Haier 2006 Annual Report Download - page 62

Download and view the complete annual report

Please find page 62 of the 2006 Haier annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

|

|

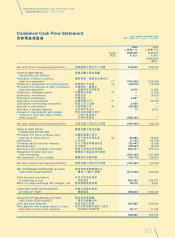

61

Haier Electronics Group Co., Ltd. Annual Report 2006

海爾電器集團有限公司 二零零六年年報

Notes to Financial Statements

財務報表附註 (31 December 2006)

(二零零六年十二月三十一日)

3.2 IMPACT OF NEW AND REVISED HONG KONG

FINANCIAL REPORTING STANDARDS

(Cont’d)

(c) HK(IFRIC)-Int 4 Determining whether an Arrangement

contains a Lease

The Group has adopted this interpretation as of 1

January 2006, which provides guidance in determining

whether arrangements contain a lease to which lease

accounting must be applied. This interpretation has had

no material impact on these financial statements.

3.3 IMPACT OF ISSUED BUT NOT YET EFFECTIVE

HONG KONG FINANCIAL REPORTING

STANDARDS

The Group has not applied the following new and revised

HKFRSs that have been issued but are not yet effective, in

these financial statements.

HKAS 1 Amendment Capital Disclosures

HKFRS 7 Financial Instruments: Disclosures

HKFRS 8 Operating Segment

HK(IFRIC)-Int 7 Applying the Restatement Approach under

HKAS 29

Financial Reporting in

Hyperinflationary Economies

HK(IFRIC)-Int 8 Scope of HKFRS 2

HK(IFRIC)-Int 9 Reassessment of Embedded Derivatives

HK(IFRIC)-Int 10 Interim Financial Reporting and Impairment

HK(IFRIC)-Int 11 HKFRS 2 — Group and Treasury Share

Transactions

HK(IFRIC)-Int 12 Service Concession Arrangements

The HKAS 1 Amendment shall be applied for annual periods

beginning on or after 1 January 2007. The revised standard

will affect the disclosures about qualitative information about

the Group’s objective, policies and processes for managing

capital; quantitative data about what the Company regards as

capital; and compliance with any capital requirements and

the consequences of any non-compliance.

3.2 新訂及經修訂香港財務報告準則之

影響

(續)

(c) 香港(國際財務匯報準則)詮釋第4

號釐定安排是否包含租賃

本集團已於二零零六年一月一日採

納此詮釋,此詮釋為釐定安排是否

包含租賃提供必須應用租賃會計之

指引。此詮釋對此等財務報表並無

構成重大影響。

3.3 已頒佈但尚未生效之香港財務報告

準則之影響

本集團尚未於此等財務報表採納下列已

頒佈但尚未生效之新訂及經修訂香港財

務報告準則。

香港會計準則第1號 資本披露

(修訂)

香港財務報告準則 金融工具:披露

第7號

香港財務報告準則 經營分類

第8號

香港(國際財務匯報 根據香港會計準則

準則)詮釋第7號第29號

嚴重通貨

膨脹經濟中之財務

報告

採用重列法

香港(國際財務匯報 香港財務報告準則

準則)詮釋第8號第2號的範圍

香港(國際財務匯報 重新評估內含衍生

準則)詮釋第9號工具

香港(國際財務匯報 中期財務報告及

準則)詮釋第10號減值

香港(國際財務匯報 香港財務報告準則

準則)詮釋第11號第2號 — 集團及

庫存股份交易

香港(國際財務匯報 服務特許權安排

準則)詮釋第12號

香港會計準則第1 號(修訂)須於二零零

七年一月一日或之後開始之年度期間應

用。經修訂準則影響本集團管理資本之

目標、政策及過程之定性資料、本公司

視作資本項目之定量數據及已符合之任

何資本規定及不符合的影響之後果之披

露。