AT&T Wireless 2009 Annual Report Download - page 44

Download and view the complete annual report

Please find page 44 of the 2009 AT&T Wireless annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

34 -

35

35 -

36

36 -

37

37 -

38

38 -

39

39 -

40

40 -

41

41 -

42

42 -

43

43 -

44

44 -

45

45 -

46

46 -

47

47 -

48

48 -

49

49 -

50

50 -

51

51 -

52

52 -

53

53 -

54

54 -

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

|

|

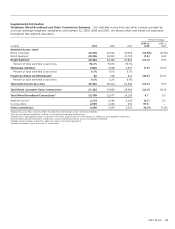

Management’s Discussion and Analysis of Financial Condition and Results of Operations (continued)

Dollars in millions except per share amounts

42 AT&T 09 AR

and has begun investigating how to develop policies to

promote that goal. While wireless communications providers’

prices and service offerings are generally not subject to state

regulation, an increasing number of states are attempting to

regulate or legislate various aspects of wireless services, such

as in the area of consumer protection.

AT&T has previously noted that the broadband marketplace

is robustly competitive and that we do not block consumers

from accessing the lawful Internet sites of their choice.

We therefore believe that prescriptive “net neutrality” rules

are not only unnecessary but also counterproductive to the

extent they would restrict broadband Internet access providers

from developing innovative new services for consumers

and/or content and application providers. Nor do we believe

that wireless providers should be prohibited from entering into

exclusive arrangements with handset manufacturers or that

government should regulate wireless early termination fees

as is currently being proposed. It is widely recognized that

the wireless industry in the United States is characterized by

innovation, differentiation, declining prices and extensive

competition among handset manufac turers, service providers

and applications. For this reason, additional broadband

regulation and new wireless requirements are unwarranted.

Expected Growth Areas

We expect our wireless services and data wireline products to

remain the most significant portion of our business and have

also discussed trends affecting the segments in which we

report results for these products (see “Wireless Segment

Results” and “Wireline Segment Results”). Over the next few

years, we expect an increasing percentage of our growth to

come from: (1) our wireless service and (2) data/broadband,

through existing and new services. We expect that our previous

acquisitions will enable us to strengthen the reach and

sophistication of our network facilities, increase our large-

business customer base and enhance the opportunity to

market wireless services to that customer base. Whether, or

the extent to which, growth in these areas will offset declines

in other areas of our business is not known.

Wireless Wireless is our fastest-growing revenue stream

and we expect to deliver continued revenue growth in the

coming years. We believe that we are in a growth period of

wireless data usage and that there are substantial

opportunities available for next-generation converged services

that combine wireless, broadband, voice and video.

Our Universal Mobile Telecommunications System/High-

Speed Downlink Packet Access 3G network technology covers

most major metropolitan areas of the U.S. This technology

provides superior speeds for data and video services, and it

offers operating efficiencies by using the same spectrum and

infrastructure for voice and data on an IP-based platform.

Our wireless networks also rely on digital transmission

techno logies known as GSM, General Packet Radio Services

and Enhanced Data Rates for GSM Evolution for data

communi cations. As of December 31, 2009, we served

85.1 million customers. We have also announced plans

to transition from 3G network technology to a higher

In the Telecommunications Act of 1996 (Telecom Act),

Congress established a national policy framework intended

to bring the benefits of competition and investment in

advanced telecommunications facilities and services to all

Americans by opening all telecommunications markets to

competition and reducing or eliminating regulatory burdens

that harm consumer welfare. However, since the Telecom Act

was passed, the Federal Communications Commission (FCC)

and some state regulatory commissions have maintained

certain regulatory requirements that were imposed decades

ago on our traditional wireline subsidiaries when they

operated as legal monopolies. Where appropriate, we are

pursuing additional legislative and regulatory measures to

reduce regulatory burdens that inhibit our ability to compete

more effectively and offer services wanted and needed by

our customers. For example, we are supporting regulatory

and legislative efforts that would offer new video entrants

a streamlined process for bringing new video services to

market and for offering more timely competition to traditional

cable television providers. With the advent of the Obama

Administration, the composition of the FCC has changed,

and the new Commission appears to be more open than the

prior Commission to maintaining or expanding regulatory

requirements on entities subject to its jurisdiction. In addition,

Congress, the President and the FCC all have declared a

national policy objective of ensuring that all Americans have

access to broadband technologies and services. To that end,

Congress has charged the FCC with developing a National

Broadband Plan and delivering that plan to Congress in early

2010. The Commission has issued dozens of notices seeking

comment on whether and how it should modify its rules and

policies on a host of issues, which would affect all segments

of the communications industry, to achieve universal access

to broadband. These issues include rules and policies relating

to universal service support, intercarrier compensation and

regulation of special access services, as well as a variety of

others that could have an impact on AT&T’s operations and

revenues. However, at this stage, it is too early to assess

what, if any, impact such changes could have on us.

In addition, states representing a majority of our local

service access lines have adopted legislation that enables

new video entrants to acquire a single statewide or state-

approved franchise (as opposed to the need to acquire

hundreds or even thousands of municipal-approved

franchises) to offer competitive video services. We also

are supporting efforts to update and improve regulatory

treatment for retail services. Passage of legislation is

uncertain and depends on many factors.

Our wireless operations operate in robust competitive

markets but are likewise subject to substantial governmental

regulation. Wireless communications providers must be

licensed by the FCC to provide communications services at

specified spectrum frequencies within specified geographic

areas and must comply with the rules and policies governing

the use of the spectrum as adopted by the FCC. The FCC has

recognized the importance of providing carriers with access

to adequate spectrum to permit continued wireless growth