AT&T Wireless 2009 Annual Report Download - page 43

Download and view the complete annual report

Please find page 43 of the 2009 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

33 -

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

AT&T 09 AR 41

2010 Expense Trends We expect a challenging operating

environment for 2010. We will continue to focus sharply on

cost-control measures, including areas such as organizational

and systems integration. We will continue our ongoing

initiatives to improve customer service and billing so we

can realize our strategy of bundling services and providing a

simple customer experience. We expect our 2010 operating

income margin to be stable with the opportunity to improve

margins, in the event the U.S. economy improves. We do not

expect significant pension funding requirements in 2010.

Expenses related to growth areas of our business, especially

in the wireless area, will apply some pressure to our operating

income margin.

Market Conditions During 2009, the securities and

mortgage markets and the banking system in general

experienced some stabilization compared with 2008 as the

year progressed, although bank lending and the housing

industry remained weak. The ongoing weakness in the general

economy has also affected our customer and supplier bases.

We saw lower demand from our residential customers as well

as our business customers at all organizational sizes. Some of

our suppliers continue to experience increased financial and

operating costs. To a large extent, these negative trends were

offset by continued growth in our wireless and IP-related

services. While the economy appears to have stabilized at

a weakened level at year-end, we do not expect a quick

return to growth during 2010. Should the economy instead

deter iorate further, we likely will experience further pressure

on pricing and margins as we compete for both wireline

and wireless customers who have less discretionary income.

We also may experience difficulty purchasing equipment in

a timely manner or maintaining and replacing warranteed

equipment from our suppliers.

Included on our consolidated balance sheets are assets

held by benefit plans for the payment of future benefits.

The losses associated with the securities markets declines

during 2008 are not expected to have an impact on the ability

of our benefit plans to pay benefits. We do not expect to

make significant funding contributions to our pension plans

in 2010. However, because our pension plans are subject to

funding requirements of the Employee Retirement Income

Security Act of 1974, as amended (ERISA), a continued

weakness in the markets could require us to make

contributions to the pension plans in order to maintain

minimum funding requirements as established by ERISA.

In addition, our policy on recognizing losses on investments

in the pension and other postretirement plans accelerated

the recognition of losses in 2009 earnings (see “Significant

Accounting Policies and Estimates”).

OPERATING ENVIRONMENT OVERVIEW

AT&T subsidiaries operating within the U.S. are subject to

federal and state regulatory authorities. AT&T subsidiaries

operating outside the U.S. are subject to the jurisdiction

of national and supranational regulatory authorities in

the markets where service is provided, and regulation is

generally limited to operational licensing authority for the

provision of services to enterprise customers.

Our Other segment also includes our equity investments

in international companies, the income from which we report

as equity in net income of affiliates. Our earnings from foreign

affiliates are sensitive to exchange-rate changes in the value

of the respective local currencies. Our foreign investments

are recorded under generally accepted accounting principles

(GAAP), which include adjustments for the equity method

of accounting and exclude certain adjustments required for

local reporting in specific countries. Our equity in net income

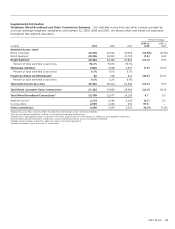

of affiliates by major investment is listed below:

2009 2008 2007

América Móvil $505 $469 $381

Telmex 133 252 265

Telmex Internacional 72 72 —

Other (4) 1 (1)

Other Segment Equity in

Net Income of Affiliates $706 $794 $645

Equity in net income of affiliates decreased $88 in 2009.

Our investment in Telmex and Telmex Internacional

decreased $119, reflecting lower operating results and

currency translation losses, partially offset by $36 of improved

operating results at América Móvil. The $149 increase in 2008

reflects improved operating results at América Móvil, as well

as lower depreciation and tax expenses, and improved results

at Telmex and Telmex Internacional. On January 13, 2010,

América Móvil announced that its Board of Directors had

authorized it to submit an offer for 100% of the equity of

Carso Global Telecom, S.A. de C.V. (CGT), a holding company

that owns 59.4% of Telmex and 60.7% of Telmex Internacional,

in exchange for América Móvil shares; and an offer for

Telmex Internacional shares not owned by CGT, to be

purchased for cash or to be exchanged for América Móvil

shares, at the election of the shareholders.

OPER ATING E NVIRO N M ENT A ND T R E NDS O F T H E BUS I N E SS

2010 Revenue Trends We expect our operating environ-

ment in 2010 to remain challenging as the economic

recession continues, competition remains strong and the

federal regulatory framework may or may not remain

receptive to investment. Despite this environment, we expect

our operating revenues in 2010 to remain stable, reflecting

continuing growth in our wireless and broadband/data

services. We expect our primary driver of growth to be

wireless, especially in sales and increased use of advanced

handsets and emerging devices (such as netbooks, eReaders

and mobile navigation devices) and that all our major

customer categories will continue to increase their use

of Internet-based broadband/data services. We expect

continuing declines in traditional access lines and in

advertising from our print directories. Where available, our

U-verse services are proving effective in stemming access

line losses, and we expect to continue to expand our

U-verse service offerings in 2010.