and

through agreements based on processing capacity

(called “MIPS agreements”). Perpetual and site

licenses are amortized using the straight-line method

over their estimated useful lives which range from

three to ten years. Software licensed under MIPS

agreements is amortized using a units-of-production

basis over the estimated useful life of the software,

generally not to exceed ten years. At each balance

sheet date, the Company evaluates impairment

losses on long-lived assets used in operations in

accordance with ASC 360.

ACQUISITION TECHNOLOGY

INTANGIBLES: These identifiable intangible assets

are software technology assets resulting from

acquisitions. These assets are amortized using the

straight-line method over periods not exceeding their

estimated useful lives, which range from five to nine

years. The provisions of ASC 350, “Intangibles —

Goodwill and Other,” require that intangible assets

with estimated useful lives be amortized over their

respective estimated useful lives to their residual

values, and reviewed for impairment in accordance

with ASC 360. Acquisition technology intangibles net

book values are included in computer software, net in

the accompanying balance sheets. Amortization

expenses are charged to cost of services in the

Company’s Consolidated Statements of Income.

SOFTWARE DEVELOPMENT COSTS: In

accordance with the provisions of ASC 985,

“Software,” software development costs are

capitalized once technological feasibility of the

software product has been established. Costs

incurred prior to establishing technological feasibility

are expensed as incurred. Technological feasibility is

established when the Company has completed a

detailed program design and has determined that a

product can be produced to meet its design

specifications, including functions, features and

technical performance requirements. Capitalization of

costs ceases when the product is generally available

to clients. At each balance sheet date, the Company

evaluates the unamortized capitalized costs of

software development as compared to the net

realizable value of the software product which is

determined by future undiscounted net cash flows.

The amount by which the unamortized software

development costs exceed the net realizable value is

written off in the period that such determination is

made. Software development costs are amortized

using the greater of (1) the straight-line method over

its estimated useful life, which ranges from three to

ten years or (2) the ratio of current revenues to total

anticipated revenue over its useful life.

The Company also develops software that is used

internally. These software development costs are

capitalized based upon the provisions of ASC 350.

Internal-use software development costs are

capitalized once: (1) the preliminary project stage is

completed, (2) management authorizes and commits

to funding a computer software project, and (3) it is

probable that the project will be completed and the

software will be used to perform the function

intended. Costs incurred prior to meeting the

qualifications are expensed as incurred. Capitalization

of costs ceases when the project is substantially

complete and ready for its intended use. Internal-use

software development costs are amortized using an

estimated useful life of three to five years. Software

development costs may become impaired in

situations where development efforts are abandoned

due to the viability of the planned project becoming

doubtful or due to technological obsolescence of the

planned software product.

CONTRACT ACQUISITION COSTS: The Company

capitalizes contract acquisition costs related to

signing or renewing long-term contracts. The

Company capitalizes internal conversion costs in

accordance with the provisions of Staff Accounting

33