Lexmark 2014 Annual Report Download - page 78

Download and view the complete annual report

Please find page 78 of the 2014 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

ASU 2014-09 will be effective for the Company on January 1, 2017 and may be adopted through either retrospective application to all

periods presented in the financial statements or through a cumulative effect adjustment to retained earnings by applying the new

guidance to contracts that still require performance at the effective date. Early adoption is not permitted. The Company is in the

process of evaluating a sample of its contracts with customers under the new standard and cannot currently estimate the financial

statement impact of adoption. The Company has not made a decision regarding the transition method it will use to adopt the new

standard.

In August 2014, the FASB issued Accounting Standards Update No. 2014-15, Presentation of Financial Statements – Going Concern

(Subtopic 205-40): Disclosure of Uncertainties about an Entity’s Ability to Continue as a Going Concern (“ASU 2014-15”). Under

ASU 2014-15, management must evaluate on a quarterly basis whether there are conditions or events that raise substantial doubt about

the entity’s ability to continue as a going concern. Substantial doubt exists when it is probable that the entity will be unable to meet its

obligations as they become due within one year after the date that the financial statements are issued. Disclosures will be required if

conditions or events give rise to substantial doubt. The amendments in ASU 2014-15 will be effective starting with the Company’s

2016 annual financial statements and are not expected to have a material impact.

The FASB and SEC staff issued other accounting guidance during the period that is not applicable to the Company’s consolidated

financial statements and disclosures and, therefore, is not discussed above.

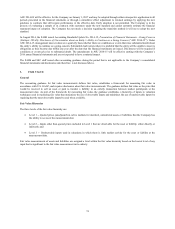

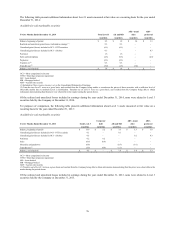

3. FAIR VALUE

General

The accounting guidance for fair value measurements defines fair value, establishes a framework for measuring fair value in

accordance with U.S. GAAP, and requires disclosures about fair value measurements. The guidance defines fair value as the price that

would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the

measurement date. As part of the framework for measuring fair value, the guidance establishes a hierarchy of inputs to valuation

techniques used in measuring fair value that maximizes the use of observable inputs and minimizes the use of unobservable inputs by

requiring that the most observable inputs be used when available.

Fair Value Hierarchy

The three levels of the fair value hierarchy are:

Level 1 -- Quoted prices (unadjusted) in active markets for identical, unrestricted assets or liabilities that the Company has

the ability to access at the measurement date;

Level 2 -- Inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or

indirectly; and

Level 3 -- Unobservable inputs used in valuations in which there is little market activity for the asset or liability at the

measurement date.

Fair value measurements of assets and liabilities are assigned a level within the fair value hierarchy based on the lowest level of any

input that is significant to the fair value measurement in its entirety.

74