Blackberry 2007 Annual Report Download - page 18

Download and view the complete annual report

Please find page 18 of the 2007 Blackberry annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

18 -

19

19 -

20

20 -

21

21 -

22

22 -

23

23 -

24

24 -

25

25 -

26

26 -

27

27 -

28

28 -

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

|

|

16

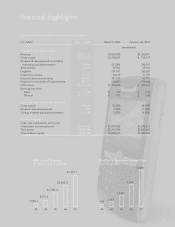

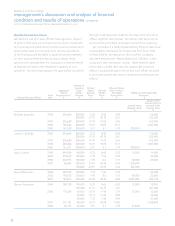

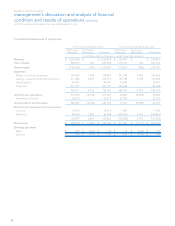

RESEARCH IN MOTION LIMITED

management’s discussion and analysis of financial

condition and results of operations continued

FOR THE THREE MONTHS AND FISCAL YEAR ENDED MARCH 3, 2007

The Special Committee determined that the Company

failed to maintain adequate internal and accounting controls

with respect to the issuance of options in compliance with

the Stock Option Plan, both in terms of how options were

granted and documented, and the measurement date used

to account for certain option grants. The grant process

was characterized by informality and a lack of definitive

documentation as to when the accounting measurement

date for a stock option occurred, and lacked safeguards to

ensure compliance with applicable accounting, regulatory

and disclosure rules. The Special Committee did not find

intentional misconduct on the part of any director, officer

or employee responsible for the administration of the

Company’s stock option grant program.

Nature of the Errors

The period covered by the Review spans the inception of the

Stock Option Plan in December 1996 to August 2006. The

Special Committee also examined certain stock-based awards

granted prior to the adoption of the Stock Option Plan. As was

permitted prior to fiscal 2007, the Company elected to use

APB 25 to measure and recognize compensation cost for all

awards granted to employees for their service as employees,

as discussed in Note 1 to the Consolidated Financial

Statements. APB 25 is based upon an intrinsic value method

of accounting for stock-based compensation. Under this

method, compensation cost is measured as the excess, if any,

of the quoted market price of the stock at the measurement

date over the amount to be paid by the employee.

Under APB 25, the measurement date for determining

compensation cost of stock options is the first date on which

are known both (1) the number of shares that an individual

employee is entitled to receive and (2) the option exercise

price. If either the number of shares or the exercise price

(or both) of a particular award are not known on the grant

date, the Company must remeasure compensation cost at

each reporting date until both are known. The application

of this principle is referred to as variable plan accounting,

and requires the Company to remeasure compensation

cost at the award’s intrinsic value until a measurement date

is triggered. When both terms are known, the award is

referred to as a fixed award, and compensation cost is not

remeasured for any changes in intrinsic value subsequent to

the measurement date.

The Review identified three significant types of accounting

errors being: (1) the misapplication of U.S. GAAP as it

relates to a “net settlement” feature contained in the

Stock Option Plan until February 27, 2002, which resulted

in variable accounting treatment, (2) the misapplication

of U.S. GAAP in the accounting for certain share awards

granted prior to the adoption of the Stock Option Plan,

which also resulted in variable accounting treatment and

(3) the misapplication of U.S. GAAP in the determination of

an accounting measurement date for options granted after

February 27, 2002. As a result of these errors, the Company

has recorded additional non-cash adjustments for stock-

based compensation expense in accordance with APB 25.

In addition, the Restatement also records adjustments to

certain tax amounts related to the accounting for stock-based

compensation as more fully described below. The following

table sets forth the impact of the additional non-cash

charges for stock-based compensation expense (benefit) on

net income (loss) for the fiscal years ended March 4, 2006,

February 26, 2005, February 28, 2004, March 1, 2003,

March 2, 2002, February 28, 2001, February 29, 2000, and the

cumulative adjustment to the fiscal year ended February 28,

1999: