HSBC 2014 Annual Report Download - page 4

Download and view the complete annual report

Please find page 4 of the 2014 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

|

|

HSBC BANK PLC

Strategic Report: Purpose and Strategic Objectives

2

Our Purpose and Strategic

Objectives

The purpose of HSBC Bank plc is to connect customers to

opportunities, enable businesses to thrive and

economies to prosper, and ultimately help people to

fulfil their hopes and realise their ambitions.

Our strategic priorities

HSBC aims to be the world’s leading and most respected

international bank. We will achieve this by focusing on

the needs of our customers and the societies we serve,

thereby delivering long-term sustainable value to all our

stakeholders.

In 2013, HSBC announced a set of three interconnected

and equally weighted priorities for 2014 to 2016 to help

us deliver our strategy:

• grow the business and dividends;

• implement Global Standards; and

• streamline processes and procedures.

Each priority is complementary and underpinned by

initiatives being undertaken within our day-to-day

business. Together they create value for our customers

and contribute to the long-term sustainability of the

group and HSBC.

In Europe the group’s aim is to be the leading and most

respected international bank connecting Europe with the

rest of the world. On an operational level the group has

developed a strategy for each of four global businesses

following HSBC’s strategic priorities while also focusing

on increasing capital and cost efficiency.

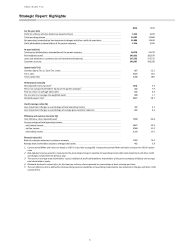

How we measure performance

We track our progress in implementing our strategy with

a range of financial and non-financial measures or key

performance indicators. These are set out on page 11.

From 2015 we have revised our targets to better reflect

the changing regulatory and operating environment.

Value creation

Within the group we continue to follow the vision for the

long-term direction of HSBC which was first outlined in

2011 along with a clear strategy that will help us achieve

it. Our strategy guides where and how we seek to

compete. We constantly assess our progress against this

strategy and provide regular updates to stakeholders.

Through our principal activities – making payments,

holding savings, enabling trade, providing finance and

managing risks – we play a central role in society and in

the economic system. Our target is to build and maintain

a business which is sustainable in the long term.

How we create value

Banks, and the individuals within them, play a crucial role

in the economic and social system, creating value for

many parties in different ways.

We provide a facility for customers to securely and

conveniently deposit their savings. We allow funds to

flow from savers and investors to borrowers, either

directly or through the capital markets. The borrowers

use these loans or other forms of credit to buy goods or

invest in businesses. By these means, we help the

economy to convert savings which may be individually

short-term into financing which is, in aggregate, longer

term. We bring together investors and people looking for

investment funding and we develop new financial

products. We also facilitate personal and commercial

transactions by acting as payment agent both within

countries and internationally. Through these activities,

we take on risks which we then manage and reflect in

our prices.

Our direct lending includes residential and commercial

mortgages and overdrafts, and term loan facilities. We

finance importers and exporters engaged in international

trade and provide advances to companies secured on

amounts owed to them by their customers.

We also offer additional financial products and services

including broking, asset management, financial advisory,

life insurance, corporate finance, securities services and

alternative investments. We make markets in financial

assets so that investors have confidence in efficient

pricing and the availability of buyers and sellers. We

provide these products for clients ranging from

governments to large and mid-market corporates, small

and medium-sized enterprises, high net worth

individuals and retail customers. We help customers

raise financing from external investors in debt and equity

capital markets. We create liquidity and price

transparency in these securities allowing investors to buy

and sell them on the secondary market. We exchange

national currencies, helping international trade.

We offer products that help a wide range of customers

to manage their risks and exposures through, for

example, life insurance and pension products for retail

customers and receivables finance or documentary trade

instruments for companies. Corporate customers also

ask us to help with managing the financial risks arising in

their businesses by employing our expertise and market

access.

An important way of managing risks arising from changes

in asset and liability values and movements in rates is

provided by derivative products such as forwards,

futures, swaps and options. In this connection, we are an

active market-maker and derivative counterparty.

Customers use derivatives to manage their risks, for

example, by:

• using forward foreign currency contracts to hedge

their income from export sales or costs of imported

materials;

• using an inflation swap to hedge future inflation-

linked liabilities, for example, for pension payments;

• transforming variable payments of debt interest into

fixed rate payments, or vice versa; or

• providing investors with hedges against movements

in markets or particular stocks.

We charge customers a spread, representing the

difference between the price charged to the customer

and the theoretical cost of executing an offsetting hedge