Holiday Inn 2008 Annual Report Download - page 60

Download and view the complete annual report

Please find page 60 of the 2008 Holiday Inn annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

|

|

58 IHG Annual Report and Financial Statements 2008

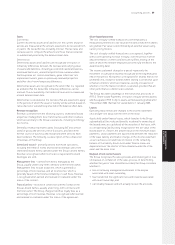

Trade receivables

Trade receivables are recorded at their original amount less

provision for impairment. It is the Group’s policy to provide for 100%

of the previous month’s aged receivables balances which are more

than 180 days past due. Adjustments to the policy may be made

due to specific or exceptional circumstances when collection is no

longer considered probable. The carrying amount of the receivable

is reduced through the use of a provision account and movements

in the provision are recognised in the income statement within cost

of sales. When a previously provided trade receivable is

uncollectable, it is written off against the provision.

Cash and cash equivalents

Cash comprises cash in hand and demand deposits.

Cash equivalents are short-term highly liquid investments

with an original maturity of three months or less that are readily

convertible to known amounts of cash and subject to insignificant

risk of changes in value.

In the cash flow statement cash and cash equivalents are shown

net of short-term overdrafts which are repayable on demand and

form an integral part of the Group’s cash management.

Assets held for sale

Non-current assets and associated liabilities are classified

as held for sale when their carrying amount will be recovered

principally through a sale transaction rather than continuing

use and a sale is highly probable.

Assets designated as held for sale are held at the lower of carrying

amount at designation and fair value less costs to sell.

Depreciation is not charged against property, plant and equipment

classified as held for sale.

Trade payables

Trade payables are non-interest-bearing and are stated at their

nominal value.

Loyalty programme

The hotel loyalty programme, Priority Club Rewards, enables

members to earn points, funded through hotel assessments,

during each stay at an IHG branded hotel and redeem the points at

a later date for free accommodation or other benefits. The future

redemption liability is included in trade and other payables and

is estimated using eventual redemption rates determined by

actuarial methods and points values.

The Group pays interest to the loyalty programme on the

accumulated cash received in advance of redemption of the

points awarded.

Self insurance

The Group is self-insured for various insurable risks including

general liability, workers’ compensation and employee medical

and dental coverage. Insurance reserves include projected

settlements for known and incurred but not reported claims.

Projected settlements are estimated based on historical trends

and actuarial data.

Provisions

Provisions are recognised when the Group has a present obligation

as a result of a past event, it is probable that a payment will be

made and a reliable estimate of the amount payable can be made.

If the effect of the time value of money is material, the provision

is discounted.

Bank and other borrowings

Bank and other borrowings are initially recognised at the fair value

of the consideration received less directly attributable transaction

costs. They are subsequently measured at amortised cost. Finance

charges, including issue costs, are charged to the income

statement using an effective interest rate method.

Borrowings are classified as non-current when the repayment date

is more than 12 months from the balance sheet date or where they

are drawn on a facility with more than 12 months to expiry.

Retirement benefits

Defined contribution plans

Payments to defined contribution schemes are charged to the

income statement as they fall due.

Defined benefit plans

Plan assets are measured at fair value and plan liabilities are

measured on an actuarial basis, using the projected unit credit

method and discounting at an interest rate equivalent to the

current rate of return on a high quality corporate bond of equivalent

currency and term to the plan liabilities. The difference between

the value of plan assets and liabilities at the balance sheet date

is the amount of surplus or deficit recorded on the balance sheet

as an asset or liability. An asset is recognised when the employer

has an unconditional right to use the surplus at some point during

the life of the plan or on its wind up. If a refund would be subject to

a tax other than income tax, as is the case in the UK, the asset is

recorded at the amount net of the tax.

The service cost of providing pension benefits to employees for

the year is charged to the income statement. The cost of making

improvements to pensions is recognised in the income statement

on a straight-line basis over the period during which any increase

in benefits vests. To the extent that improvements in benefits vest

immediately, the cost is recognised immediately as an expense.

Actuarial gains and losses may result from: differences between

the expected return and the actual return on plan assets;

differences between the actuarial assumptions underlying the plan

liabilities and actual experience during the year; or changes in the

actuarial assumptions used in the valuation of the plan liabilities.

Actuarial gains and losses, and taxation thereon, are recognised

in the Group statement of recognised income and expense.

Actuarial valuations are normally carried out every three years and

are updated for material transactions and other material changes

in circumstances (including changes in market prices and interest

rates) up to the balance sheet date.

Accounting policies continued