Blackberry 2010 Annual Report Download - page 74

Download and view the complete annual report

Please find page 74 of the 2010 Blackberry annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

|

|

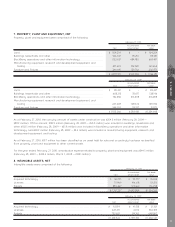

guidance on disclosure requirements around disaggregation and valuation techniques for both recurring and non-

recurring fair value measurements in either Level 2 or Level 3. The new authoritative guidance is effective for interim and

annual periods beginning after December 15, 2009, except for the requirement to separately disclose purchases, sales,

issuances and settlements in the Level 3 reconciliation which is effective for interim and annual periods beginning after

December 15, 2010. The Company will adopt the guidance in the first quarter of fiscal 2011 and the first quarter of fiscal

2012, respectively. The Company is currently evaluating the impact that the adoption of this guidance will have on its

financial statement disclosures.

In October 2009, the FASB issued authoritative guidance on revenue recognition for arrangements with multiple

deliverables. The guidance amends previous literature to require an entity to use an estimated selling price when vendor

specific objective evidence or acceptable third party evidence does not exist for any products or services included in a

multiple element arrangement. The arrangement consideration should be allocated among the products and services

based upon their relative selling prices, thus eliminating the use of the residual method of allocation. The guidance also

requires expanded qualitative and quantitative disclosures regarding significant judgements made and changes in

applying the guidance. The new authoritative guidance is effective for revenue arrangements entered into or materially

modified in fiscal years beginning after June 15, 2010 with early application permitted. The Company plans to adopt the

guidance in the first quarter of fiscal 2011 and the Company does not expect the adoption will have a material impact on

the Company’s results of operations and financial condition.

In October 2009, the FASB issued authoritative guidance on certain revenue arrangements that include software elements.

The guidance amends previous literature to exclude tangible products containing software components and non-software

components that function together to deliver the product’s essential functionality from applying software revenue

recognition guidance to those products. The new authoritative guidance is effective for revenue arrangements entered into

or materially modified in fiscal years on or after June 15, 2010 with early application permitted. The Company plans to

adopt the guidance in the first quarter of fiscal 2011 and the Company does not expect the adoption will have a material

impact on the Company’s results of operations and financial condition.

In June 2009, the FASB issued authoritative guidance to amend the manner in which an enterprise performs an analysis to

determine whether the enterprise’s variable interest gives it a controlling interest in the variable interest entity (“VIE”). The

guidance uses a qualitative risks and rewards approach by focusing on which enterprise has the power to direct the

activities of the VIE, the obligation to absorb the entity’s losses and rights to receive benefits from the entity. The guidance

also requires enhanced disclosures related to the VIE. The new authoritative guidance is effective for annual periods

beginning after November 15, 2009. The Company will adopt the guidance in the first quarter of fiscal 2011 and the

Company does not expect the adoption will have a material impact on the Company’s results of operations and financial

condition.

In June 2009, the FASB issued authoritative guidance amending the accounting for transfers of financial assets. The

guidance, among other things, eliminates the exceptions for qualifying special-purpose entities from the consolidation

guidance, clarifies the requirements for transferred financial assets that are eligible for sale accounting and requires

enhanced disclosures about a transferor’s continuing involvement with transferred financial assets. This new authoritative

guidance is effective for annual periods beginning after November 15, 2009. The Company will adopt the guidance in the

first quarter of fiscal 2011 and the Company does not expect the adoption will have a material impact on the Company’s

results of operations and financial condition.

In November 2008, the SEC announced a proposed roadmap for comment regarding the potential use by U.S. issuers of

financial statements prepared in accordance with International Financial Reporting Standards (“IFRS”). IFRS is a

comprehensive series of accounting standards published by the International Accounting Standards Board. On

February 24, 2010, the SEC issued a statement describing its position regarding global accounting standards. Among other

things, the SEC stated that it has directed its staff to execute a work plan which will include consideration of IFRS as it

exists today and after completion of various “convergence” projects currently underway between U.S. and international

accounting standards setters. By 2011, assuming completion of certain projects and the SEC staff’s work plan, the SEC will

decide whether to incorporate IFRS into the U.S. financial reporting system. The Company is currently assessing the impact

that this proposed change would have on the consolidated financial statements, accompanying notes and disclosures,

and will continue to monitor the development of the potential implementation of IFRS.

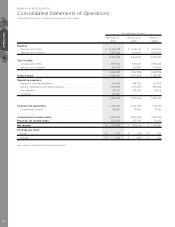

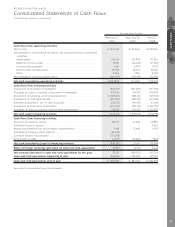

RESEARCH IN MOTION LIMITED

Notes to the Consolidated Financial Statements continued

In thousands of United States dollars, except share and per share data, and except as otherwise indicated

NOTE 3

66