Lexmark 2014 Annual Report Download - page 119

Download and view the complete annual report

Please find page 119 of the 2014 Lexmark annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

118 -

119

119 -

120

120 -

121

121 -

122

122 -

123

123 -

124

124 -

125

125 -

126

126 -

127

127 -

128

128 -

129

129 -

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

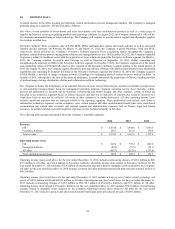

Cash Flow Hedges

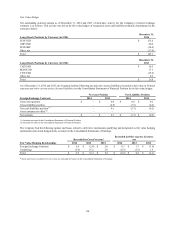

The Company’s cash flow hedging contracts are not subject to master netting agreements or other terms under U.S. GAAP that allow

net presentation in the Consolidated Statements of Financial Position. The total notional amounts as of December 31, 2014 of the

Company’s foreign exchange options designated as cash flow hedges of anticipated Euro and British pound denominated sales were

$683.3 million and $56.0 million, respectively. As of December 31, 2014, the Company had the following gross derivative assets

(liabilities) recorded at fair value in Prepaid expenses and other current assets (Accrued liabilities) on the Consolidated Statements of

Financial Position for its cash flow hedges:

Foreign Exchange Contracts 2014

Gross asset position $ 28.3

Gross (liability) position (8.6)

The Company had the following gains and (losses) related to derivative instruments qualifying and designated as cash flow hedging

instruments and related hedged items recorded on the Consolidated Statements of Comprehensive Earnings:

Location of gain Pre-tax amount of

Amount of after-tax (loss) reclassified gain (loss)

gain (loss) recognized from Accumulated reclassified from

in Other other comprehensive Accumulated other

Comprehensive loss into Net comprehensive loss

(loss) earnings earnings into Net earnings

Cash Flow Hedging (effective portion) (effective portion) (effective portion)

Relationships 2014

2014

Foreign Exchange

Contracts $ 15.9 Revenue $ –

During the fourth quarter of 2014, Lexmark entered into foreign exchange option contracts as hedges of anticipated foreign currency

denominated sales. The settlement of these contracts and subsequent recognition in the Company’s Consolidated Statements of

Earnings will begin in the first quarter of 2015 and continue throughout the year as the underlying hedged transactions occur. As of

December 31, 2014, deferred net gains on derivative instruments recorded in Accumulated other comprehensive loss were

$17.6 million pre-tax, all of which, if realized, will be reclassified into earnings during the next 12 months. No gains or losses were

reclassified into earnings for cash flow hedges for the years ended December 31, 2014, 2013 or 2012. Ineffective portions of hedges

are immediately recognized in current period earnings. There were no material gains or losses related to the ineffective portion of

hedges recognized in 2014, 2013 or 2012.

Additional information regarding derivatives can be referenced in Note 3 of the Notes to Consolidated Financial Statements.

Concentrations of Risk

Lexmark’s main concentrations of credit risk consist primarily of cash equivalent investments, marketable securities and trade

receivables. Cash equivalents and marketable securities investments are made in a variety of high quality securities with prudent

diversification requirements. The Company seeks diversification among its cash investments by limiting the amount of cash

investments that can be made with any one obligor. Credit risk related to trade receivables is dispersed across a large number of

customers located in various geographic areas. Collateral such as letters of credit and bank guarantees is required in certain

circumstances. In addition, the Company uses credit insurance for specific obligors to limit the impact of nonperformance. Lexmark

sells a large portion of its products through third-party distributors and resellers and original equipment manufacturer (“OEM”)

customers. If the financial condition or operations of these distributors, resellers and OEM customers were to deteriorate substantially,

the Company’s operating results could be adversely affected. The three largest distributor, reseller and OEM customers collectively

represented $108 million or approximately 19% of the dollar amount of outstanding invoices at December 31, 2014 and $107 million

or approximately 18% of the dollar amount of outstanding invoices at December 31, 2013. One OEM customer accounted for

$42 million or approximately 7% of the dollar amount of outstanding invoices at December 31, 2014 and $48 million or

approximately 8% of the dollar amount of outstanding invoices at December 31, 2013. Lexmark performs ongoing credit evaluations

of the financial position of its third-party distributors, resellers and other customers to determine appropriate credit limits.

Lexmark generally has experienced longer accounts receivable cycles in its emerging markets, in particular, Latin America, when

compared to its U.S. and European markets. In the event that accounts receivable cycles in these developing markets lengthen further,

the Company could be adversely affected.

115