Kia 2006 Annual Report Download - page 52

Download and view the complete annual report

Please find page 52 of the 2006 Kia annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

|

|

052

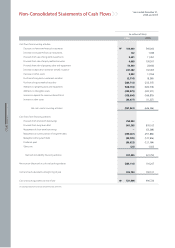

KIA MOTORS 2006 Annual Report

The Board of Directors and Stockholders

Kia Motors Corporation:

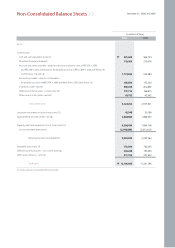

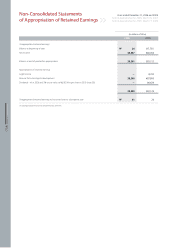

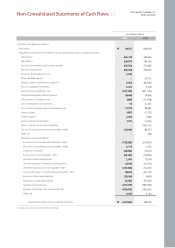

We have audited the accompanying non-consolidated balance sheet of Kia Motors Corporation (the “Company”) as of December 31, 2006, and the related non-

consolidated statements of income, appropriation of retained earnings and cash flows for the year then ended. These non-consolidated financial statements are

the responsibility of the Company’s management. Our responsibility is to express an opinion on these non-consolidated financial statements based on our audit.

The accompanying non-consolidated financial statements of the Company as of December 31, 2005, were audited by other auditors, whose report thereon dated

January 26, 2006, expressed an unqualified opinion on those statements.

We conducted our audit in accordance with auditing standards generally accepted in the Republic of Korea. Those standards require that we plan and perform the

audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis,

evidence supporting the amounts and disclosures in the financial statements. An audit also includes assessing the accounting principles used and significant

estimates made by management, as well as evaluating the overall financial statement presentation. We believe that our audit provides a reasonable basis for our

opinion.

In our opinion, the non-consolidated financial statements referred to above present fairly, in all material respects, the financial position of Kia Motors Corporation as

of December 31, 2006, and the results of its operations, the appropriation of its retained earnings, and its cash flows for the year then ended in conformity with

accounting principles generally accepted in the Republic of Korea.

Without qualifying our opinion, we draw attention to the following:

As discussed in note 1(b) to the non-consolidated financial statements, accounting principles and auditing standards and their application in practice vary among

countries. The accompanying non-consolidated financial statements are not intended to present the financial position, results of operations and cash flows in

accordance with accounting principles and practices generally accepted in countries other than the Republic of Korea. In addition, the procedures and practices

utilized in the Republic of Korea to audit such financial statements may differ from those generally accepted and applied in other countries. Accordingly, this report

and the accompanying non-consolidated financial statements are for use by those knowledgeable in Korean accounting principles and auditing standards and

their application in practice.

KPMG Samjong Accounting Corp.

Seoul, Korea

January 31, 2007

Independent Auditors’ Report

Based on a report originally issued in Korean

∷This report is effective as of January 31, 2007, the audit report date. Certain subsequent events or circumstances, which may occur between the audit

report date and the time of reading this report, could have a material impact on the accompanying non-consolidated financial statements and notes

thereto. Accordingly, the readers of the audit report should understand that there is a possibility that the above audit report may have to be revised to

reflect the impact of such subsequent events or circumstances, if any.