Avon 2015 Annual Report Download - page 107

Download and view the complete annual report

Please find page 107 of the 2015 Avon annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

114 -

115

115 -

116

116 -

117

117 -

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

|

|

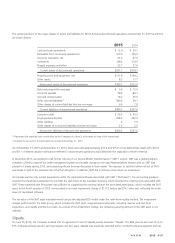

At December 31, 2015, we had recognized deferred tax assets of $746.1 relating to U.S. business credit carryforwards (excess foreign tax

credits, minimum tax credits, research and experimentation credits and investment tax credits) for which a valuation allowance of $746.1 has

been provided, deferred tax assets relating to foreign tax loss carryforwards of $656.9, for which a valuation allowance of $651.7 has been

provided and deferred tax assets relating to state tax loss carryforwards of $125.0 for which a valuation allowance of $125.0 has been

provided. The foreign tax loss carryforwards as of December 31, 2015 were $2,302.1, of which $2,134.6 are not subject to expiration and

$167.5 are subject to expiration between 2016 and 2030. The state tax loss carryforwards as of December 31, 2015 were $1,750.0 which

are subject to expiration between 2016 and 2035. The U.S. foreign tax credit carryforwards of $689.6 are subject to expiration between

2018 and 2025; the U.S. minimum tax credits of $35.9 are not subject to expiration; the U.S. research and experimentation credits of $16.3

are subject to expiration between 2027 and 2035 and the U.S. investment tax credits of $4.3 are subject to expiration between 2020 and

2030.

At December 31, 2015, we continue to assert that our foreign earnings are not indefinitely reinvested, as a result of our domestic liquidity

profile. Accordingly, we adjusted our deferred tax liability to account for the balance of our undistributed earnings of foreign subsidiaries

and for the tax effect of earnings that were actually repatriated to the U.S. during the year. We also adjusted our deferred tax liability to

exclude deferred tax assets of $94.9 associated with our foreign earnings that we do not plan to repatriate within the foreseeable future.

The deferred tax liability associated with the Company’s undistributed earnings increased by $74.9, resulting in a deferred tax liability

balance of $89.2 related to the incremental tax cost on $1.4 billion of undistributed foreign earnings at December 31, 2015. This deferred

income tax liability amount is net of the estimated foreign tax credits that would be generated upon the repatriation of such earnings. The

repatriation of foreign earnings may result in the utilization of a portion of our excess foreign tax credit carryforwards in the year of

repatriation; therefore the utilization of our foreign tax credit carryforwards is dependent on the amount and timing of repatriations, as well

as the jurisdictions involved. We have not included the undistributed earnings of our subsidiary in Venezuela in the calculation of this

deferred tax liability as local regulations restrict cash distributions denominated in U.S. dollars.

At December 31, 2015, the valuation allowance primarily represents amounts for all U.S. deferred tax assets, certain foreign tax loss

carryforwards and certain other foreign deferred tax assets. The recognition of deferred tax assets was based on the evaluation of current

and estimated future profitability of the operations, reversal of deferred tax liabilities and the likelihood of utilizing tax credit and/or loss

carryforwards. Tax planning strategies were also considered and evaluated as support for the realization of deferred tax assets. Where these

sources of income existed along with sufficient positive evidence that indicated it was more likely than not that such sources of income could

be relied upon, then the deferred tax assets were not reduced by a valuation allowance.

The net increase in the valuation allowance during 2015 of $609.5 was primarily due to the recording of the valuation allowances for U.S.

deferred tax assets (discussed further below), partially offset by the increase in the deferred tax liability for unremitted earnings of foreign

subsidiaries discussed above. In addition, the net increase in the valuation allowance was also attributable to additional valuation allowances

for deferred tax assets outside of the U.S., primarily in Russia, which was largely due to lower earnings and the impact of foreign exchange

losses on working capital balances.

During the first and second quarters of 2015, the Company recorded a $31.3 charge and a $3.2 benefit, respectively, associated with

valuation allowances, to adjust our U.S. deferred tax assets to an amount that was “more likely than not” to be realized. These adjustments

were primarily caused by fluctuations of the U.S. dollar against currencies of some of our key markets.

During the third quarter of 2015, we recorded an additional valuation allowance on our remaining U.S. deferred tax assets of $649.5. The

increase in the valuation allowance resulted from management’s determination that it was no longer more likely than not to realize the tax

benefits expected to be obtained from tax planning strategies associated with an anticipated accelerated receipt in the U.S. of foreign source

income. As the U.S. dollar had further strengthened against currencies of some of our key markets during the third quarter of 2015, the

benefits associated with the Company’s tax planning strategies were no longer sufficient for the Company to continue to conclude that its

tax planning strategies were prudent. In the absence of any alternative prudent tax planning strategies and other sources of future taxable

income, it was determined that a full valuation allowance should be recorded. Although the Company continues to expect that it will

generate taxable income and tax liability in the U.S., the Company is expected to offset its current and future tax liability with foreign tax

credits, and as a result, the expected level of future taxable income and tax liability is not adequate to realize the benefit of previously

recorded deferred tax assets. Although the Company may not be able to recognize a financial statement benefit associated with its deferred

tax assets, the Company will continue to manage and plan for the utilization of its deferred tax assets to avoid the expiration of deferred tax

assets that have limited lives.

A V O N 2015 F-25

7553_fin.pdf 97