Lexmark 2014 Annual Report Download - page 41

Download and view the complete annual report

Please find page 41 of the 2014 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

31 -

32

32 -

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

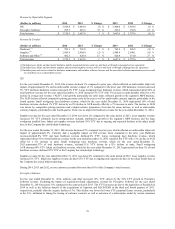

other factors which is recognized in other comprehensive income. Refer to Part II, Item 8, Note 2 of the Notes to Consolidated

Financial Statements for more details regarding this guidance. The Company’s policy considers various factors in making these two

assessments.

Given the level of judgment required to make the assessments, the final outcomes of the Company’s investments in debt securities

could prove to be different than the results reported. Issuers with good credit standings and relatively solid financial conditions today

may not be able to fulfill their obligations ultimately. Furthermore, the Company could reconsider its decision not to sell a security

depending on changes in its own cash flow projections as well as changes in the regulatory and economic environment that may

indicate that selling a security is advantageous to the Company. Historically, the Company has incurred a low amount of realized

losses from sales of marketable securities.

Refer to Part II, Item 8, Note 7 of the Notes to Consolidated Financial Statements for more information regarding the Company’s

marketable securities.

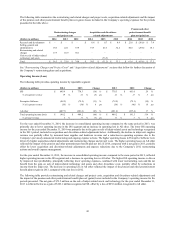

Business Combinations

The application of the acquisition method of accounting for business combinations requires the use of significant estimates and

assumptions in the determination of the fair value of assets acquired and liabilities assumed in order to properly allocate purchase

price consideration between identifiable intangible assets and goodwill. The fair values of identifiable intangible assets are estimated

using an income approach, including the excess earnings, relief from royalty and with-and-without methods. These estimations are

conducted using market participant assumptions and require projected financial information, including assumptions about future

revenue growth and costs necessary to facilitate the projected growth. Other key inputs include assumptions about technological

obsolescence, customer attrition rates, brand recognition and discount rates. The Company also considers market participant

assumptions in its valuations of deferred revenue acquired in a business combination, including estimated costs to fulfill the obligation

as well as a profit markup that would exist in the case of a hypothetical third-party servicing firm.

Goodwill and Intangible Assets

Lexmark performs an assessment of its goodwill for impairment each fiscal year as of December 31 or between annual tests if an

event occurs or circumstances change that lead management to believe it is more likely than not that an impairment exists. Examples

of such events or circumstances include a deterioration in general economic conditions, increased competitive environment, or a

decline in overall financial performance of the Company. Goodwill is tested at the reporting unit level, which is an operating segment

or one level below an operating segment (a "component") if the component constitutes a business for which discrete financial

information is available and regularly reviewed by segment management. Components are aggregated as a single reporting unit if they

have similar economic characteristics. Goodwill is assigned to reporting units of the Company that are expected to benefit from the

synergies of the related acquisition.

Although the qualitative assessment for goodwill impairment testing is available to Lexmark, the Company performed a quantitative

test of impairment in 2014 and 2013. In estimating the fair value of its reporting units, the Company generally considers a discounted

cash flow analysis, which requires judgments such as projected future earnings and weighted average cost of capital, and market based

measurements analysis, which include multiples developed from prices paid in observed market transactions of comparable

companies. For its estimation of the fair value of the Perceptive Software reporting unit, the Company used an equally-weighted

measure based on a discounted cash flow analysis and a market based measurement analysis. For its estimation of the fair value of the

ISS reporting unit, the Company used a discounted cash flow analysis.

Goodwill recognized by the Company at December 31, 2014 was $605.8 million and was allocated to the Perceptive Software and ISS

reporting units in the amount of $587.0 million and $18.8 million, respectively. The fair values of these reporting units were

substantially in excess of their carrying values on this date. The values of Perceptive Software and ISS were heavily reliant on

forecasted financial information. Key assumptions to the valuation of Perceptive Software include its ability to strengthen its channel

presence and expand internationally and the revenue growth that would result therefrom. Other key inputs to the fair value

calculations include operating margin assumptions and discount rates.

Intangible assets with finite lives are amortized over their estimated useful lives using the straight-line method. In certain instances

where consumption could be greater in the earlier years of the asset’s life, the Company has selected, as a compensating measure, a

shorter period over which to amortize the asset. The Company’s intangible assets with finite lives are tested for impairment in

accordance with its policy for long-lived assets below.

Long-Lived Assets Held and Used

Lexmark reviews for impairment of long-lived assets whenever events or changes in circumstances indicate that the carrying amount

of an asset (or asset group) may not be recoverable. If the estimated undiscounted future cash flows expected to result from the use of

the assets and their eventual disposition are insufficient to recover the carrying value of the assets, then an impairment loss is

37