AT&T Wireless 2009 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2009 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

|

|

AT&T 09 AR 83

plans’ investments. Actual long-term return can, in relatively

stable markets, also serve as a factor in determining future

expectations. However, the dramatic adverse market

conditions in 2008 have skewed traditional measures of

long-term return, such as the 10-year return, which was 3.67%

through 2009 and 4.21% through 2008, compared with 9.18%

through 2007. The severity of the 2008 losses may make the

10-year return less of a relevant factor in future expectations.

In 2009, we experienced actual returns on investments much

greater than what was expected, which will create a reduction

in combined pension and postretirement costs for 2010.

Based on the future expectations for the target asset mix, this

assumption will remain unchanged for 2010. We consider

many factors that include, but are not limited to, historical

returns on plan assets, current market information on long-

term returns (e.g., long-term bond rates) and current and

target asset allocations between asset categories. The target

asset allocation is determined based on consultations with

external investment advisors. This assumption, which is based

on our long-term expectations of market returns in future

years, is one of the most significant of the weighted-average

assumptions used to determine our actuarial estimates of

pension and postretirement benefit expense. If all other

factors were to remain unchanged, we expect that a 1%

decrease in the expected long-term rate of return would

cause 2010 combined pension and postretirement cost to

increase $639.

Composite Rate of Compensation Increase Our expected

composite rate of compensation increase of 4% reflects the

long-term average rate of salary increases.

Health Care Cost Trend Our health care cost trend

assumptions are developed based on historical cost data, the

near-term outlook and an assessment of likely long-term

trends. In addition to the health care cost trend, we assume

an annual 3% growth in administrative expenses and an

annual 3% growth in dental claims. Due to benefit design

changes (e.g., increased co-pays and deductibles for

prescription drugs and certain medical services), we have

generally experienced better-than-expected claims cost in

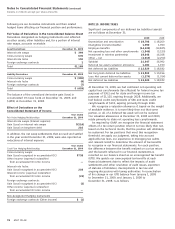

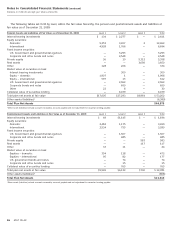

recent years. The following table provides our assumed

average health care cost trend based on the demographics

of plan participants:

2010 2009

Health care cost trend rate assumed

for current year

Retirees 64 and under 5.00% 5.21%

Retirees 65 and over 5.00% 5.36%

Rate to which the cost trend is assumed

to decline (the ultimate trend rate) 5.00% 5.00%

Year that rate reaches the

ultimate trend rate 2010 2010

Approximately 10% of pension and postretirement costs are

capitalized as part of construction labor, providing a small

reduction in the net expense recorded. Uncertainty in the

securities markets and U.S. economy could result in

investment returns less than those assumed. GAAP requires

that actual gains and losses on pension and postretirement

plan assets be recognized in the market-related value of

assets (MRVA) equally over a period of not more than five

years. We use a methodology, allowed under GAAP, under

which we hold the MRVA to within 20% of the actual fair

value of plan assets, which can have the effect of

accelerating the recognition of excess actual gains and

losses into the MRVA to less than five years. Due to

investment losses on plan assets experienced in 2008, this

methodology contributed approximately $1,577 to our

combined net pension and postretirement cost in 2009 as

compared with not using this methodology. This methodology

did not have a material impact on 2008 and 2007 combined

net pension and postretirement benefits. Should the

securities markets decline or medical and prescription drug

costs increase at a rate greater than assumed, we would

expect increasing annual combined net pension and

postretirement costs for the next several years. Should actual

experience differ from actuarial assumptions, the projected

pension benefit obligation and net pension cost and

accumulated postretirement benefit obligation and

postretirement benefit cost would be affected in future years.

Discount Rate Our assumed discount rate of 6.50% at

December 31, 2009, reflects the hypothetical rate at which

the projected benefit obligations could be effectively settled

or paid out to participants. We determined our discount rate

based on a range of factors, including a yield curve comprised

of the rates of return on several hundred high-quality, fixed-

income corporate bonds available at the measurement date

and the related expected duration for the obligations.

These bonds were all rated at least Aa3 or AA- by one

of the nationally recognized statistical rating organizations,

denominated in U.S. dollars, and neither callable, convertible

nor index linked. For the year ended December 31, 2009, we

decreased our discount rate by 0.50%, resulting in an increase

in our pension plan benefit obligation of $2,065 and an

increase in our postretirement benefit obligation of $1,847.

For the year ended December 31, 2008, we increased our

discount rate by 0.50%, resulting in a decrease in our pension

plan benefit obligation of $2,176 and a decrease in our

postretirement benefit obligation of $2,154.

Expected Long-Term Rate of Return Our expected

long-term rate of return on plan assets of 8.50% for 2010 and

2009 reflects the average rate of earnings expected on the

funds invested, or to be invested, to provide for the benefits

included in the projected benefit obligations. In setting the

long-term assumed rate of return, management considers

capital markets future expectations and the asset mix of the