Holiday Inn 2008 Annual Report Download - page 8

Download and view the complete annual report

Please find page 8 of the 2008 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

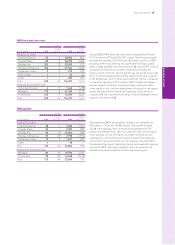

6IHGAnnual Report and Financial Statements 2008

This Business Review for the financial year ended 31 December 2008 provides a review of the

business and strategy of InterContinental Hotels Group PLC (the Group or IHG), commentaries

on the development and performance of the business, employee and environmental matters

and a description of the risks and uncertainties impacting the business.

Business overview

Market and competitive environment

Global economic events and industry cycle

The unprecedented financial events of late 2008 and the resulting

global recession are having, and will continue to have, a significant

impact on IHG and the wider hotel industry. IHG’s share price fell

by 36% in 2008 and, although we outperformed our peers,

whose aggregate share price fell by 49%, this is a major change

in sentiment. We continue to monitor key trends and indicators

to ensure our strategy remains well suited to the developing

environment and our capabilities. In essence, we believe our

business is resilient and, accordingly, our strategy remains

unchanged. However, we see short-term risks in the pace of

future openings, availability of debt and consumer demand.

None of these factors is expected to require major change

to our strategy and we remain focused on the medium to

long term, while we protect short-term profitability.

It is beyond doubt that this downturn is severe, with a sharp decline

in revenue per available room (RevPAR) and bookings. However, we

believe we are well placed to manage through this economic

situation, despite its severity. While the current downturn is unusual

in its rapidity, unpredictability and degree of credit restriction, our

industry has always been cyclical. Traditionally we have seen

periods of five to eight years of RevPAR growth followed by up to

two years of declines in RevPAR. Demand has rarely fallen for

sustained periods and it is the interplay between hotel supply and

demand in the industry that drives longer-term fluctuations in

RevPAR. The Group’s fee-based profit is partly protected from

changes in hotel supply due to its model of third-party ownership of

hotels under IHG management and franchise contracts. IHG profit

varies more with hotel revenue (demand) than it does with hotel

profit performance. We believe we are well placed over the coming

year compared with competitors who own hotels, rather than

simply operate them, as IHG does.

Market size

The global hotel market has an estimated room capacity of 17.5

million rooms. This has grown at approximately 2% per annum over

the last five years. Competitors in the market include other large

hotel companies and independently owned hotels.

The market remains fragmented, with an estimated 7.7 million

branded hotel rooms (approximately 45% of the total market). IHG

has an estimated 8% share of the branded market (approximately

3% of the total market). The top six major companies, including

IHG, together control approximately 42% of the branded rooms,

only 19% of total hotel rooms.

Geographically, the market is more concentrated with the top 20

countries accounting for 80% of global hotel rooms. Within this,

the United States (US) is dominant (more than 25% of global hotel

rooms) with China, Japan and Italy being the next largest markets.

The Group’s brands have more leadership positions (top three by

room numbers) in the six largest geographic markets than any

other major hotel company.

Drivers of growth

US market data historically indicates a steady increase in hotel

industry revenues, broadly in line with Gross Domestic Product,

with growth of approximately 1.5% per annum in real terms

since 1967.

Globally, we believe demand is driven by a number of underlying

trends:

• change in demographics – as the population ages and becomes

wealthier, increased leisure time and income encourages more

travel and hotel visits: younger generations are increasingly

seeking work/life balance, with positive implications for

increased leisure travel;

• increase in travel volumes as low-cost airlines grow rapidly;

• globalisation of trade and tourism;

• increase in affluence and freedom to travel within emerging

markets, such as China; and

• increase in the preference for branded hotels amongst

consumers.

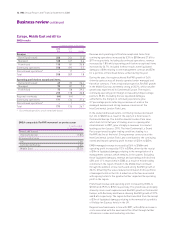

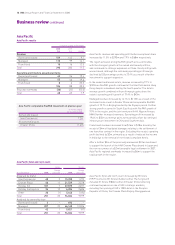

Branded v unbranded

2007 branded hotel rooms by region

as a percentage of the total market

US 69%

Europe, Middle East and Africa (EMEA) 33%

Asia Pacific 29%

Source: IHG analysis, Northstar Travel Management, Smith Travel Research (STR).

Within the global market, a relatively low proportion of hotel rooms

is branded; however, there has been an increasing trend towards

branded rooms. Over the last three years, the branded market

(as represented by the nine major global branded hotel companies)

has grown at a 3.6% compound annual growth rate (CAGR), over

twice as quickly as the overall market, implying an increased

preference towards branded hotels. Branded companies are

therefore gaining market share at the expense of unbranded

companies. IHG is well positioned to benefit from this trend. Hotel

owners are increasingly recognising the benefits of working with

IHG which can offer a portfolio of brands to suit the different real

estate opportunities an owner may have, together with effective

revenue delivery through global reservation channels. Furthermore,

hotel ownership is increasingly being separated from hotel

operations, encouraging hotel owners to use third parties such

as IHG to manage or franchise their hotels.

Other factors

Potential negative trends impacting hotel industry growth include

the possibility of increased terrorism, environmental considerations

and economic factors such as those now prevailing, namely

recession and global credit restrictions.

Business review