Berkshire Hathaway 2000 Annual Report Download - page 6

Download and view the complete annual report

Please find page 6 of the 2000 Berkshire Hathaway annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

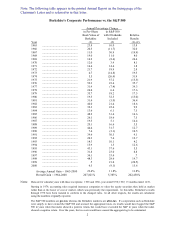

1

1 -

2

2 -

3

3 -

4

4 -

5

5 -

6

6 -

7

7 -

8

8 -

9

9 -

10

10 -

11

11 -

12

12 -

13

13 -

14

14 -

15

15 -

16

16 -

17

17 -

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

|

|

5

We quickly purchased CORT for Wesco, our 80%-owned subsidiary, paying about $386 million

in cash. You will find more details about CORT’s operations in Wesco’s 1999 and 2000 annual

reports. Both Charlie and I enjoy working with Paul, and CORT looks like a good bet to beat our

original expectations.

•Early last year, Ron Ferguson of General Re put me in contact with Bob Berry, whose family had

owned U.S. Liability for 49 years. This insurer, along with two sister companies, is a medium-

sized, highly-respected writer of unusual risks — “excess and surplus lines” in insurance jargon.

After Bob and I got in touch, we agreed by phone on a half-stock, half-cash deal.

In recent years, Tom Nerney has managed the operation for the Berry family and has achieved a

rare combination of excellent growth and unusual profitability. Tom is a powerhouse in other

ways as well. In addition to having four adopted children (two from Russia), he has an extended

family: the Philadelphia Belles, a young-teen girls basketball team that Tom coaches. The team

had a 62-4 record last year and finished second in the AAU national tournament.

Few property-casualty companies are outstanding businesses. We have far more than our share,

and U.S. Liability adds luster to the collection.

•Ben Bridge Jeweler was another purchase we made by phone, prior to any face-to-face meeting

between me and the management. Ed Bridge, who with his cousin, Jon, manages this 65-store

West Coast retailer, is a friend of Barnett Helzberg, from whom we bought Helzberg Diamonds

in 1995. Upon learning that the Bridge family proposed to sell its company, Barnett gave

Berkshire a strong recommendation. Ed then called and explained his business to me, also

sending some figures, and we made a deal, again half for cash and half for stock.

Ed and Jon are fourth generation owner-managers of a business started 89 years ago in Seattle.

Both the business and the family— including Herb and Bob, the fathers of Jon and Ed — enjoy

extraordinary reputations. Same-store sales have increased by 9%, 11%, 13%, 10%, 12%, 21%

and 7% over the past seven years, a truly remarkable record.

It was vital to the family that the company operate in the future as in the past. No one wanted

another jewelry chain to come in and decimate the organization with ideas about synergy and

cost saving (which, though they would never work, were certain to be tried). I told Ed and Jon

that they would be in charge, and they knew I could be believed: After all, it’s obvious that your

Chairman would be a disaster at actually running a store or selling jewelry (though there are

members of his family who have earned black belts as purchasers).

In their typically classy way, the Bridges allocated a substantial portion of the proceeds from their

sale to the hundreds of co-workers who had helped the company achieve its success. We’re

proud to be associated with both the family and the company.

•In July we acquired Justin Industries, the leading maker of Western boots — including the

Justin, Tony Lama, Nocona, and Chippewa brands and the premier producer of brick in Texas

and five neighboring states.

Here again, our acquisition involved serendipity. On May 4th, I received a fax from Mark Jones,

a stranger to me, proposing that Berkshire join a group to acquire an unnamed company. I faxed

him back, explaining that with rare exceptions we don’t invest with others, but would happily

pay him a commission if he sent details and we later made a purchase. He replied that the

“mystery company” was Justin. I then went to Fort Worth to meet John Roach, chairman of the

company and John Justin, who had built the business and was its major shareholder. Soon after,

we bought Justin for $570 million in cash.

John Justin loved Justin Industries but had been forced to retire because of severe health problems

(which sadly led to his death in late February). John was a class act as a citizen, businessman

and human being. Fortunately, he had groomed two outstanding managers, Harrold Melton at

Acme and Randy Watson at Justin Boot, each of whom runs his company autonomously.