Berkshire Hathaway 2007 Annual Report Download - page 61

Download and view the complete annual report

Please find page 61 of the 2007 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

51 -

52

52 -

53

53 -

54

54 -

55

55 -

56

56 -

57

57 -

58

58 -

59

59 -

60

60 -

61

61 -

62

62 -

63

63 -

64

64 -

65

65 -

66

66 -

67

67 -

68

68 -

69

69 -

70

70 -

71

71 -

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

60

Management’s Discussion (Continued)

Investment and Derivative Gains/Losses (Continued)

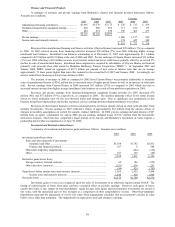

In each of the past three years, pre-tax investment gains from sales and other disposals primarily derived from equity

securities. In 2005, pre-tax investment gains from sales and other disposals included a non-cash pre-tax gain of approximately

$5 billion from Berkshire’ s exchange of common stock of The Gillette Company (“Gillette”), which Berkshire held for many

years, for shares of The Procter & Gamble Company (“PG”), which PG issued in its acquisition of Gillette. Berkshire’ s

management does not regard the gain recorded, as required under GAAP, as meaningful. The gain recognized for financial

reporting purposes is deferred for income tax purposes. The transaction essentially had no effect on Berkshire’ s consolidated

shareholders’ equity because the gain was accompanied by a corresponding reduction of unrealized investment gains included in

accumulated other comprehensive income.

Derivative gains and losses from foreign currency forward contracts arise as the value of the U.S. dollar changes

against certain foreign currencies. The notional value of open foreign currency forward contracts was approximately $14 billion

as of December 31, 2005 but has declined to an immaterial amount at December 31, 2007. During 2005, the value of most

foreign currencies decreased relative to the U.S. dollar and these contracts produced losses.

Other derivative contracts primarily pertain to credit default risks of other U.S. entities as well as equity price risks

associated with major worldwide equity indices. Such contracts are carried at estimated fair value and changes in estimated fair

value are included in earnings in the period of the change. The gains/losses from such contracts are principally attributable to

non-cash changes in the fair values of the related contracts and reflect changes in applicable underlying credit standing, equity

index values, interest rates, foreign currency exchange rates and other factors. These contracts generally may not be settled

before the expiration date (up to 20 years in the future with respect to equity index contracts) and therefore the amount of cash

basis gains or losses will not be known for years. Nevertheless, the fair values on any given reporting date and the resulting

gains and losses reflected in earnings will likely be volatile, reflecting the volatility of equity and credit markets.

The estimated fair value of equity index and credit default derivative contracts at December 31, 2007 was

approximately $6.4 billion, an increase of approximately $3.1 billion from December 31, 2006. The increase was primarily due

to new contracts entered into during the year for which Berkshire received premiums of approximately $2.9 billion. As of

December 31, 2007, Berkshire’ s maximum exposure under these contracts was approximately $40 billion, an increase of

approximately $16 billion from December 31, 2006.

Financial Condition

Berkshire’ s balance sheet continues to reflect significant liquidity and a strong capital base. Consolidated

shareholders’ equity at December 31, 2007 was $120.7 billion. Consolidated cash and invested assets, excluding assets of

finance and financial products businesses, was approximately $142.4 billion at December 31, 2007 (including cash and cash

equivalents of $38.9 billion) and $125.2 billion at December 31, 2006 (including cash and cash equivalents of $38.3 billion).

Berkshire’ s invested assets are held predominantly in its insurance businesses. A large amount of capital is maintained in the

insurance subsidiaries for strategic and marketing purposes and in support of reserves for unpaid losses. In the United States, in

particular, dividend payments by insurance companies are subject to prior approval by state regulators. For the year ending

December 31, 2007, Berkshire’ s insurance subsidiaries paid dividends of $4.9 billion.

During 2007, Berkshire made several relatively small business acquisitions for aggregate cash consideration of $1.6

billion. Additionally, Berkshire agreed in December 2007 to acquire a 60% interest in Marmon Holdings, Inc. (“Marmon”) for

$4.5 billion. This acquisition is subject to customary closing conditions, including regulatory approvals, and is expected to close

in March 2008. See Note 2 to the Consolidated Financial Statements for more information concerning the business acquisitions.

Berkshire believes that it currently maintains sufficient liquidity to cover its contractual obligations and provide for contingent

liquidity.

Notes payable and other borrowings of the insurance and other businesses were $2.7 billion (includes about $1.7

billion issued or guaranteed by Berkshire Hathaway Inc.) at December 31, 2007, a decrease of $1 billion from December 31,

2006, reflecting maturities and prepayments of $644 million of parent company debt, reductions in commercial paper

(principally NetJets) and repayments of other borrowings of subsidiaries. Berkshire issued 3,715 Class A equivalent shares of

common stock during 2007 in connection with the SQUARZ warrant exercises in exchange for $333 million.

Capital expenditures of the utilities and energy businesses were approximately $3.5 billion in 2007 and are forecasted

to be approximately $3.9 billion in 2008. MidAmerican expects to fund these capital expenditures with cash flows from

operations and debt proceeds. Certain of its borrowings are secured by certain assets of its regulated utility subsidiaries. During

2007, MidAmerican issued $3.55 billion par amount of new term debt and repaid $1.57 billion of previously issued debt

including net repayments of short-term borrowings. Term debt of MidAmerican maturing in 2008 is $1.97 billion with an

additional $3.16 billion due before 2013. Berkshire has committed until February 28, 2011 to provide up to $3.5 billion of

additional capital to MidAmerican to permit the repayment of its debt obligations or to fund its regulated utility subsidiaries.

Berkshire has not and does not intend to guarantee the repayment of debt by MidAmerican or any of its subsidiaries.

Assets of the finance and financial products businesses were $25.7 billion as of December 31, 2007 and $24.6 billion at

December 31, 2006, which consisted primarily of loans and finance receivables, fixed maturity securities and cash and cash

equivalents. Liabilities were $22.0 billion as of December 31, 2007 and $19.4 billion at December 31, 2006. As of December

31, 2007, notes payable and other borrowings of $12.1 billion included $8.9 billion par amount of medium-term notes issued by

BHFC. In 2007, BHFC issued $750 million par amount of notes due in 2012 and repaid $700 million par amount of notes that

matured. In 2008, an additional $3.1 billion par amount of notes will mature, including $1.25 billion that matured in January

2008. BHFC issued an additional $2.0 billion par amount of medium-term notes in January 2008. BHFC notes are unsecured

and mature at various dates extending through 2015. The proceeds from these notes are being used to finance originated and