CarMax 2010 Annual Report Download - page 66

Download and view the complete annual report

Please find page 66 of the 2010 CarMax annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

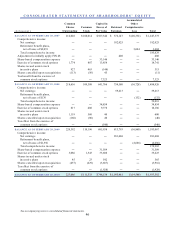

|

|

56

Financial Covenants and Performance Triggers

The securitization agreement related to the warehouse facility includes various financial covenants and performance

triggers. The financial covenants include a maximum total liabilities to tangible net worth ratio and a minimum

fixed charge coverage ratio. Performance triggers require that the pool of securitized receivables in the warehouse

facility achieve specified thresholds related to portfolio yield, loss rate and delinquency rate. If these financial

covenants and/or thresholds are not met, we could be unable to continue to securitize receivables through the

warehouse facility. In addition, the warehouse facility investors would charge us a higher rate of interest and could

have us replaced as servicer. Further, we could be required to deposit collections on the securitized receivables with

the warehouse agent on a daily basis and deliver executed lockbox agreements to the warehouse facility agent. As

of February 28, 2010, we were in compliance with the financial covenants and the securitized receivables were in

compliance with the performance triggers.

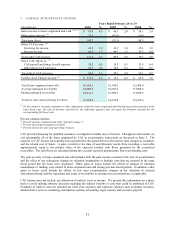

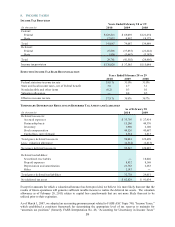

5. FINANCIAL DERIVATIVES

We utilize derivatives relating to our auto loan receivable securitizations and our investment in certain retained

subordinated bonds. Interest rate swaps are used to better match funding costs to the interest on the fixed-rate

receivables being securitized and the retained subordinated bonds, and to minimize the funding costs related to

certain of our securitization trusts. Swaps related to receivables funded in the warehouse facility are unwound when

those receivables are refinanced in a term securitization. During fiscal 2010, we entered into 80 interest rate swaps

with initial notional amounts totaling $1.86 billion and terms ranging from 15 to 41 months. The notional amount of

outstanding swaps totaled $473.6 million as of February 28, 2010, and $1.36 billion as of February 28, 2009.

Interest rate caps are used to limit risk for investors in our warehouse facility. During fiscal 2010, we entered into

six interest rate caps, with terms ranging from 48 to 53 months. As of February 28, 2010, we were party to six

interest rate caps, three of which were assets and three were liabilities, and as a result the net effect on the

consolidated balance sheet was not material.

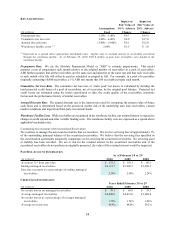

FAIR VALUE OF DERIVATIVE INSTRUMENTS (1)

(In thousands) Consolidated Balance Sheets

Asset derivatives:

Interest rate swaps Retained interest in securitized receivables ―$ 33$

Interest rate swaps Prepaid expenses and other current assets 1,279 ―

Interest rate swaps Accounts payable ― 52

Interest rate caps Prepaid expenses and other current assets 1,999 ―

Liability derivatives:

Interest rate swaps Accounts payable (7,171) (30,590)

Interest rate caps Prepaid expens es and other current ass ets (1,982) ―

Total (5,875)$ (30,505)$

As of February 28

20092010

CHANGES IN FAIR VALUE OF DERIVATIVE INSTRUMENTS (1)

(In thousands) Consolidated S tatements of Earnings

Los s on derivatives CarM ax A uto Finance income (8,547)$ (15,214)$ (14,107)$

2010 2009 2008

Years Ended February 28 or 29

(1) Additional information on fair value measurements is included in Note 6.

The market and credit risks associated with interest rate swaps and caps are similar to those relating to other types of

financial instruments. Market risk is the exposure created by potential fluctuations in interest rates. We do not

anticipate significant market risk from swaps as they are predominantly used to match funding costs to the use of the

funding. However, disruptions in the credit markets could impact the effectiveness of our hedging strategies. Credit

risk is the exposure to nonperformance of another party to an agreement. We mitigate credit risk by dealing with

highly rated bank counterparties.

6. FAIR VALUE MEASUREMENTS

Fair value is defined as the price that would be received to sell an asset or paid to transfer a liability in an orderly

transaction between market participants in the principal market, or if none exists, the most advantageous market, for

the specific asset or liability at the measurement date (referred to as the “exit price”). The fair value should be based

on assumptions that market participants would use, including a consideration of nonperformance risk.