IBM 2001 Annual Report Download - page 77

Download and view the complete annual report

Please find page 77 of the 2001 IBM annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

|

|

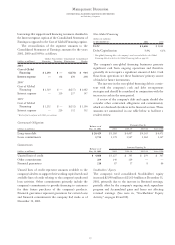

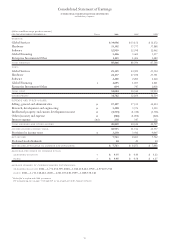

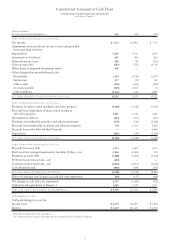

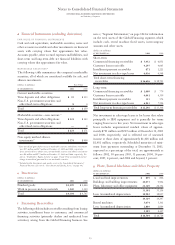

Notes to Consolidated Financial Statements

INTERNATIONAL BUSINESS MACHINES CORPORATION

and Subsidiary Companies

75

aSignificant Accounting Policies

PRINCIPLES OF CONSOLIDATION

The consolidated financial statements include the accounts

of International Business Machines Corporation and its con-

trolled subsidiary companies, which in general are majority

owned. Investments in business entities in which the com-

pany does not have control, but has the ability to exercise

significant influence over operating and financial policies

(generally 20-50 percent ownership), are accounted for by

the equity method. Other investments are accounted for

by the cost method. The accounting policy for other invest-

ments in securities is described on page 78 within

“Marketable Securities.”

USE OF ESTIMATES

The preparation of financial statements in conformity with

generally accepted accounting principles requires manage-

ment to make estimates and assumptions that affect the

amounts that are reported in the consolidated financial state-

ments and accompanying disclosures. Although these

estimates are based on management’s best knowledge of cur-

rent events and actions that the company may undertake in

the future, actual results may be different from the estimates.

REVENUE

The company recognizes revenue when it is realized or real-

izable and earned. The company considers revenue realized

or realizable and earned when it has persuasive evidence of

an arrangement, the product has been shipped or the services

have been provided to the customer, the sales price is fixed

or determinable and collectibility is reasonably assured. The

company reduces revenue for estimated customer returns

and other allowances. In addition to the aforementioned

general policy, the following are the specific revenue recog-

nition policies for each major category of revenue and for

multiple element arrangements.

Services

The terms of service contracts generally range from less

than one year up to ten years. Revenue from time and mate-

rial service contracts is recognized as the services are

provided. Revenue from Strategic Outsourcing Service con-

tracts reflects the extent of actual services delivered in the

period in accordance with the terms of the contract.

Revenue from Business Innovation Services (BIS) contracts

requiring the delivery of unique products and/or services is

recognized using the percentage-of-completion (POC)

method of accounting. In using the POC method, the com-

pany records revenue by reference to the costs incurred to

date and the estimated costs remaining to fulfill the con-

tracts. Provisions for losses are recognized during the period

in which the loss first becomes apparent. Revenue from

maintenance is recognized over the contractual period or as

the services are performed.

In some of the company’s services contracts, the com-

pany bills the customer prior to performing the service.

This situation gives rise to deferred income of $2.4 billion

and $2.5 billion at December 31, 2001 and 2000, respectively,

included in Deferred income on the Consolidated Statement

of Financial Position. In other services contracts, the company

performs the service prior to billing the customer. This situa-

tion gives rise to unbilled accounts receivable of $1.3 billion

and $1.2 billion at December 31, 2001 and 2000, respectively,

included in Notes and accounts receivable

—

trade on the

Consolidated Statement of Financial Position. In these

circumstances, billings usually occur shortly after the com-

pany performs the services and can range up to six months

later. Unbilled receivables are expected to be billed and col-

lected within nine months.

Hardware

Revenue from hardware sales or sales-type leases is recog-

nized when the product is shipped to the customer and there

are no unfulfilled company obligations that affect the cus-

tomer’s final acceptance of the arrangement. Any cost of

these obligations is accrued when the corresponding revenue

is recognized. Revenue from rentals and operating leases is

recognized monthly as the fees accrue.

Software

Revenue from one-time charge licensed software is recognized

at the inception of the license term. Revenue from monthly

software licenses is recognized ratably over the license term.

Revenue from maintenance, unspecified upgrades and tech-

nical support is recognized over the period such items are

delivered. See “Multiple Element Arrangements” below for

further information.

Financing

Revenue from financing is recognized at level rates of return

over the term of the lease or receivable.

Multiple Element Arrangements

The company enters into transactions that include multiple

element arrangements, which may include any combination

of hardware, services or software. These arrangements and

stand-alone software arrangements may also involve any com-

bination of software maintenance, software technical support

or unspecified software upgrades. When some elements are