TCF Bank 2012 Annual Report Download - page 103

Download and view the complete annual report

Please find page 103 of the 2012 TCF Bank annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

93 -

94

94 -

95

95 -

96

96 -

97

97 -

98

98 -

99

99 -

100

100 -

101

101 -

102

102 -

103

103 -

104

104 -

105

105 -

106

106 -

107

107 -

108

108 -

109

109 -

110

110 -

111

111 -

112

112 -

113

113 -

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

|

|

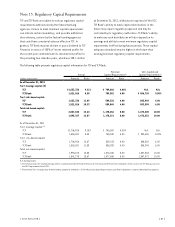

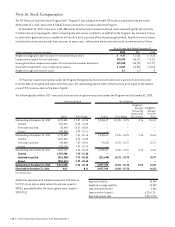

Note 15. Regulatory Capital Requirements

TCF and TCF Bank are subject to various regulatory capital

requirements administered by the federal banking

agencies. Failure to meet minimum capital requirements

can initiate certain mandatory, and possible additional

discretionary, actions by the federal banking agencies

that could have a material adverse effect on TCF. In

general, TCF Bank may not declare or pay a dividend to TCF

Financial in excess of 100% of its net retained profits for

the current year combined with its retained net profits for

the preceding two calendar years, which was $28.1 million

at December 31, 2012, without prior approval of the OCC.

TCF Bank’s ability to make capital distributions in the

future may require regulatory approval and may be

restricted by its regulatory authorities. TCF Bank’s ability

to make any such distributions will also depend on its

earnings and ability to meet minimum regulatory capital

requirements in effect during future periods. These capital

adequacy standards may be higher in the future than

existing minimum regulatory capital requirements.

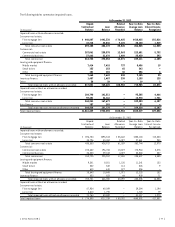

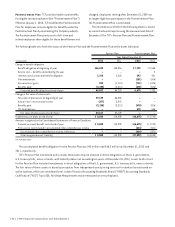

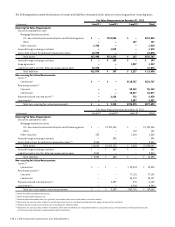

The following table presents regulatory capital information for TCF and TCF Bank.

Actual

Minimum

Capital Requirement(1)

Well-Capitalized

Capital Requirement(1)

(Dollars in thousands) Amount Ratio Amount Ratio Amount Ratio

As of December 31, 2012

Tier 1 leverage capital:(2)

TCF $1,633,336 9.21% $ 709,606 4.00% N.A. N.A.

TCF Bank 1,521,026 8.58 709,382 4.00 $ 886,728 5.00%

Tier 1 risk-based capital:

TCF 1,633,336 11.09 589,328 4.00 883,992 6.00

TCF Bank 1,521,026 10.33 589,060 4.00 883,590 6.00

Total risk-based capital:

TCF 2,007,835 13.63 1,178,656 8.00 1,473,320 10.00

TCF Bank 1,895,367 12.87 1,178,121 8.00 1,472,651 10.00

As of December 31, 2011

Tier 1 leverage capital:(2)

TCF $1,706,926 9.15% $ 745,887 4.00% N.A. N.A.

TCF Bank 1,553,381 8.33 745,940 4.00 $ 932,426 5.00%

Tier 1 risk-based capital:

TCF 1,706,926 12.67 539,013 4.00 808,520 6.00

TCF Bank 1,553,381 11.53 538,829 4.00 808,243 6.00

Total risk-based capital:

TCF 1,994,875 14.80 1,078,026 8.00 1,347,533 10.00

TCF Bank 1,841,273 13.67 1,077,658 8.00 1,347,072 10.00

N.A. Not Applicable.

(1) The minimum and well-capitalized requirements are determined by the Federal Reserve for TCF and by the Office of the Comptroller of the Currency for TCF Bank pursuant to

the FDIC Improvement Act of 1991.

(2) The minimum Tier 1 leverage ratio for bank holding companies and banks is 3.0 or 4.0 percent, depending on factors specified in regulations issued by federal banking agencies.

{ 2012 Form 10K } { 87 }