Blackberry 2007 Annual Report Download - page 73

Download and view the complete annual report

Please find page 73 of the 2007 Blackberry annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

72 -

73

73 -

74

74 -

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

71

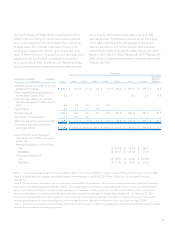

No. 123, Accounting for Stock-Based Compensation, however,

SFAS 123(R) requires the Company to factor in an expected

forfeiture rate in establishing the expense while under SFAS

123 the Company accounted for forfeitures as they occurred.

The Company is using the MPT method as permitted by

SFAS 123(R) to record stock-based compensation expense

and accordingly prior periods have not been restated to

reflect the impact of SFAS 123(R). Stock-based compensation

expense calculated using the MPT approach is recognized on

a prospective basis in the financial statements for all new and

unvested stock options that are ultimately expected to vest as

the requisite service is rendered beginning in the Company’s

fiscal 2007 year. Stock-based compensation expense for

awards granted prior to fiscal 2007 is based on the grant-date

fair value as determined under the pro forma provisions of

SFAS 123. As a result of the Company adopting SFAS 123(R)

in the first quarter of fiscal 2007, the Company’s net income

for the year ended March 3, 2007 included stock-based

compensation expense of $18.8 million or $0.10 per share

basic and diluted.

Accounting Changes and Error Corrections

In May 2005, the FASB issued SFAS 154 Accounting Changes

and Error Corrections. SFAS 154 replaces APB Opinion

20 (“APB 20”) and SFAS 3, with many of those provisions

being carried forward without change. If practical, SFAS

154 requires retrospective application to prior year’s

financial statements for a voluntary change in accounting

principle. In addition, SFAS 154 also requires that a change

in depreciation method for long-lived non-financial assets

be accounted for as a change in estimate, as opposed to a

change in accounting principle under APB 20. The standard

is effective for fiscal years beginning after December 15,

2005. The Company has adopted SFAS 154 and it had no

impact on the Company’s operating results in fiscal 2007.

Considering the Effects of Prior Year Misstatements when

Quantifying Misstatements in Current Year Financial

Statements

In September 2006, the SEC issued Staff Accounting Bulletin

No. 108 (“SAB 108”) Considering the Effects of Prior Year

Misstatements when Quantifying Misstatements in Current

Year Financial Statements. SAB 108 requires that a company

consider and evaluate materiality with respect to identified

unadjusted errors using both a rollover and iron curtain

approach. The rollover approach quantifies a misstatement

based on the identified unadjusted item originating in the

current year income statement and ignores any portion of

the misstatement that originated in a prior period. The iron

curtain approach quantifies misstatements that exist in the

balance sheet at the end of the current period regardless of

the period of origin. Financial statements would be required

to be adjusted when either approach results in quantifying

a misstatement that is material. SAB 108 is effective for the

Company’s 2007 fiscal year and there is no effect on the

Company’s financial position, results of operations or cash

flows.

3. RECENTLY ISSUED PRONOUNCEMENTS

Accounting for Certain Hybrid Financial Instruments

In February 2006, the FASB issued SFAS 155 Accounting

for Certain Hybrid Financial Instruments. SFAS 155 amends

SFAS 133 and among other things, permits fair value

remeasurement for any hybrid financial instrument that

contains an embedded derivative that otherwise would

require bifurcation. SFAS 155 is in effect for fiscal years

beginning after September 15, 2006 and the Company will

be required to adopt the standard in the first quarter of fiscal

2008. The Company is currently evaluating what impact, if

any, SFAS 155 will have on its financial statements.

Fair Value Measurements

In September 2006, the FASB issued SFAS 157 Fair Value

Measurements. SFAS 157 clarifies the definition of fair value,

establishes a framework for measurement of fair value, and

expands disclosure about fair value measurements. SFAS

157 is effective for fiscal years beginning after December 15,

2007 and the Company will be required to adopt the standard

in the first quarter of fiscal 2009. The Company is currently

evaluating what impact, if any, SFAS 157 will have on its

financial statements.

Accounting for Uncertainty in Income Taxes

In July 2006, the FASB issued FASB Interpretation No. 48

(“FIN 48”) Accounting for Uncertainty in Income Taxes. FIN 48

clarifies the accounting for uncertainty in tax positions subject

to SFAS 109 Accounting for Income Taxes. FIN 48 provides

a recognition threshold and a mechanism to measure and

record tax positions taken, or expected to be taken during

the filing of tax returns. The mechanism is a two-step

process in which the tax position is evaluated for recognition