Johnson Controls 2010 Annual Report Download - page 85

Download and view the complete annual report

Please find page 85 of the 2010 Johnson Controls annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

75 -

76

76 -

77

77 -

78

78 -

79

79 -

80

80 -

81

81 -

82

82 -

83

83 -

84

84 -

85

85 -

86

86 -

87

87 -

88

88 -

89

89 -

90

90 -

91

91 -

92

92 -

93

93 -

94

94 -

95

95 -

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

|

|

85

Hedge Funds: The fair value of hedge funds is accounted for by a custodian. The custodian obtains valuations from

underlying managers based on market quotes for the most liquid assets and alternative methods for assets that do not

have sufficient trading activity to derive prices. The Company and custodian review the methods used by the

underlying managers to value the assets. The Company believes this is an appropriate methodology to obtain the fair

value of these assets.

Real Estate: The fair value of investment in real estate is valued by the fund managers. The fund managers value the

real estate investments via independent third-party appraisals on a periodic basis. Assumptions used to revalue the

properties are updated every quarter. The Company believes this is an appropriate methodology to obtain the fair

value of these assets. For the component of the real estate portfolio under development, the investments are carried

at cost until they are completed and valued by a third-party appraiser.

The methods described above may produce a fair value calculation that may not be indicative of net realizable value

or reflective of future fair values. Furthermore, while the Company believes its valuation methods are appropriate

and consistent with other market participants, the use of different methodologies or assumptions to determine the

fair value of certain financial instruments could result in a different fair value measurement at the reporting date.

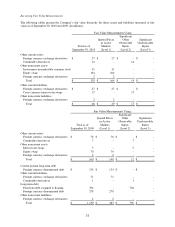

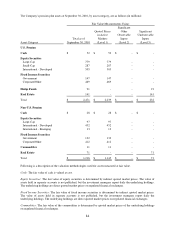

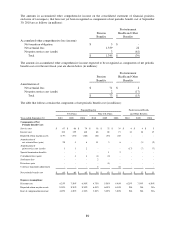

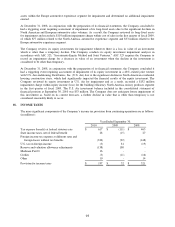

The following sets forth a summary of changes in the fair value of assets measured using significant unobservable

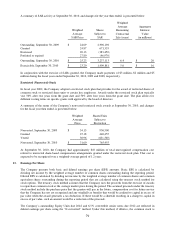

inputs (Level 3) (in millions):

Total

Hedge Funds

Real Estate

U.S. Pension

Asset Value as of September 30, 2009

$

174

$

86

$

88

Additions

59

-

59

Redemptions

(9)

-

(9)

Realized loss

(5)

-

(5)

Unrealized gain

13

5

8

Asset Value as of September 30, 2010

$

232

$

91

$

141

Non-U.S. Pension

Asset Value as of September 30, 2009

$

64

$

-

$

64

Unrealized gain

7

-

7

Asset Value as of September 30, 2010

$

71

$

-

$

71

The expected return on plan assets is based on the Company's expectation of the long-term average rate of return of

the capital markets in which the plans invest. The average market returns are adjusted, where appropriate, for active

asset management returns. The expected return reflects the investment policy target asset mix and considers the

historical returns earned for each asset category.

For pension plans with accumulated benefit obligations (ABO) that exceed plan assets, the projected benefit

obligation (PBO), ABO and fair value of plan assets of those plans were $3,942 million, $3,804 million and $3,169

million, respectively, as of September 30, 2010 and $3,316 million, $3,111 million and $2,219 million, respectively,

as of September 30, 2009.