HSBC 2001 Annual Report Download - page 269

Download and view the complete annual report

Please find page 269 of the 2001 HSBC annual report below. You can navigate through the pages in the report by either clicking on the pages listed below, or by using the keyword search tool below to find specific information within the annual report.-

1

1 -

2

-

3

-

4

-

5

-

6

-

7

-

8

-

9

-

10

-

11

-

12

-

13

-

14

-

15

-

16

-

17

-

18

-

19

-

20

-

21

-

22

-

23

-

24

-

25

-

26

-

27

-

28

-

29

-

30

-

31

-

32

-

33

-

34

-

35

-

36

-

37

-

38

-

39

-

40

-

41

-

42

-

43

-

44

-

45

-

46

-

47

-

48

-

49

-

50

-

51

-

52

-

53

-

54

-

55

-

56

-

57

-

58

-

59

-

60

-

61

-

62

-

63

-

64

-

65

-

66

-

67

-

68

-

69

-

70

-

71

-

72

-

73

-

74

-

75

-

76

-

77

-

78

-

79

-

80

-

81

-

82

-

83

-

84

-

85

-

86

-

87

-

88

-

89

-

90

-

91

-

92

-

93

-

94

-

95

-

96

-

97

-

98

-

99

-

100

-

101

-

102

-

103

-

104

-

105

-

106

-

107

-

108

-

109

-

110

-

111

-

112

-

113

-

114

-

115

-

116

-

117

-

118

-

119

-

120

-

121

-

122

-

123

-

124

-

125

-

126

-

127

-

128

-

129

-

130

-

131

-

132

-

133

-

134

-

135

-

136

-

137

-

138

-

139

-

140

-

141

-

142

-

143

-

144

-

145

-

146

-

147

-

148

-

149

-

150

-

151

-

152

-

153

-

154

-

155

-

156

-

157

-

158

-

159

-

160

-

161

-

162

-

163

-

164

-

165

-

166

-

167

-

168

-

169

-

170

-

171

-

172

-

173

-

174

-

175

-

176

-

177

-

178

-

179

-

180

-

181

-

182

-

183

-

184

-

185

-

186

-

187

-

188

-

189

-

190

-

191

-

192

-

193

-

194

-

195

-

196

-

197

-

198

-

199

-

200

-

201

-

202

-

203

-

204

-

205

-

206

-

207

-

208

-

209

-

210

-

211

-

212

-

213

-

214

-

215

-

216

-

217

-

218

-

219

-

220

-

221

-

222

-

223

-

224

-

225

-

226

-

227

-

228

-

229

-

230

-

231

-

232

-

233

-

234

-

235

-

236

-

237

-

238

-

239

-

240

-

241

-

242

-

243

-

244

-

245

-

246

-

247

-

248

-

249

-

250

-

251

-

252

-

253

-

254

-

255

-

256

-

257

-

258

-

259

259 -

260

260 -

261

261 -

262

262 -

263

263 -

264

264 -

265

265 -

266

266 -

267

267 -

268

268 -

269

269 -

270

270 -

271

271 -

272

272 -

273

273 -

274

274 -

275

275 -

276

276 -

277

277 -

278

278 -

279

279 -

280

-

281

-

282

-

283

-

284

|

|

267

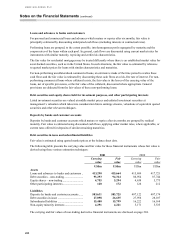

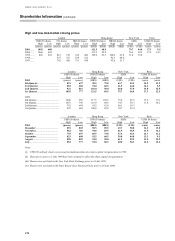

(l) Earnings per share

Basic earnings per share under US GAAP, SFAS 128 ‘Earnings per share’ , is calculated by dividing net income

of US$4,911 million (2000: US$6,236 million; 1999: US$4,889 million) by the weighted average number of

ordinary shares in issue in 2001 of 9,237 million (2000: 8,777 million; 1999: 8,296 million).

Diluted earnings per share under US GAAP is calculated by dividing net income, which requires no adjustment

for the effects of dilutive ordinary potential shares, by the weighted average number of shares outstanding plus

the weighted average number of ordinary shares that would be issued on conversion of all the dilutive potential

ordinary shares in 2001 of 9,336 million (2000: 8,865 million; 1999: 8,374 million), as shown in Note 11.

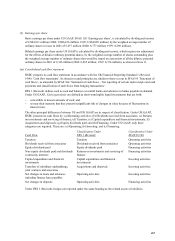

(m) Consolidated cash flow statement

HSBC prepares its cash flow statement in accordance with the UK Financial Reporting Standard 1 (Revised

1996) ‘Cash flow statements’ . Its objectives and principles are similar to those set out in SFAS 95 ‘Statement of

cash flows’ , as amended by SFAS 104 ‘Statement of cash flows – Net reporting of certain cash receipts and cash

payments and classification of cash flows from hedging transactions’ .

FRS 1 (Revised) defines cash as cash and balances at central banks and advances to banks payable on demand.

Under US GAAP, Cash equivalents are defined as short-term highly liquid investments that are both:

− convertible to known amounts of cash; and

− so near their maturity that they present insignificant risk of changes in value because of fluctuations in

interest rates.

The other principal differences between US and UK GAAP are in respect of classification. Under UK GAAP,

HSBC presents its cash flows by: (a) Operating activities; (b) Dividends received from associates; (c) Returns

on investments and servicing of finance; (d) Taxation; (e) Capital expenditure and financial investments; (f)

Acquisitions and disposals; (g) Equity dividends paid; and (h) Financing. Under US GAAP, only three

categories are required. These are: (a) Operating; (b) Investing; and (c) Financing.

Classification Under Classification Under

Cash Flow FRS 1 (Revised) SFAS 95/104

Taxation Taxation Operating activities

Dividends received from associates Dividends received from associates Operating activities

Equity dividends paid Equity dividends paid Financing activities

Non-equity dividends paid and dividends

to minority interests

Returns on investments and servicing of

finance

Financing activities

Capital expenditure and financial

investments

Capital expenditure and financial

investments

Investing activities

Transfers of subsidiary undertakings,

joint ventures and associates

Acquisitions and disposals Investing activities

Net changes in loans and advances

including finance lease payables

Operating activities Investing activities

Net changes in deposits Operating activities Financing activities

Under FRS 1 (Revised), hedges are reported under the same heading as the related assets or liabilities.